News in Brief

DNB’s McKinsey Study Lays Out the Future of Cash

The Dutch National Bank (DNB) spoke at the recent European Cash Cycle seminar (ICCOS) about the McKinsey study commissioned to consider the cash infrastructure the Netherlands will need for the next 10 years. With cash transactions now representing 20% of all transactions, down from 32% pre-pandemic, the Netherlands is preparing for a less cash society.

Olaf Sleijpen, Executive Director, outlined the strengths of cash – peace of mind against emergencies, ease of use, control over spending, public money providing privacy, comfortable way to pay, suitable for all people.

McKinsey identified cash as a back-up for electronic payments, a necessary option for vulnerable people and a general, public means of payment. For the DNB these roles determine the size and the cost of the cash infrastructure. If these roles change, so should the infrastructure.

The paper then goes on to consider how and when those roles may change and how to respond to that. It starts by challenging the private sector to come up with back-ups to electronic payments other than cash. Until those back-ups are in place and being used, cash remains relevant and needed.

With effective, accepted back-ups in place, the DNB sees the response as a shared responsibility. Whatever happens, the future must be inclusive of those who find the digital era challenging or who simply prefer a public means of payment. Achieving an efficient solution will require a co-operative rather than a competitive market approach, albeit overseen by the DNB.

In the final phase, using cash is a choice and people no longer depend on it for payments. At this point cash is a universal service. The DNB sees a bigger role for public institutions in safeguarding accessible, available and affordable cash. The National Payments Forum will have to address this but whatever is decided, it will be a shared future.

The DNB is working on a covenant with all members of the National Payments Forum based on the McKinsey study. It will cover the next five years for how cash will function in the first two phases of change. The covenant is an alternative to regulation and the DNB hopes agreement is imminent.

Paying Bills in Cash Easier in the US

In the US a partnership has been announced to make paying in cash easier. Doxo, a direct-to-consumer bill pay provider, is partnering with InComm Payments to allow people who want to pay bills in cash more options. People will be able to pay bills issued by utility companies and other bill issuers associated with Doxo at retailers in InComm’s VanillaDirect network. There is a charge of $2.50 to pay a bill.

InComm has 65,000 retail stores and Doxo has 100,000 bill issuers in its network. Companies such as Walgreens, CVS, 7-Eleven and Dollar General use InComm’s VanillaDirect platform. 5 million people use its bill-payment app.

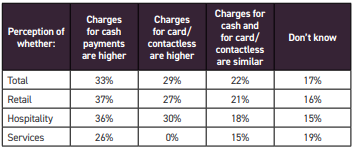

Why do SMEs Accept Cash?

The Financial Conduct Authority in the UK commissioned research from Savanta about what drives small and medium enterprise (SME) owners to accept cash, and how important this was, absolutely and relatively, to accepting digital payments. Small businesses have seen cash use fall 15% since COVID-19 started, with contactless payments up 10%.

Qualitative research in late 2020 surveyed face-to-face intensive SMEs in the retail, hospitality and service sectors. Quantitative research was also carried out between 26 April and 2 July 2021 on businesses with a fewer than 50 staff and an annual turnover of up to £6.5 million.

The businesses were ‘very happy’ to accept cash, with payment choice key; 29% respondents listed it as their prime reason. In the quantitative survey, asked why they accept cash, small business owners ‘would never turn away a customer if they needed to pay cash’ (98%), cash relies less heavily on technology (76%), their customers expect a payment choice (70%), accepting cash is a community service (44%) and there are fewer errors and less fraud with cash (39%).

Cost was of relatively low importance and was not mentioned as an important factor, at the same time awareness of the relative charges was low.

One in five small businesses did not know what the monthly cost of depositing cash was. One in seven did not know the relative cost of accessing cash for use within the business.

The time taken to deposit cash had not changed since COVID started for 49%, and for 11% it had dropped. The remainder had found queuing times had increased and bank and post office opening times had reduced. Half of small businesses had decided to make fewer visits to deposit cash.

Less than one in ten businesses currently offer ‘formal’ cashback with purchases, although in rural areas this was one in seven. The two main reasons for this were lack of customer demand and holding insufficient cash in the till.

Optimising ATMs in Switzerland

Finews in Switzerland has published a piece about how Switzerland should react to a fall in cash withdrawals from ATMs. It claims most Swiss ATMs are now only processing about 30,000 transactions a year even though they are capable of 120,000. The article offers some solutions, including:

Banks focusing on cashless payment methods

Co-operating with the retail sector to access cash in shops

Cutting the number of ATMs, as Postfinance is doing

Optimising the placing of ATMs.

This last option is a key finding in a study by the Swiss Stock Exchange working with Senozon, an analytical consultancy. It appears about 6,000 ATM locations are not actually necessary. The study found that 2,161 ATMs at 1,159 locations are enough in order to serve the entire country, in which case the number of transactions per ATM would rise to 80,000 a year, delivering major cost savings.

If the placing of ATMs was treated as a utility, the distribution of ATMs would increase in popular locations and decrease elsewhere, probably improving the general access to cash. With each ATM costing about $32,500 a year to run, the savings would be about $110 million per year in Switzerland.

One challenge to implementing such a scenario is that not all banks are experiencing the same decline in ATM transactions. One way to interpret this is that cash remains sufficiently important in Switzerland that the banks do not want to give up their competitive advantage. So-called ‘white-labelling’ of ATMs does not yet suit all.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.