From Merchant to Consumer: a Payment Overview

The Bank of Canada (BOC) has published two survey reports in the last few months.

The first was the Methods of Payment (MOP) survey 2021 1 and the second the Merchant Acceptance Survey (MAS) Pilot Study 2. These surveys cover the payment stakeholder spectrum and offer, therefore, an interesting overview of changing payment dynamics.

MAS survey pilot study

The MAS is important because it provides data on what is happening to merchant cash acceptance and payment trends. An MAS was carried out in 2018 but the pandemic disrupted the normal schedule. This MAS is also an opportunity for BOC to understand the conditions for the potential issue of a CBDC.

Acceptance of different payment methods depends on the size of merchants, the industry and region. This version of the MAS was slightly different in that it targeted small and medium size businesses (SMBs), namely businesses with up to 49 staff.

The survey focused on three sectors – retail/food services/drinking places, and an ‘other’ group such as personal services and repair shops. It looked at results in five regions – British Colombia, the Prairies, Ontario, Quebec and Atlantic Canada.

The survey took place in two parts, late 2021 and then early 2022. The MAS wanted to see to what extent the pandemic had changed payments and, as part of that, how the use of contactless cards and Canada’s Interac e-transfer payment tool had changed things.

Deputy Governor Tim Lane had made a speech in 2020 which gave two scenarios which could lead to Canada issuing a CBDC:

The use of physical cash reduces or is eliminated

Private digital currencies see more widespread use as a method of payment, store of value and unit of account.

Observations on MAS

On the one hand, consumers can only use the payment method accepted by merchants. On the other, merchants can only serve consumers who have, and choose to use, those accepted payment methods.

Widespread use of a payment method critically depends on consumers knowing that they can use it at stores where they shop. Merchant acceptance is, therefore, critical.

MAS looks at how merchants contribute to the cash cycle and cash and payment demand, including looking at cash access points (automatic banknote machines (ABMs) and bank branches). Access was robust during the pandemic, but merchant acceptance is a less understood area.

Findings

When it comes to cash, the size of the organisation makes little difference, but it is very different for small businesses (five employees) and medium businesses (up to 49).

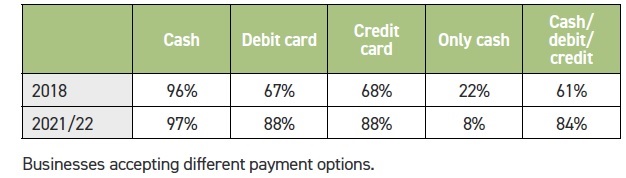

In 2018 31% of small business were cash only, now the figure is 10%. Medium size businesses have remained unchanged.

92% of merchants expect to continue accepting cash. This is perhaps unsurprising given the finding that 79% of consumers do not expect to go cashless.

Cards: Debit and credit card acceptance increased by 30 percentage points for small businesses between 2018 and 2021/22 but only 5% and 2% respectively for debit and credit cards for medium size businesses. 86% and 94% of small and medium-sized businesses now accept debit cards and 87% and 92% credit cards respectively. Increasingly consumers know they can use cards if they wish to, as well as cash.

Card acceptance increased across the different business sectors surveyed, although providers of ‘other services’ saw a lower level of increase, albeit a significant one (from 23% in 2015 to 81% for debit and 82% credit cards).

There were some quite big regional differences relating to stores that only accepted cards. Quebec, for example, had 15% of stores card only, whereas Atlantic Canada had none.

Of the 88% of businesses who accepted card payments, 81% now accept contactless payments. Larger merchants and accommodation and food service businesses are more likely to accept them.

Cheques: Cheque acceptance increased from 34% in 2018 to 54% in 2021/22, but this is still less than the 2015 figure of 64%.

e-transfer: Interac e-transfer acceptance rose to 60% from 36%, although food services and drinking places lagged at 45%. The 2021 Cash Alternatives Survey found that 42% of Canadians had made an e-transfer in the last week, so this acceptance increase is perhaps not surprising.

Mobile payment apps: Apps were 15% in 2015, 18% in 2018 and 43% in 2021/22. This appears to be a response to consumer demand.

Merchant assessment of different payment methods

Only 60 merchants gave their opinion on different payment methods and this is an area that will be expanded in future. The questions rated costs, fees, speed, fraud risk and reliability.

Debit cards: lowest labour cost, lowest fraud risk

Cash: fastest, most reliable, lowest fees

Credit cards: the least favourable payment option in all areas.

The paper said that merchant acceptance was critical to enabling widespread use of payment methods. It is significant then that while SMB merchants are committed to accepting cash, over the last 3-4 years their ability to accept alternative payment options has increased markedly. The sector and regional variations are significant, but they do not negate this reality.

Headline findings of the MOP survey 2021

BOC has carried out its consumer focused survey and three day payment diary MOP survey every four years since 2009. It published the results of its 2021 MOP at the very end of 2022 with five key findings.

Reduction in the number of cash payments, but stable dollar value

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.