Access to Cash: a European Perspective

Cash Essentials recently ran the first in a series of ‘Cash Talks’ looking at access to cash with reports from AGE Platform Europe, the European Retail Payment Board (ERPB), the Dutch National Bank (DNB) and LINK.

Those who need cash

Anne-Sophie Parent is co-chair of the ERPB working group on access to and acceptance of cash. She spoke in her capacity at AGE Platform Europe providing some thoughts on those who need cash and some of the challenges for cash.

Need for cash: She started with some facts about three groups who are not ready for digital payments:

In France, 20% of 15-29 year olds are not confident using digital devices beyond social media.

In the European Union (EU), 40% of 16-74 year olds have no or low digital skills and are unable to cope with digital financial services. This percentage has not changed since 2017.

According to the European Commission’s Retail Payment strategy, there are 30 million unbanked people in Europe.

It is not just the old who are challenged.

Challenges: Although a number of countries have carried out detailed assessments of ATM networks, these are a blunt tool. They do not take account of where people who really ‘need’ cash live, or factors such as whether public transport links are credible.

The pandemic has led not only retailers to move to digital payments only, but public authorities as well. The European Union’s Court of Justice decisions C-422/19 and C-423/19 involving Hessischer Rundfunk found that public authorities ‘can also limit payment option on public interest grounds’. Although this conflicts with accessibility legislation, this has allowed public authorities to move to digital payments.

Conclusion: Anne-Sophie’s conclusion is that you can’t rely on market forces to maintain cash and that legal impositions of minimum coverage levels of ATMs and cashback will be needed. There needs to be a common EU wide measure of ATM coverage and the ECB should regularly survey consumers and retailers about their satisfaction with cash services.

ERPB Working Group report on access to and acceptance of cash

Diederik Bruggink, also a co-chair of the ERPB working group, presented the findings of its 2021 report. The overview is that there is a great variety of initiatives to ensure access to cash across Europe. Access to cash remains though, broadly assured through traditional routes to cash access.

The success of the cash cycle remains based on the profit-cost models in place, sustainability and the service levels of operating ATMs and bank branches. All parties need to work together and co- operate to maintain cash.

Diederik presented on the findings of the working group:

There is now an understanding of the importance of the distance and capacity criteria for cash access points.

Access of rural and ageing populations may need further investigation.

Some EU states have non-binding national plans.

There is a lack of harmonisation of the accessibility requirements stemming from the European Accessibility Act.

If cash infrastructure is in place and working, merchants are happy to work with cash.

Independent ATM Deployers (IADs), cashback and cash in shop solutions are complementary to cash access points, but they are not fully fledged alternatives to ATMs or branches because it is not always possible to deposit coins and banknotes with them.

Post Offices are a successful provider of cash services.

There may be a need to increase incentives to retailers and IADs to encourage them to provide cash services.

More clarity is needed on the notion of the legal tender status of cash. This needs to resolve the conflict between mandatory cash acceptance and contractual freedom of choice about payment acceptance.

There is the need to keep revisiting cash access and acceptance and to determine the appropriate level of cash infrastructure.

The recommendations of the working group were that either a new ERPB working group or a dedicated body needs forming to implement these findings. A study on the societal costs and benefits of different payment instruments in the euro area is needed. This should report in 2023 using 2022 data.

Cash in the Netherlands

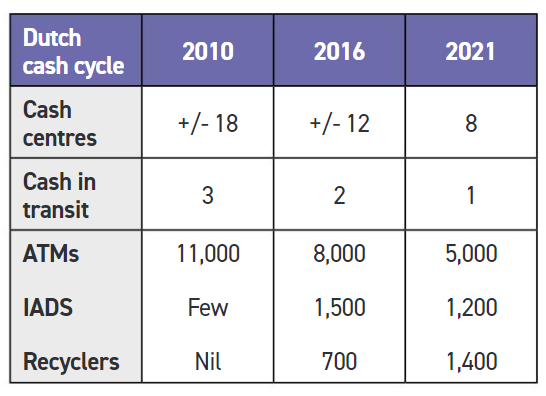

Roel van Anholt from the DNB started by looking at the Dutch changing cash cycle:

As of this year there are no bank owned ATMs with Geldmaat running the ATMs on their behalf. The decline in the number of ATMs over the last three years has been significant. At the end of 2019 there were 6,500, in 2020 5,800 and, 4,900 in 2021.

Despite that, 99.5% of the population have an ATM within 5 km of them.

Cash payments fell to a low of 15% in April 2020 but have now stabilised at 20-25%. 97% of merchants still accept cash.

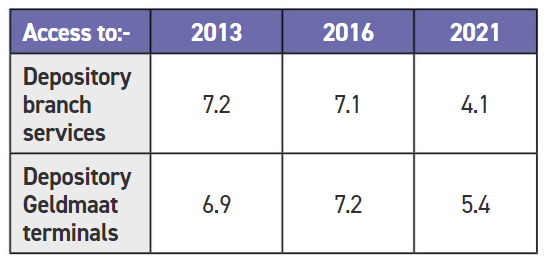

For merchants their perception of their access to cash is rather different:

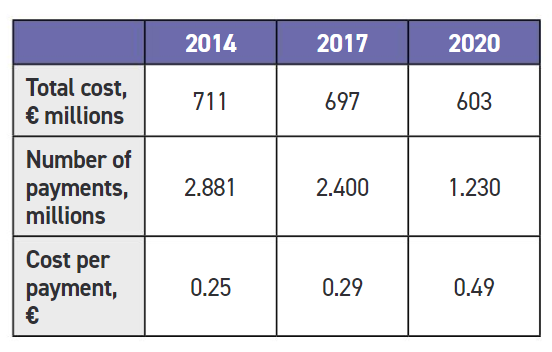

At the same time the cost of retail payments in cash has risen:

Pressure on cash: Cash is under pressure in four areas:

Redundancy has been removed from the ATM network.

In September 2020 ATM availability was less than 90%.

Bankers are increasingly passing costs on to customers.

Merchants are discouraging cash use.

It was this situation that led the DNB in 2021 to ask the consultancy McKinsey to review the provision of cash services.

Covenant on cash

McKinsey came up with four conclusions, three of which the DNB is choosing to pursue through a non-legally binding covenant with cash cycle stakeholders. The conclusions were:

Maintain the ATM infrastructure. Downsizing can only happen after electronic back-ups are in place.

Help cash dependent groups become less dependent.

Ensure acceptance of cash remains high by merchants.

Government to step in if the cash infrastructure falls below a commercially viable level.

The DNB’s concerns about the covenant, if it is actually agreed and put in place, is that it may not last even five years. If cash is not viable, then what legislation will be appropriate? Should banks be required to operate and fund cash infrastructure? Should there be public subsidies to merchants and banks? Should a third party cash provider be put in place?

The second in the series of Cash Talks will be held on 24 March on the topic of Cash and CBDC.

LINK and the UK

The webinar also included a full report from LINK on access to cash activities in the UK but this is covered in the UK access to cash article and so is not reviewed here.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.