European Cash Fundamentals on the Move

The European Central Bank (ECB) has reported on its Study on the Payment Attitudes of Consumers in the Euro Area (SPACE) 2022.

While payment behaviour varies significantly across Europe, the trend is clear, a move away from cash. On the other hand, there is also a clear change in people’s understanding about the value and importance of cash.

Key observations

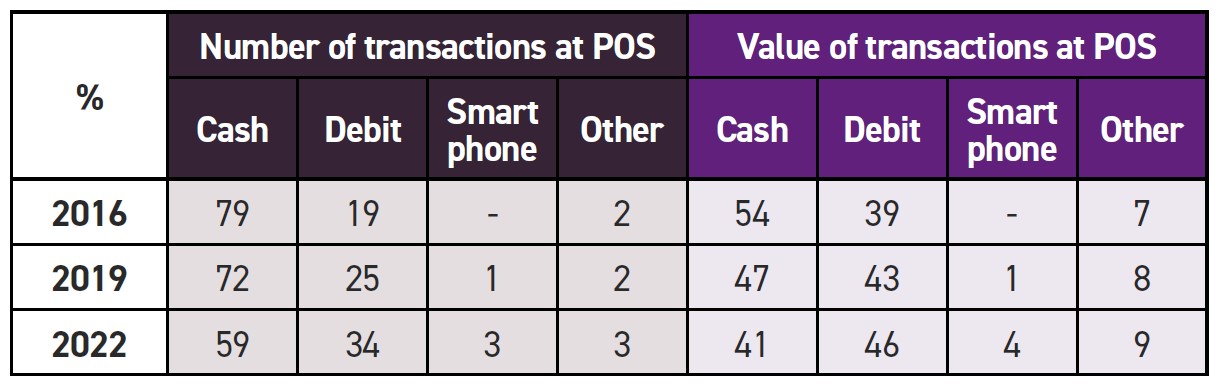

Cash was used for most consumer payments, but its share decreased to 59%.

The share of electronic payments rose, including day to day and online payments.

Consumers prefer to pay electronically but value cash as an option. Those regarding having the option to pay in cash as important increased from 55% in 2019 to 60% in 2022.

Cash is used for low value payments in store and person-to-person (P2P).

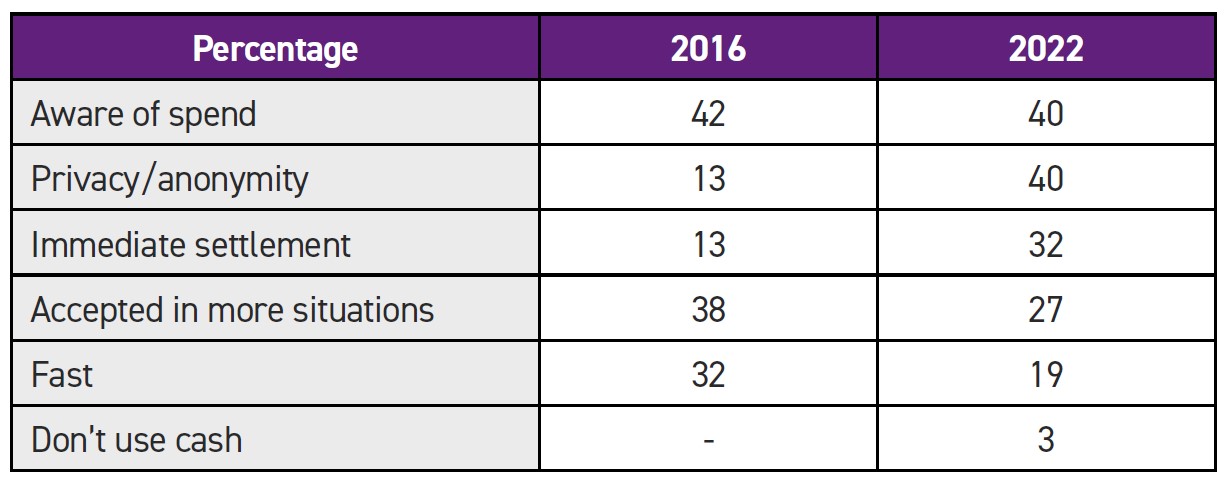

Cash is seen as valuable as a way to remain aware of expenditure (40%), to protect privacy (40%) and to allow immediate settlement (32%).

