CBDCs: An Insurance Policy or a Necessity?

The Central Bank Digital Currency (CBDC) conference took place at the very end of August in Frankfurt, the first CBDC conference in person reflecting just how new CBDCs are.

A big question recurring throughout the conference was what is the benefit of issuing a CBDC? There appear to be two communities. Those who either lack elements of a modern payment infrastructure and/or for whom financial inclusion is a problem, and countries for whom concerns about the sovereignty of their money supply is an issue.

For this second group the user case is more ambiguous. There seemed to be a sense that money itself is changing and there is the potential for central banks to lose control of the nation’s money, with all the implications for monetary policy that would bring.

A CBDC could be regarded as an insurance policy against an undefined risk. Insurance policies are expensive, until you need them when the suddenly become good value. Given the lack of definition of the risk and the need for the insurance policy to be watertight, central banks will take the time necessary to design and test their CBDCs, which is why five years was the earliest forecast for one being introduced into this group.

Who was there?

33 central banks and 58 central bankers attended with Europe (14 central banks) and Africa (8) best represented. The attendees included all nearly all the countries who are piloting or have launched a CBDC, with China being the major exception, so there was real knowledge and experience attending. The majority of the focus was on retail CBDCs although cross-border payments received significant attention.

The programme included the Bank for International Settlements (BIS) and a number of speakers active in their innovation hubs. Jamaica, Zambia, Nigeria, Kazakhstan, Ghana, the Bahamas, Sweden, Israel and Thailand all spoke about their work. Sadly, technology issues meant South Africa and the Federal Reserve were not heard.

Alongside the central banks were a wide range of suppliers, for example Bitt whose product is used in Nigeria, G+D who Ghana is using for their pilot, nChain, Amazon Web Services, Emtech and Ripple.

Digital Euro Association: user needs

The conference started with a series of master classes as an introduction.

Sensibly the Digital Euro Association (DEA) started by considering potential user needs. A CBDC could or should be a default resistant digital money, an independent, autonomous payment system, usable for cash-like private payments, capable of online and offline payments, offering money and payments the ability to be programmable and allowing cheaper and faster payments, including cross-border payments. The list went on.

With such a long list, the DEA suggested the starting point was to find a user case first and to tackle specific user needs. Central banks need to apply a user-centric perspective to the design of the CBDC.

When this is done, the key question is – are the features sufficiently useful to ensure the CBDC receives a high adoption and usage rate by consumers and merchants? This question came up consistently through the conference.

Only then should the central bank consider the underlying technology. Part of all this has to be an international dimension given the benefits offered for cross-border payments.

Their final advice was to ensure your prototypes consider different technologies.

SICPA’S Brazil research

Fitting neatly with the DEA’s statement about the importance of applying a user-centric perspective, SICPA had commissioned research in Brazil with Finthropology on payment choice and behaviour as part of designing a CBDC based on user needs. It found that technology literacy was often a technology issue rather than a literacy issue. Equally people are more financially literate than we think.

In Brazil 74% of people have identity documents and 40% of those surveyed in the rural and the urban surveys carried out had three or more accounts. On the other hand, access is not a proxy for usage. Perhaps it is an effect of Brazil’s Pix payment system, but people still tend to use accounts belonging to family members for payment.

The surveys found few patterns. Choice is individualised, indicating that there are gaps in people’s financial tool kits. If new tools existed, people would find ways to use them if they were useful to them.

Finally, what was important to the public was access, user privacy, being able to access service, payment recoverability and added functional value to overcome existing payment pain points.

