Cash Balance Optimization Using AI & Big Data

Garanti BBVA has developed software using Big Data and Artificial Intelligence (AI) to manage its cash logistics. Alper Sayin, Head of Cash Planning and Operations, has written about his experience introducing this software and how they are using it.

Why Big Data?

Garanti BBVA is the second largest private bank in Turkey and its Cash Planning & Operations Department manages its cash logistics and cash processing in-house. Cash services are provided to 7,216 service points (branches, off-site ATMs and retail points) via a fleet of 255 armoured vehicles and 45 cash centers. The different dynamics of its 911 branches, located all over the country, create a wide range of variables and unique cash flows. In addition, to increase the accuracy of the predictions, the bank uses historical data for all of the routines, seasons and customer transactions.

The data set for all of the branches for all of the possible variables (some 180 are used, including the historical data) runs into the billions. Traditional calculations cannot manage the combinations and iterations of data to be considered, and so Big Data tools are needed. In addition, the bank wants to use AI tools that can automatically and continuously learn from events.

In-house development vs. outsourcing

When deciding between developing software, either in-house or outsourcing it, the key issues to be evaluated are:

An in-house model will be tailor made and a flexible tool. Additionally, it should be easier to integrate into your core banking system. If the software is outsourced, it won’t offer this much flexibility. However, an outsourced model has the advantage of being proven and so should have fewer ‘bugs’ and have been designed based on many user cases.

To develop in-house software requires capex for GPUs (Graphics Processing Units) to compute big data and to train big data analytic teams and developers, while outsourced software may require lower investment costs.

The precision and accuracy of the tool increases as the number of variables increase. However, you may not be able to share private information (ie. customer demographics) with your vendor. Garanti bank use 180 variables but could share only 30 of them with their vendor. This means a dramatic limitation of the data set.

The level of support after going live is important. Traditionally, when you outsource, there will be a dedicated team ready to solve your problems and they follow the latest updates and needs in the market and enhance the product all the time. Looking back to the in-house case, if you don’t have a dedicated team and structured up-time procedures, troubleshooting and additional enhancements may be a problem.

When you use the in-house model you will be independent from the vendor’s calendar for updates. Additionally, some vendors may not have all of the plug-ins you want. For example, if your vendor cannot provide route optimisation together with a cash optimisation tool, you have to look for another vendor or push your vendor to develop a tool for you. In both cases the additional cost can be much higher than adding the necessary tools to your in-house model.

Other key points before you start are:

Make sure you have well defined variables and constraints.

Your data should be very consistent. Avoid dirty data that can mislead your predictions.

Develop a parametric structure (constraints and rules) for possible business model changes.

Variables & algorithms used

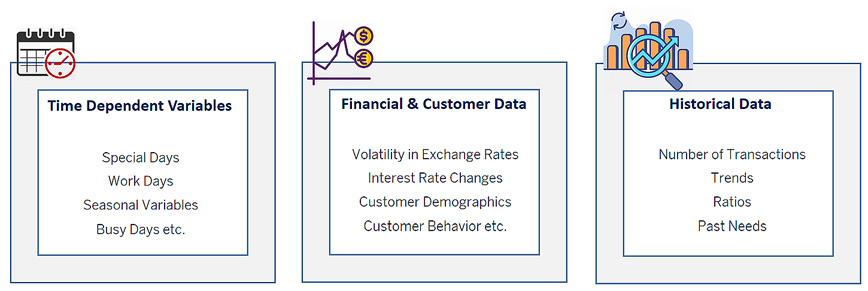

The number of variables used in our model is 180. There are three types of variable data sets (Figure 1) talking to each other.

Fig 1: Variable sets.

Fig 1: Variable sets.For example, in branch A, each September, farmers who have loans bring cash to the branch every Monday and Wednesday afternoon between 14.00 and 16.00. This is the September routine of this specific branch. The model estimates different optimum cash levels for September and other months. These routines can be hourly, daily, monthly, yearly etc.

Also, the model is able to catch changing routines according to market conditions. For example, if the USD/TL exchange rate fluctuates, the USD cash demand would increase at the branches whose customers are mainly dealing with FX trade.

As seen in the above example, the more variables and data you use, the greater the precision of the model as you capture more routines and cycles. The bank has tested a number of algorithms, but achieved the best results with the random forest algorithm.