Overall people were satisfied that they could access cash.

Organisation of the survey

In 2016 the ECB ran a study on the use of cash by households (SUCH). In 2019 it ran its first SPACE survey, and this was repeated in 2021/22. Although the SUCH survey was different, many of the results are appropriate to compare with the SPACE surveys.

In addition to the questions used in 2019, the 2022 SPACE survey set out to understand changes since the start of the pandemic, to look at recent trends in digital payments, such as instant payments, and to investigate the ownership and use of crypto assets.

The SPACE survey was conducted in 17 Eurosystem countries involving 39,765 people. 40% of the interviews were conducted between 2 October and 7 December 2021 and the balance between 17 March and 9 June 2022.

In addition, the Bundesbank (BBk) and the Dutch National Bank (DNB) conducted separate but similar studies. The BBk’s survey was between 8 September and 5 December 2021 and the DNB’s in the fourth quarter of 2021 and the first quarter of 2022.

Clearly the pandemic had a major impact on the results, even though lockdowns were not in place when they took place and virtually all restrictions had been lifted. It cannot be certain, therefore, whether the changes noted may not yet reverse themselves.

Impact of the pandemic

When asked why their payment habits had changed it was clear that the pandemic had played a significant role. The following reasons were given for paying with less cash:

Strongly advised not to pay in cash – 42%

Government recommendation – 29%

Fear of virus infection – 26%

Cash not accepted – 9%

Less easy to withdraw cash – 8%.

On the other hand, reasons for paying electronically were:

Electronic more convenient – 58%

Discovered other means of payment – 14%.

It will be interesting to see whether the positives for electronic payment are more long lasting than the pandemic drivers that now don’t apply.

54% of those surveyed reported no change in their cash use before or after the pandemic. 32% reported a decrease made up of 17% somewhat less and 15% much less. This explains the fall in cash use from 72% in 2019 to 59% in 2022. Perhaps surprisingly, 8% of people use somewhat more cash and 6% much more.

2020 data collected in the IMPACT survey during the pandemic said that the availability of non-cash payment methods was the biggest reason for the move to less cash, which also underlines the importance of merchants being able to accept alternative payment methods.

Interestingly, it was still only possible to pay with non-cash means for 81% of transactions. This is up 2% on 2019. This is, perhaps, a lower than expected figure and a surprisingly low increase given the changes driven by the pandemic.

Where people pay

For non-recurring payments, 80% are at the point of sale (POS), 17% are online and 4% are person-to-person.

