Cash Increases Risk for Central Banks

A recent paper, ‘COVID Cash*’, by Kenneth Rogoff and Jessica Scazzero considers the implications for advanced economies in the long-term trend of value being stored in cash, a trend accelerated by, and highly visible due to, the pandemic. They make two arguments.

Firstly, most of this cash is being held due to criminal intent or tax evasion, and the resulting lost value to the economy and the cost of policing this means the seigniorage benefits are small or negative. (Rogoff is, of course, well-known for his views in our industry through his book ‘The Curse of Cash: How Large-Denomination Bills Aid Crime and Tax Evasion and Constrain Monetary Policy’).

Secondly, people can swiftly move from holding value as cash to holding it in bank accounts should interest rates or circumstances change. A quick reversal will require central banks to convert their long-term interest-bearing assets into funds to pay to the banks that are, effectively, with a maturity close to zero. This disrupts government debt funding and introduces volatility, adding complexity to what will probably already be a difficult time.

Cash usage today

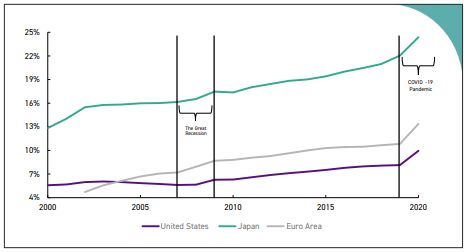

The data for the increase in cash demand during the pandemic, along with the increase in contactless electronic payments, is now well known. The authors argued that this is an extension of an already noted long term phenomenon.

Given that, they asked whether the increase in demand for banknotes means we are not going cashless and whether a strong demand for cash is a good thing.

For this second question, the paper assessed the answer as part of the consolidated government balance sheet.

Value of cash to a government

Interest rates are core to this discussion. With long term interest rates so low, many governments can borrow cheaply. Seigniorage income is so low that the costs of cash almost make it not worth having.

To put it another way, if cash was withdrawn and replaced by a CBDC and the government borrowed that money, the borrowing costs of giving up cash would not be high. The paper used the 0.95% December 18 rate on 10-year US treasury bills and multiplied it by the $2.2 trillion in circulation in the US (the September figure), giving a cost of $21 billion. The paper examines this from a number of angles and in great detail.

If cash is, effectively, a zero-interest perpetual bond, it protects the government against debt distress or future rises in interest rates. Is this an argument for cash? But the paper shows it can’t be regarded as a zero-interest perpetual bond because cash holders can always, and swiftly, put cash in a bank account. At this point it becomes part of bank reserves, with a maturity close to zero.

The demand for cash by the public is related to the long-term interest rate, and the tax rate, in countries. The authors’ work, mirrored in a BIS 2019 study, found that the long-term demand for cash balances, relative to nominal GDP, would fall by 0.65% with a 1% increase in the steady state treasury bill rate. Their work found that interest rates only influence the demand for high denomination banknotes.

The baseline regression with US government bond interest rates and tax/ GDP, the roughly 4% average drop in 10 year Treasury nominal interest rates since 2000, can account for a roughly 2.5% increase in the currency/GDP ratio.

The paper does not draw conclusions, but it is worth noting that interest and tax rates can change. In a less benign environment the observations of this study might be different.

Cash as a store of value

The paper explored the thought that since many governments can borrow so cheaply, where is the advantage in issuing cash? Why not create a CBDC and allow people to hold their stored value in risk free CBDCs, whether the account is at the central bank or a commercial bank?

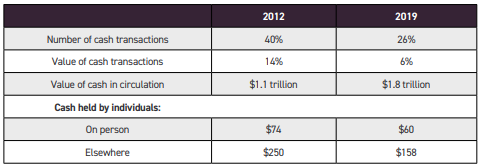

They presented data that showed the issue of high denomination notes along with the extensive data on electronic payments. The cash volume and value data proves that the increase in cash in circulation is to store value rather than for transactions. They concluded that the electronic data, a significant increase in debit card transactions accompanied by a decrease in the average transaction value, provides overwhelming evidence that fewer transactions are in cash.

They argued that people hold cash because it cannot be tracked. A relatively small proportion of people would, therefore, opt to hold CBDCs, perhaps as low as 20%.

The preference for cash, whether tax evasion or criminality, diverts significant resources to combating both of these, and it removes value from circulation where it could be boosting the economy. In a 2016 paper, Rogoff had suggested that the shadow economy represented 8-25% of GDP in advanced economies.

The conclusion was that the seigniorage earned by the central bank, particularly when there are low interest rates, is significantly less than the cost of these cash holdings and fighting the evasive behaviour. Although the paper does not state it in this way, if one follows the logic of their argument, the store of value function of cash is detrimental to the economy.

* COVID Cash, published by Centre for Monetary and Financial Alternatives (CMFA): Working Paper 002/2021

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.