News in Brief

Spain Legislates for Cash

At the end of May a new law in Spain made it mandatory for retailers to accept cash, with refusal to accept cash becoming an offence. Under certain conditions it can be regarded as a severe, rather than a minor, offence. Spain has an association for the defence of cash, the Denaria Platform, which has carried out surveys as part of its campaign to maintain access to cash. A survey in September 2021 found 70% of the population consider cash a necessity for society.

Spain imposes a limit on cash payments of €1,000 when one of those involved in the transaction is a business or acting in a professional capacity. The ECB has strongly criticised such limits, most recently in March 2022.

The Denaria Platform wants the cash infrastructure to be designated as Critical National Infrastructure, a maximum distance between ATMs to be set based on geographical, socio-economic and cultural factors and the removal of barriers to cash handling.

New Apps for Cash

The Dutch National Bank (DNB) has made available for Android and Apple mobile phones an app that can be used to authenticate euro banknotes.

Perhaps unsurprisingly, no indication is given about how it works, but it joins Koenig and Bauer Banknote Solutions (KBBS) with their banknote authentication app Valicash™ as a solution available for free to the public.

KBBS has also launched the SMILL™ app. SMILL allows people, organisations or governments to load an image onto a banknote which is either publicly or privately available. No user profile is required to use the app and content is created without asking for personal data.

The marketing and brand potential is enormous far outside of the banknote world. Equally a central bank could load security feature information or a government public information onto banknotes, even tourist messages for banknotes being supplied overseas.

Removing Canada’s One Cent Coin

As countries such as Estonia consider ceasing use of the once cent coin, it is coming up to ten years since Canada had its one cent coin.

A recent survey by Research Co found 71% of the public did not miss the one cent coin, with 19% disagreeing. Those aged 35-64 years old missed it most with only 65% supporting its abolishment while older people were 72% in favour. British Colombia was most wedded to the one cent, again with 65% supporting its abolishment.

Focus has now moved to the five cent coin, with 40% supporting its removal but 49% having reservations. Unlike the one cent coin, the face value is still higher than the cost of production. No plans have been announced.

SARB Maintains Denominational Mix

The South African Reserve Bank (SARB) has recently commented about options for its denominational structure. The highest denomination is the R200 but there is no pressure to introduce a higher value note given that the R100, rather than the R200, is the most used note. The R200 is fulfilling a store of value function. Between March 2020 and June 2021, there were an average of 307.3 million R200’s and 776.6 million R100’s in circulation.

A SARB study has concluded that there is an economic case to issue an R10 coin, but that the public is not keen on the idea. Public perception, along with the buying power of the rand and general inflation trends, is an important factor in the decision for change.

Using Cryptocurrencies to Access Cash

Whatever one thinks of cryptocurrencies and the blockchain, those advocating the use of cash will be pleased to see that MoneyGram, who is developing digital person-to-person (P2P) payments, and the Stellar Development Foundation (SDF), an open-source public blockchain designed to allow money to be tokenised and transferred around the world, are working together to allow cryptocurrencies to be sent and then turned into cash by the receiver.

MoneyGram and SDF formed a partnership in October 2021 and the new service is available in Canada, Kenya, the Philippines and the US. By the end of June this cash-in service should be available in seven countries with cash-out functionality available globally where allowed by law. To make these remittances people will need a Stellar-enabled digital wallet, access to MoneyGram’s retail agent network and to hold Circle’s USD Coin (USDC). USDC is a fully- reserved dollar digital currency.

Settlement will occur in near real-time, which should improve efficiencies and reduce risks as well as speeding up the collection of funds. Users will not require a bank account or credit card.

For the first 12 months, MoneyGram is offering this service without charging a service fee.

Financial Inclusion Remains a Challenge in Mexico

Counter-intuitively Mexico’s National Inclusion Report (ENIF) reports a fall in financial inclusion. While cash continues to dominate, used for 90% of transactions under 500 pesos ($25) and 78.7% of payments over 500 pesos, the number of people with at least one financial product fell by half a percent to 67.8%.

