Bank of England Reports Cash Recovery

The Bank of England published in its quarterly bulleting an update on cash. The headlines were that cash has made a partial recovery. It has not returned to where it was but given that transaction usage has stabilised, it is probable that it will not recover further to where it was. Cash in circulation remains elevated and has not yet started to fall. The article provides the detailed research and data gathered to understand what has happened and what is likely to happen.

The Bank is clear that there has been a long-term shift in payment habits to using digital payments. Despite that, the Bank’s January 2022 survey found that for about 20% of the population cash is their preferred method of payment, a figure that has not changed from before the pandemic, and which, therefore, probably represents the base figure for cash. The UK Finance’s Payments Market Survey 2022 found 1.1 million people dependent on cash.

Impact of COVID-19 on transactions

Since 2017 the number of transactions made in cash has fallen by about 15% per year. While in 2009 cash was used for 60% of transactions, by 2019 it was 23%, in 2020 17% and in 2021 15%. 2020, therefore, saw cash use fall by 35% but that decrease has slowed.

ATM withdrawals fell 50% at their lowest point in the pandemic, but by mid-2020 had recovered to a 30% reduction. The Bank extrapolated the declining trend in ATM withdrawal values in the years before the pandemic and found that in the second quarter of 2022 ATM use was about 20% down on where it might otherwise have been.

On that basis, the pandemic accelerated the decline in cash use by over five years. UK Finance have estimated that by 2031 only 6% of payments will be made in cash.

Impact of COVID-19 on cash held as a store of value

The value of notes in circulation (NIC) rose 17% between March 2020 and June 2022, an increase of £12.3 billion. In August 2021 COVID restrictions lifted in the UK and the growth of NIC slowed. In June 2022 growth was close to zero.

The long-term trend has been one of growth. Between 2012 and 2021 NIC increased by 50% and the Bank attributes that primarily to uncertainty combined with low interest rates. It has taken longer for cash to be deposited as restrictions lifted from mid-2020, and this may have contributed to weaker inflows to Note Circulation Scheme cash centres between April and August 2020.

Low interest rates, budgeting and disruption to international travel may also have contributed to NIC not falling back. On the other hand, history shows that after large, significant increases, cash outflows do not reverse.

The Bank has carried out three surveys in order to get a better understanding of NIC. In March 2021 it surveyed 5,000 people and found 60% held cash reserves with a median value of £167. A third of people held less than £100. The Bank estimates £10-30 billion is held in domestic reserves.

The variation in how much was held was small between different age groups, but older people actively sought cash by going to ATMs and banks while younger people tended to receive cash as gifts or from friends.

The second survey, also in March 2021, was of 2,000 self-employed people. 37% held reserves with a median value of almost £188. The Bank estimates this group hold £1.2-1.5 billion in cash.

There was no correlation between turnover, length of time self-employed or demographics. 64% of those who employed three to five people held cash. 49% of those who did not have employees held no cash. 26% of those who take more than half their payments in cash hold over £1,000.

Compared with three years ago, 16% were holding more cash and 35% less.

The final piece of research was into cash held overseas. The research took place in 2021 across 11 countries. 23% of respondents held sterling with an average sum of £59. 36% held dollars and 35% euros. Respondents had obtained their cash when abroad as tourists (63%), from shops (16%) or as gifts (31%).

Cash drivers during the pandemic

The four drivers of cash use are said to be:

1. The overall level of consumer spending - consumption has been increasing since the end of pandemic restrictions. In the fourth quarter of 2021 consumptions was only 1% lower than in the fourth quarter of 2019. Cash usage has increased but is still lower than pre- pandemic.

2. Online shopping – this rose from 20% of purchases in February 2020 to a peak of 36% in February 2021. In June 2022 it had fallen back to 25% suggesting a small long-term increase in online shopping.

3. Attitudes to cash compared with alternative payment methods - the Bank’s October 2021 survey showed 27% of people using less cash due to hygiene concerns. At the peak, this figure was 39%. Despite significantly less concern about COVID, 56% of people said they were using less cash because they preferred being cashless. This suggests an underlying behavioural shift.