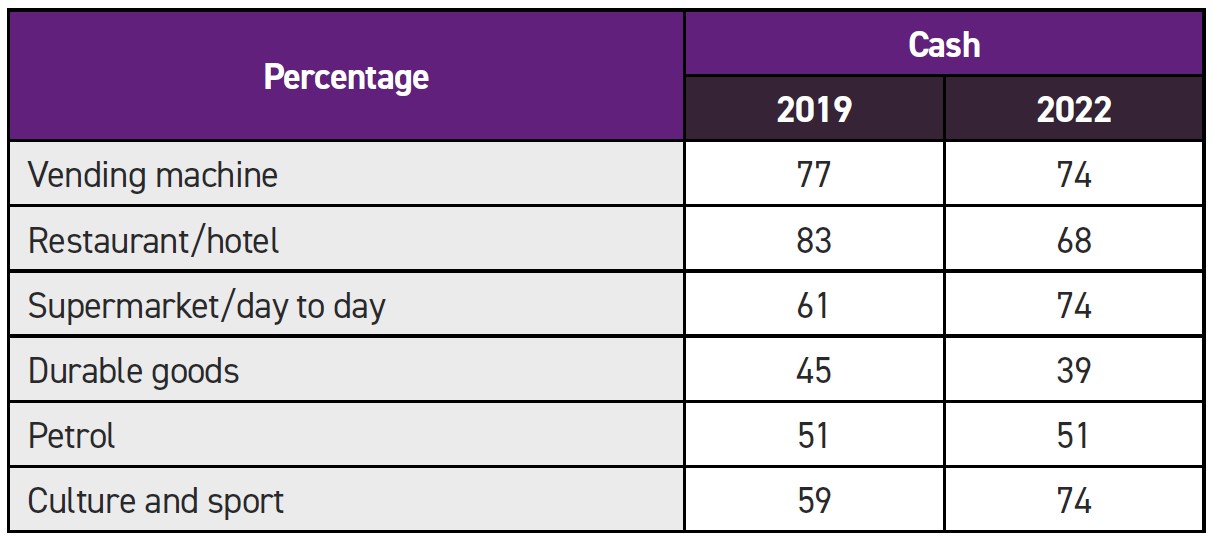

For the POS transactions, 54% are made at supermarkets or for day-to-day purchases and 18% in restaurants, cafes and hotels. These figures are largely unchanged compared with 2019.

The use of cash at the POS declined between 2019 and 2022.

Acceptance of cash at the point of sale (POS) has fallen from 98% in 2019 to 95% in 2022, falling in all countries other than the Netherlands. Although not a conclusion in the report, this is likely to be a contributor to the decline in cash usage rather than caused by it.

Mobile apps were used for around 3-5% of transactions. At the POS they increased from less than 1% in 2019 to 3% in 2022.

How people pay

In 2019 6% of non-recurring purchases were made online, in 2022, 17%. This reflects, of course, the significant change in behaviour initiated by the pandemic.

At the POS, card usage increased from 25% in 2019 to 34% in 2022, mainly contactless payments. Although not a conclusion in the report this is, perhaps, explained by the preference for people to use cash when buying low value items. Electronic payment methods were found to be faster, easier and avoided people having to have large cash holdings.

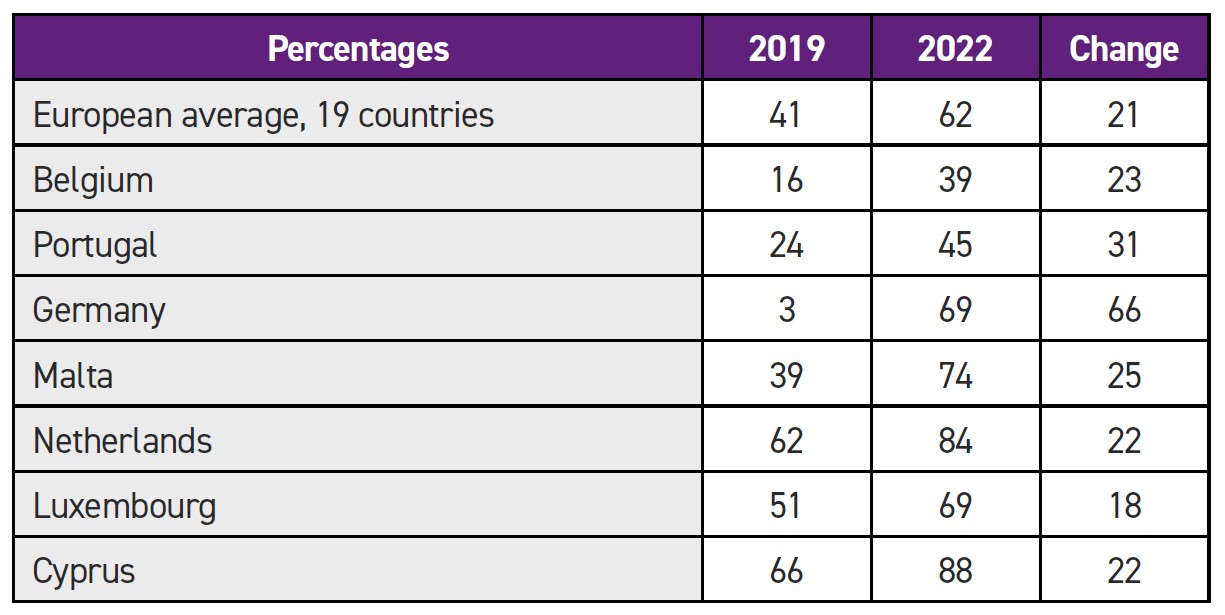

The number of contactless transactions increased from 41% in 2019 to 62% in 2022.

