Contactless Payments Have Little Impact on Cash Usage

Marie-Hélène Felt wrote the Bank of Canada’s Staff Working Paper 2020-56 'Losing Contact: The Impact of Contactless Payments on Cash Usage'.

It addresses an important topic for the future of cash, whether there is a causal link between the decline in cash transactions and the rise in contactless payments. The short answer is no, but the paper includes rich detail supporting that answer and highlights just how much impact the ‘cost’ of getting cash is and how it affects behaviour. In particular, ‘cost’ includes the distance to bank branches and Automatic Banknote Machines (ABMs).

The approach used

The paper builds on the extensive research already done in this area, using the latest data, assessing how the Canadian Financial Monitor (CFM) panel data estimates have varied over the sample period, investigating the heterogeneity in the impact of contactless credit cards (CTCs) across households using Finite Mixture Modelling and using a two-part model that properly takes into account the corner-solution nature of the dependent variable ‘cash share’.

The paper is an economist’s delight, but it contains rich nuggets for those who have a less technical interest.

Canadian data

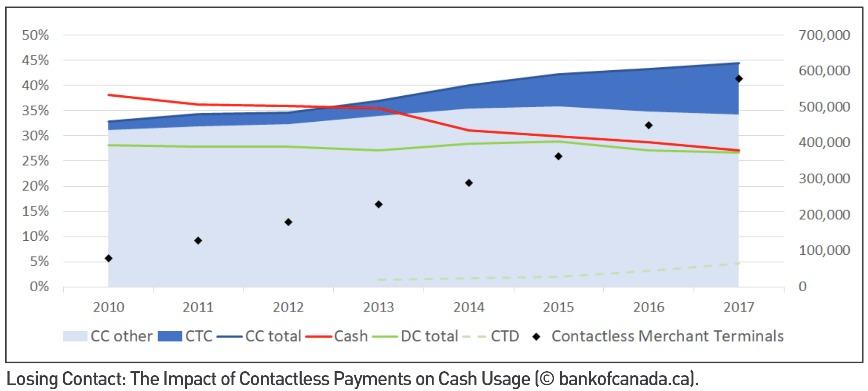

CTCs were introduced in Canada in 2006 by MasterCard, with Visa following the next year. Between 2007 and 2015 their adoption was relatively slow and this is reflected in the CFM data, where 2016/17 appears to be an inflexion point for their use. Between 2013 and 2018 the point of sale infrastructure for contactless payments increased at a rate of 24% a year.

Cash usage has steadily declined in the meantime, and by 2017 nearly a quarter of CFM respondents said they never or seldom used cash.

The paper looked at households that did not use CTCs and those that did. Generally, CTC users had young families, were employed and homeowners. Over the time the CFMs have been run, this group became more urban and with higher incomes than non-CTC households. The paper was clear, though, that unobserved heterogeneity matters when assessing the impact of CTCs; for example, it could be that being tech ‘savvy’ matters more than, say, home ownership.

Overall, CTC households used cash about 10% less, number of transactions and value, than non-CTC households. Non-CTC households in 2017 used cash for 31% of their transactions, 22% by value, down from 42% and 28% respectively in 2010. The paper concludes that CTCs do have a negative impact on what it calls the ‘intensive margin of cash usage’, but not on its ‘extensive’ margin.

Clearly the starting point for and attitude of CTC and non-CTC households towards how much they use cash and how widely they use it differs significantly, and so the impact of CTCs is different.

Evidence of a causal link

Regression analysis of micro data provided little evidence of a causal relationship between CTCs and cash usage. This was consistent with 2017 research by Chen H, M-H Felt, and K P Huynh that found little or no reduction in cash usage, by 2020 research by Trütsch that found that CTCs and contactless debit cards (CDCs) exert no statistically significant effect on cash usage (based on US data 2009-2013) and 2020 research by Brown M, N Hentschel, H Mettler, and H Stix that found a moderate average reduction in the share of cash payments after the introduction of CTDs in Switzerland (0.6% relative to an average cash share of 68%).

The author applied corner analysis to understand the differences based on whether CFM respondents ‘participated’ – focusing on the theory that the cost of getting and holding cash is a key driver, and the ‘amount’ of cash usage. The study found big differences between the two user types. Households that use cash hold more, spend it more frequently and spend more. It also appeared that it cost them more to get cash.

The model was set up based on the assumption that the optimal withdrawal frequency goes down in line with the relative withdrawal cost (ie. cost per dollar spent) and that both the withdrawal size to cash consumption ratio and the average cash holding to cash consumption ratio would increase in line with that cost.

The large number of households with ‘zero’ cash had a lower withdrawal frequency but had high ratios for cash withdrawals and holdings, suggesting that they regarded cash costs as higher. In Canada though, throughout the CFM study period there has been low and stable inflation, low interest rates and the risk of holding cash has been low.

The author concludes that the amount of cash spent depends on personal preferences and merchant-side factors rather than withdrawal costs.

What drives cash usage?

The final conclusion of the paper was that the overall impact of CTCs on the transactional usage of cash was very small between 2010 and 2017.

What the paper does highlight, though, is the role and impact of ‘geography’ on cash usage, a critical factor as bank branches close and ATM networks shrink. It appears that in terms of the ‘cost’ of getting cash, in Canada the distance travelled rather than monetary costs has a greater effect on cash usage than the introduction of CTCs.

Previous research found that for a given purchase value, higher bank branch and ABM density reduces the level of average consumer cash holdings, presumably causing more cash withdrawals. Similarly, Chen et al concluded that the shorter the distance travelled to get cash, the more frequent the cash withdrawals. In a similar vein, research also found that as retail density reduces, travel to get cash increases. As a result, more online banking takes place.

Do bank branch closures, therefore, lead or follow consumer behaviour? The conclusion of Allen et al was that it leads. For those who wish to preserve payment choice, this paper highlights that perhaps maintaining access to cash is a more important area to focus on rather than worrying about the plethora of alternative payment options.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.