Learning from the Sand Dollar

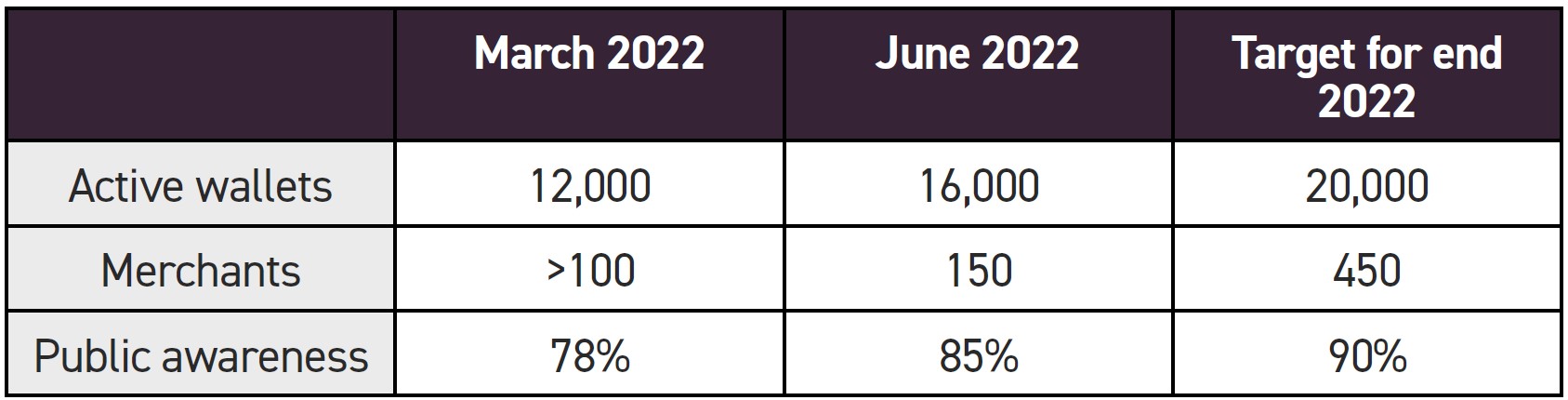

The Sand Dollar, issued by the Central Bank of the Bahamas, has been circulating since October 2020 and this presentation reviewed the challenges it is facing and what is being done to promote its use.

Currently there is a low volume of Sand Dollars in circulation, accompanied by low merchant activity. The Sand Dollar is not visible in government. On the other hand, research shows an appetite for information about it amongst the population.

Population, 410,000 people.

Population, 410,000 people.Clearly, launching in a pandemic has not helped and this curtailed the planned outreach programme, including training merchants and staff at the Bank. There have been technical challenges and the need to harmonise policies and protocols for participating Authorised Financial Institutions (AFIs) has been identified.

Technical updates. The Bank has embarked on a programme of updates to provide more functionality and make it easier to use. The integration of bank accounts into the Automatic Clearing House (ACH) system allows money to be transferred from mobile banking apps to wallets. New enhancements have been commissioned to allow an offline capability, electronic know your money and self-on boarding modules. Commercial banks are being re-engaged with the goal of allowing sequenced, gradual entry in the third quarter.

Push for adoption. Alongside the updates, the Bank is having a push for adoption. It has established an adoption unit within the Bank, hired an external public relations consultancy and set up an online sign-up platform for merchants.

A budget of $1 million has been put aside for giveaways, merchant fee discounts, festival sponsorship and island family outreach programmes.

The Central Bank is planning education programmes for Members of Parliament and the school system. It wants the policy on access to data to ensure Sand Dollar payments are zero rated on cell phone networks and that data access points exist to allow better and lower cost connectivity.

Consumer and merchant engagement. Considerable work has been done on reaching the unbanked, underbanked, the fintech community and young professionals. New target groups have been identified, notably family island groups, students, public transport passengers and transient entrants. New programmes to reach these groups are now being planned.

One focus has been identifying the unique selling points of the Sand Dollar for consumers and merchants. For merchants these are that the Sand Dollar is low cost, secure, trackable, efficient, immediate and offering final settlement.

For consumers it offers convenient, easy access to cash, it is inclusive, secure, contactless and allows the easy transfer of money. The Central Bank believes it offers these benefits better than the available alternatives.

Government engagement. The Central Bank is looking to engage the Post Office, passport issuing office, inland revenue, national insurance board, department for road traffic and the court system so that all of them accept payments using Sand Dollars.

Final word

Reviewing a handful of presentations can only give a snapshot of the conference. But even these pull out some key messages starting with the DEA’s question, are the features sufficiently useful to ensure the CBDC receives a high adoption and usage rate by consumers and merchants?

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.