In shops 55% preferred to pay with cards or other contactless payment means, 22% with cash and 23% were undecided. The undecided percentage feels like a big number. The result is neatly mirrored by the ECB’s company survey1 which found that the percentage of companies preferring cash payments was 24%, with card payments preferred by 53%.

Perception of the advantages of different payment types

The perceived advantage of cash was its privacy, anonymity and the immediate awareness of how much has been spent.

It is interesting to see privacy and anonymity and immediate settlement increase in importance. The decline in acceptance in more situations is perhaps unsurprising given the pandemic. The change in the appreciation of speed may be linked to the experience of contactless payments, although this was not a conclusion of the report.

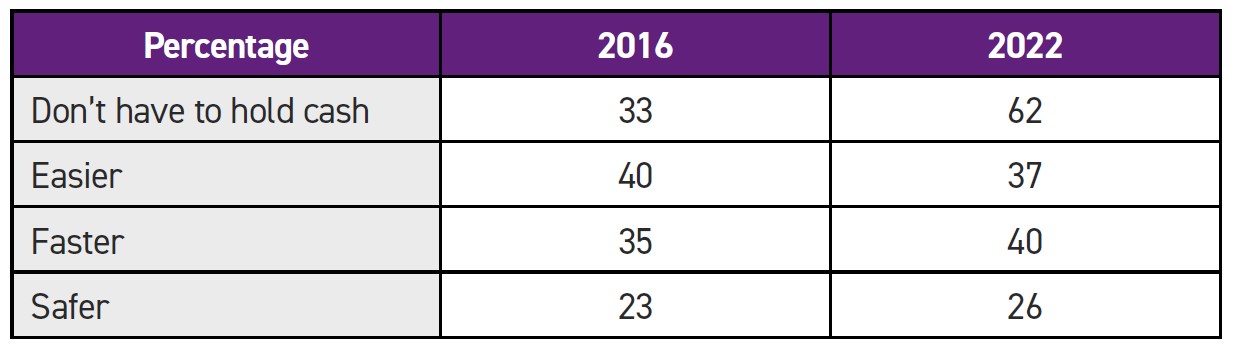

For cards, the big change between 2016 and 2022 was not having to have large cash holdings.

In the 2020 IMPACT study data collected during the pandemic, 45% said digital payment was more convenient than paying cash but this figure has increased to 58% in this survey. Convenience remains the most significant advantage of cards.

How people pay: cash

In only Luxembourg, the Netherlands and Finland were the number of cash transactions less than 40% of the total. When citizens in those countries were asked whether it was important or very important to have the option to pay in cash, 51% of those in Luxembourg, 46% in the Netherlands and 57% in Finland agreed.

In seven countries the value of cash payments was 50% or over of the total (and in Italy the figure was 49% and in Greece 48%).

The number of cash transactions had fallen in Lithuania (-5%), France (-7%) and Austria (-9%). In Estonia they were unchanged. In all the other countries the decline in the number of cash transactions was double digit. Cyprus had the largest fall, -23%.

