Financial Crime is Not Victimless

Financial crime, particularly digital financial crime, can feel victimless. The losses are factored into the fees and charges which are passed on in higher prices and the press seldom focus on the distress and stress caused to individuals faced with criminal activity. In addition, the authorities continue to focus on cash while the evidence grows that criminals are at least as comfortable, if not more so, working with digital cash.

Crypto currency and crime

Three recent headlines:

7 June: US recovers $2.3 million in bitcoin paid in the Colonial Pipeline ransom

25 June: ‘UK cops seize £114 million in crypto’

13 July: ‘UK cops make record crypto haul in money laundering investigation’ (£180 million).

Despite the recovery of bitcoin achieved by the US authorities in this case, Senator Roy Blunt commented at the time, ‘we have a lot of cash requirements in our country, but we haven’t figured out, in the country or in the world, how to trace cryptocurrency.’

The UK announcements were followed by a statement from London’s Metropolitan Police Deputy assistant commissioner Graham McNulty: ‘proceeds of crime are laundered in many different ways. While cash still remains king in the criminal word, as digital platforms develop we’re increasingly seeing organised criminals using cryptocurrency to launder their dirty money.’

One doesn’t see many headlines about cash hauls matching £114 million and £180 million, and cryptocurrencies are clearly useful for cross border criminal activity. Perhaps the focus needs to be on electronic money rather than constantly decreasing cash payment limits.

UK financial crime

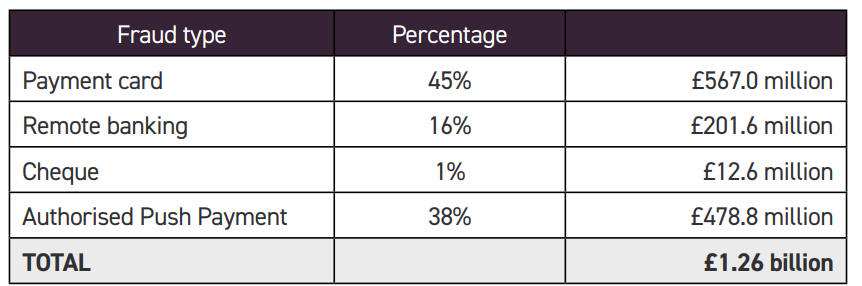

A recent report by UK Finance on fraud provides evidence of the scale of criminal activity. The pandemic has seen an explosion in what is known as ‘authorised push payment’ fraud (APP), where people are persuaded to send funds to the criminals. UK Finance members reported 149,946 APP incidents in 2020 with gross losses of £479 million.

Even without including that category of crime, unauthorised financial fraud losses across payment cards, remote banking and cheques totalled £783.8 million in 2020. The good new being this was a decrease of 5% compared to 2019.

In addition, the financial industry stopped £1.6 billion of unauthorised fraud losses, equivalent to £6.73 in every £10 of attempted fraud being stopped.

Fraud losses on UK-issued cards totalled £574.2 million in 2020, a 7% fall from £620.6 million in 2019. The number of cases was up 3% to 2,835,622. These figures cover fraud on debit, credit, charge and ATM only cards issued in the UK. Payment card fraud losses are organised into five categories: remote purchase (card not present or CNP), counterfeit, lost and stolen, card not received and card ID theft.

Card fraud at UK cash machines was £28.1 million. This covers fraudulent transactions made at cash machines in the UK, either using a stolen card or where a card account has been taken over by the criminal. In all cases the fraudster would need to have access to the genuine PIN and card.

Cheque fraud was down 77% to £12.3 million involving 1,247 incidents. The fraud types were counterfeiting, £7.2 million, and forged or fraudulently altered cheques (£5.1 million).

Although not included in the UK Finance report, in 2020 the Bank of England identified 170,000 counterfeit banknotes with a nominal face value of £3.8 million.

Who pays?

In the UK the banks signed up to a code of conduct that set standards for compensation and preventative advice. The reality has been though, that compensation payments by the eight banks have ranged from 1% to 77% of cases.

Perhaps it is unfair to expect the banks to provide compensation since mobile phone companies don’t prevent criminals assuming a bank customer’s identity using a replacement SIM card and tech companies host online scams. The Information Commissioner’s Office fined organisations that lose consumer data £40 million in 2020, but this money went to the UK Treasury rather than to victims.

The Lending Standards Board overseas the voluntary code. Between May 2019 and July 2020, banks decided that 77% of fraud victims were partially or wholly to blame for their own losses. 60% were found to be fully at fault and so entirely liable for their losses. In only 11% of cases were victims found to be blameless.

Given that ultimately the cost of crime is passed on to the customer through fees, charges and interest rates, the level of crime matters for everybody, not just the immediate victims. Although cash attracts crime and criminals, the accessibility of digital payments makes the threat of loss significant. If the cyber criminals have the impact they are having they will undermine confidence in the new digital world. Perhaps cash has a safe haven role even in this area.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.