Cash Use Rises in the UK

For the first time in years, cash usage has risen in the UK, and not by a small percentage. The British Retail Consortium (BRC) conducts an annual Payments Survey which covers 35% of the UK’s retailers, and this is the first time since it started the survey in 2013 that it has seen an increase.

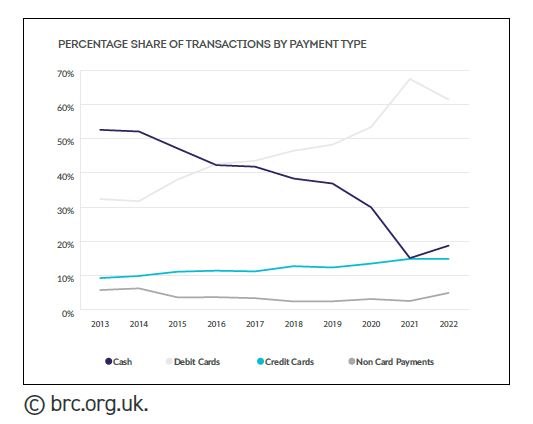

While card payments fell from 83% of transactions at the point of sale in 2021 to 76% in 2022, cash rose from 15% to 19%. By value, cash rose from 8% to 11% over the same period.

In 2020, cash transactions were 30% of the total number of cash transactions.

Financial pressure

Evidence that consumers are under financial pressure is that the average transaction value fell from £24.49 to £22.43, and the need to budget is given as the driver for increased cash usage. Credit card spend fell from £33.49 in 2021 to £30.57 in 2022, the lowest value recorded, and the debit card transaction average fell from £25.11 to £23.39.

Other evidence of consumers managing their payments differently is that the number of transactions has gone up and the use of, buy now, pay later, loans and open banking payments has risen from 2% in 2021 to 4.9% in 2023.

Total merchant service charges

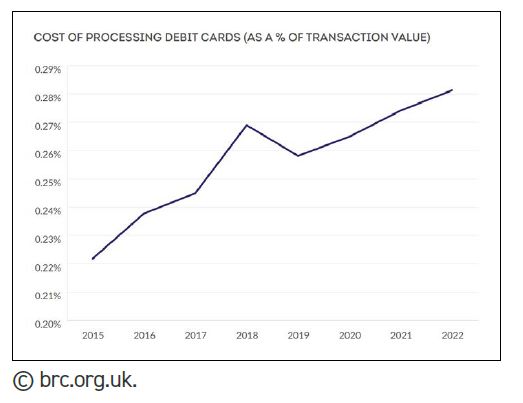

BRC also found that card fees have continued to rise. Retailers spent £1.26 billion on card processing fees. Scheme fees have risen 27%1 and interchange fees rose 7% as a percentage of turnover2. Total merchant service charges rose 13% year- on-year.

Unsurprisingly, the BRC wants the UK’s Payment Systems Regulator to make reforms to increase competition and reduce payment market costs. It also wants a Treasury review of interchange fees, and it wants open banking to grow but without replicating the existing card system.

Commercial card processing fees

Commercial card processing costs are out of scope of the caps set by the Interchange Fee Regulation (IFR). BRC regards the 36% increase in commercial interchange fees year-on-year, measured as a percentage of turnover, as opportunistic. Expressed in pence per transaction, these fees rose from 17.2 pence in 2021, to 30.69 pence in 2022. This is felt particularly acutely by retailers with large numbers of low value card transactions.

It is ironic that at the same time, the UK has seen over 600 bank branches close in 2023 and, in November, Barclays announced it will close 34 branches, and Lloyds Banking Group 120 branches, in 2024.

Future of cash

BRC members have concerns about the long-term sustainability of the cash ecosystem in the context of increasing logistical challenges created by lower demand. Survey respondents said they still accepted cash, albeit the survey did not capture every type of retailer, for example small businesses or the hospitality sector. 11% of respondents do not accept £50 notes.

For retailers with self-service check outs, 89% accepted cash in at least some of these machines. However, for some of them cash acceptance was as low as 15% of shops.

BRC’s report said, ‘the government should consider further interventions to support a sustainable future for cash; these should focus on ensuring cash acceptance is a viable option for merchants across the whole ecosystem.’

Final word

While the BRC has a positive headline for cash, the report also outlines future challenges and structural weaknesses. The cost of digital payments could not be clearer and, at the same time, the underlying value to society of cash is evident.

1 Scheme fees – fees paid by retailers to the card schemes

2 Interchange fees – fees paid by retailers to the issuing companies e.g. Barclaycard, Santander, Capital One. The rates paid are set by the card schemes, which are payment networks eg. Visa, Mastercard and American Express).

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.