The bank predicts how much money should be kept at the branch until the next visit of an armoured vehicle. To ensure cash outs are avoided it adds an extra margin to the forecast. Each branch is modeled separately because of the unique dynamics. The model will re-learn on a monthly basis and so, in the case of opening a new branch, it will produce estimates after the first month.

POV & POC results

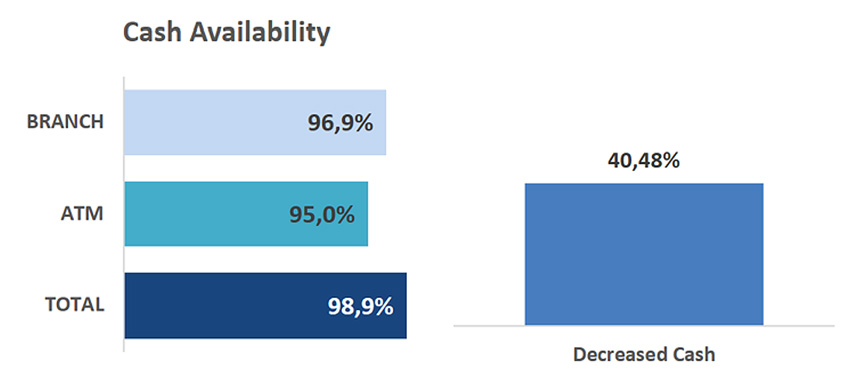

After deciding on the variables, algorithms and constraints, the bank made a POV (proof of value) study with the historical data of nine different branches. On average, it was discovered that these branches could keep 40% less cash and still maintain a cash availability of 98,9% (see Figure 2).

Although total availability is high, the bank saw some cash outs at ATMs and tellers. Thanks to the parametric structure, the bank could run a live POC (proof of concept) with conservative margins. The availabilities increased up to 99.7% and cash levels decreased by 30%, without any major cash-outs.

End-user experience and handling ad-hoc cash flows

Another thing the bank experienced was that you should design a user-friendly monitoring screen for the branch. Its branch screen makes real time calculations and, depending on the current balance and the predicted amount, it shows a single action to the branch personnel – ‘give x amount to the armored vehicle’ or ‘order y amount from cash center’. This is simple for staff to use.

There is crucial data that should be taken from the branch manually. These are the ad-hoc (out of routine) bulk amounts reserved for withdrawal or deposited by customers. Since these amounts are not routine transactions, they cannot be detected by the model.

In response, the bank created an additional screen where branches can enter the details (customer ID, date, time, amount) of these ad-hoc cash movements. The screen knows the time period of the transaction and can add this ad-hoc amount to the real time calculations.

Additionally, the branch can see its performance in terms of compliance with the predictions and realisation of the ad hoc orders. On the other hand, the bank has performance reports for the process owner based on Service Level Agreements and Key Performance Indicators of each branch.

Step by step towards integrated cash cycle

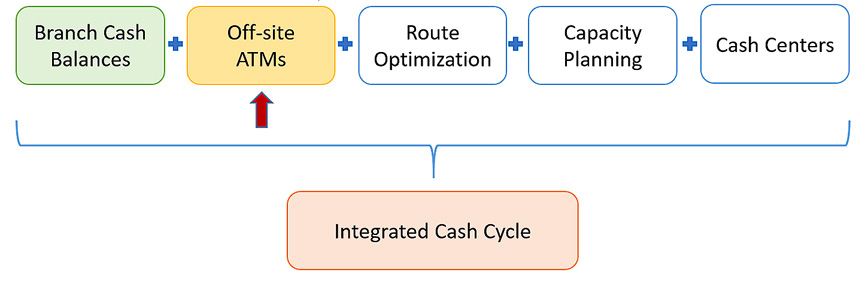

The banks vision is to optimise the whole cash cycle in terms of idle cash and resources allocated for this business line (Figure 3). The bank started with branch cash balances. Now the bank is preparing to develop a cash optimisation tool for off-site ATMs and vehicle routes.

Fig 3: End to end optimisation.

Fig 3: End to end optimisation.Combining the cash and route optimisation will bring opportunities for better capacity planning. From this level on, constraints will be more flexible and interchangeable. When optimising cash levels and routes together, it may end up with much more efficient results such as ‘fewer visits and less cash’.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.