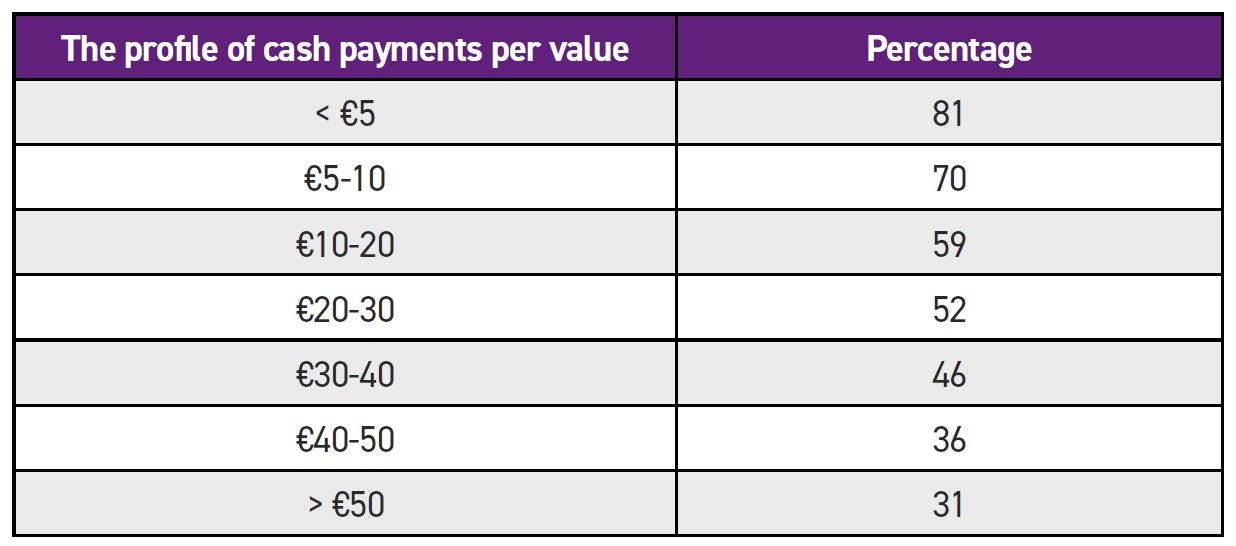

While more than 25% of online payments are for a value over €50, 60% of POS payments are for under €20.

How people prefer to pay

Age is often said to be a divide when it comes to using cash. When asked about their preferences, there was a ten point divide between 18-24 year olds (54%) and 55-64 year olds (64%).

The general preference at the POS for cash payments has dropped 5%. In 2016 the figure was 32%, in 2019 27% and in 2022 22%. Within these averages there are significant variations. Nine countries had a preference less than 22% with Finland, at 7%, the lowest. Ten countries had a higher preference with Austria, at 45%, the highest.

In five countries the preference actually rose:

Belgium, +9%

Estonia, +7%

France, +5%

Austria, +3%

Slovenia, +2%.

Access to cash

74% of people used ATMs to get their cash and only 6% bank branches. Since 37% of people said that they keep cash at home, separate from that which is in their wallets, it is perhaps not surprising that 11% used their reserves to access cash.

90% of people found cash fairly easy or very easy to get, almost the same figure as in 2019 when it was 89%. 50% found it very easy, 39% easy, 7% fairly difficult and only 3% very difficult. In three countries getting cash had become harder – Belgium (12% increase), Netherlands and Luxembourg (both 7%). That both Belgium and the Netherlands have moved to a utility model ATM networks for the organisation of their utility model may be a coincidence.

Over half of Europeans pay no ATM fees to withdraw cash (59%), but 11% either always do or do most of the time.

The use of cashback across all countries was extremely low.

The average sum of money in wallets and purses was €83. Citizens of seven countries held less, with the Netherlands the least at €46. 12 held more, with Austria the highest at €121. 85% of people did not receive regular income paid in cash, slightly less than the 2019 figure of 87%.

How people pay

Electronic payments. 94% of people have access to a payment card and 91% have access to an account for payments. There is little difference in these figures between those who live in rural or urban areas or between people with different levels of educational attainment.

Contactless payments. Seven out of the 19 countries saw a rise in contactless payments over 20%. Germany saw the biggest change.

The move to contactless appears entrenched in many countries, where it has become so dominant that it feels unlikely that it will change back.

Credit card transactions. The number of online non-recurring payments made by credit cards was unusually high in five countries compared with the average which was 6%. No explanation is offered for these differences.

Finland, 33%

Estonia, 23%

Latvia, 20%

Lithuania, 16%

Luxembourg, 16%.

Cryptocurrency. Crypto currency ownership is 4% but it is held primarily as an investment and is seldom used for transactions.

Final word

Online payments are rising. People now have experience of electronic payments and the convenience is valued. Contactless payments are hugely popular.

Cash remains very widely used and its strengths are clearly understood and valued. People carry it in their wallets and store it at home. Access to cash is good, although the decline in ease of ATM access in the Netherlands and Belgium brings concerns about the utility model of access to cash.

1 - Use of cash by companies in the euro area (europa.eu).

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.