‘Counter-intuitive’ because of Mexico’s vibrant ‘pro-inclusion’ fintech scene, which has seen products such as Klar, Kueski Pay, Stori and Albo come to market offering no-fee banking or easy ways to sign up.

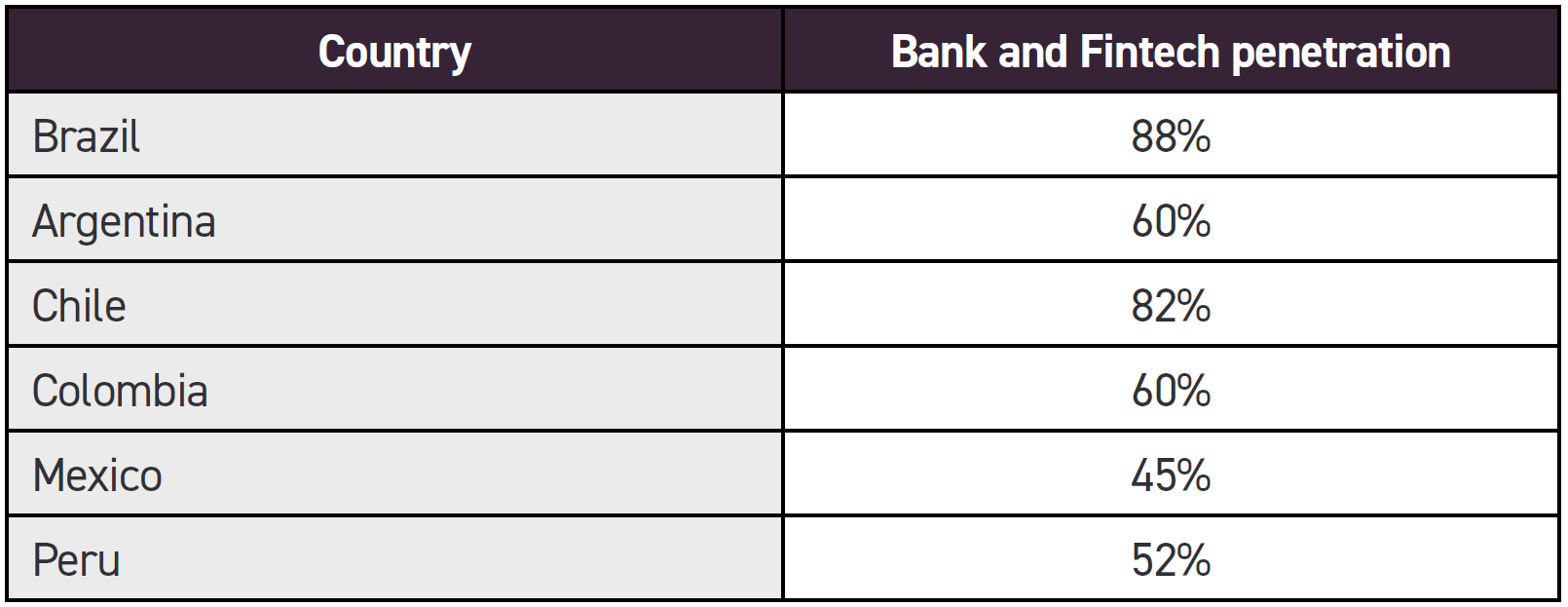

Latam bank and fintech penetration (Source: Americas Market Intelligence).

Latam bank and fintech penetration (Source: Americas Market Intelligence).These figures put Mexico behind similar economies, such as India and Brazil, for inclusion and reliance on cash.

One hypothesis is that the fintechs are targeting the metropolitan elite rather than the poorer, rural communities who lack the necessary banking infrastructure. The fintechs argue they need more regulatory support if they are to make an impact. Revolut’s Mexico CEO suggests that more digital players need to be licensed as banks to make progress.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.