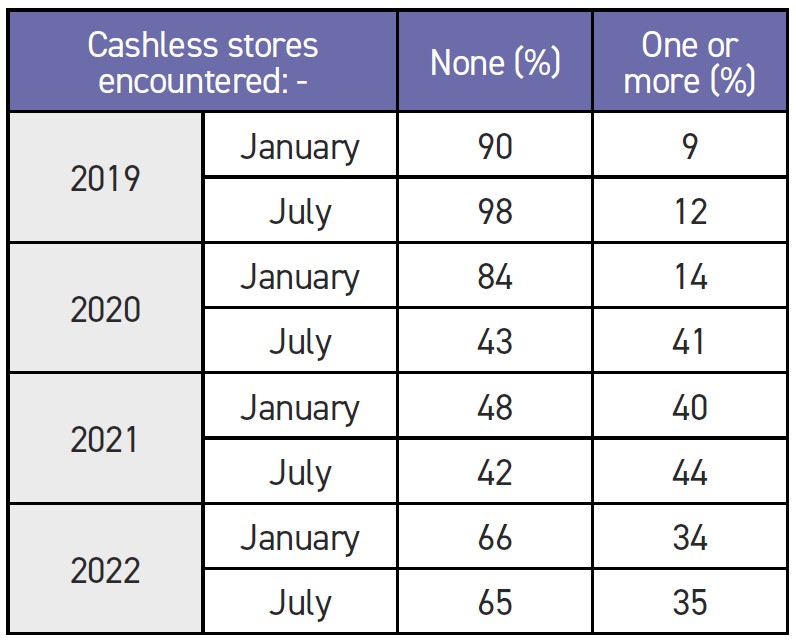

4. Cash acceptance - the Bank interviewed large retailers in the first half of 2022 and found that they were no longer actively encouraging cashless payments. 98% of small business owners accept cash. In July 2021 44% of the public had experienced shops that promoted no cash and in July 2022 this had reduced to 35%.

Overall, these drivers of less cash behaviour have eased since the height of the pandemic but with consumption still slightly lower, online shopping slightly higher, a higher level of ease and willingness to use contactless payments a few stores still declining cash, the decline in cash transactions is not a surprise.

Overall, these drivers of less cash behaviour have eased since the height of the pandemic but with consumption still slightly lower, online shopping slightly higher, a higher level of ease and willingness to use contactless payments a few stores still declining cash, the decline in cash transactions is not a surprise.

The importance of cash

Although cash remains an important form of money for many, the use of cash has stabilised. The Bank does not expect usage to increase.

A number of surveys have shown which are the main groups for whom cash is their first preference payment method:

The elderly (those 65 years old or older) and lower income groups. In the July 2022 survey cash was preferred by 27% compared with 20% in July 2021. Pre- pandemic in January 2020 it had been 38%.

C2/D/E social group, July 2022, 28% preferred cash.

In 2020 the Financial Conduct Authority found the digitally excluded (46%), those with no educational qualifications (31%) and those in poor health (26%) relied on cash. In addition were those with physical or cognitive disabilities.

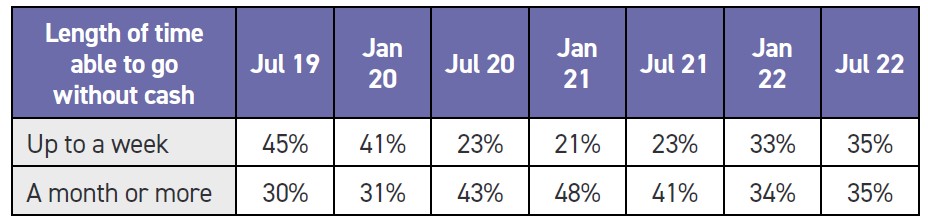

The Bank asked people how long they could go without using cash. While people found they could survive without cash during the pandemic, as the situation returned to something more normal, so results have returned to close to pre- pandemic levels.

It is interesting that fewer people now thing they can go for up to a week without cash than before but, equally, more people think they can go without cash for a month or more. At each end of the spectrum small changes have occurred.

In March 2022 85% of people said that cash was still needed as a back-up payment means.

This section of the report included a summary of the legislative reforms included in the Financial Services and Markets Bill. These are intended to assure access to cash, and they give the Bank the ability to keep the wholesale cash infrastructure effective, sustainable and resilient.

Conclusion

This summary report tells a complex story. The explanation of cash decline during the pandemic holds few surprises but there are some interesting hints of complexity for the future. The NIC figure is now at zero. Will higher interest rates and high inflation see cash held as a store of value return or fall away?

Underlying behaviour and attitudes to contactless payments have shifted. The drivers that lead to less cash continue to point in the wrong direction. Do these pointers suggest that the long-term decline of cash will continue? Is the polarisation hinted at in the figures for those who can only go without cash a week and those a month or longer significant?

Within this context, is the current stabilisation a ‘pause’ before continued decline or have we hit a ‘base’ level of cash usage? Time will tell.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.