Payment News

Prepaid Debit Cards Rush Ahead

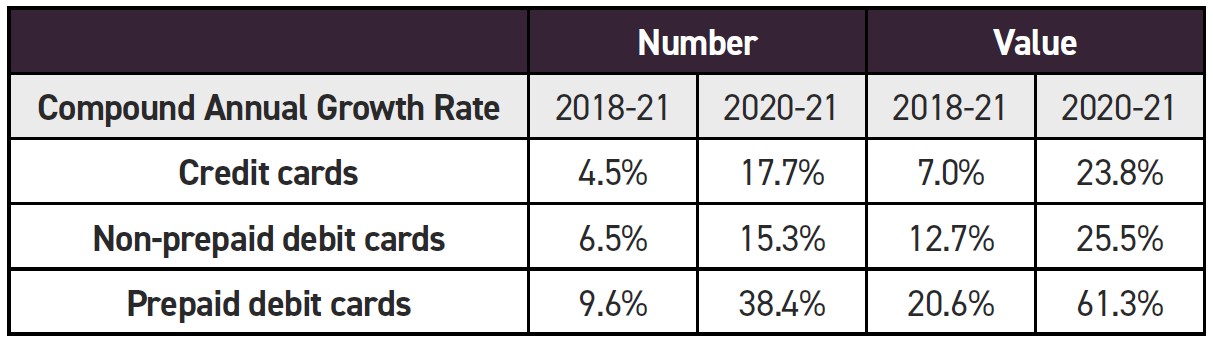

The latest Federal Reserve Payments Study shows an annual 6.2% increase in the number of card payments between 2018 and 2021. Behind that figure there are fluctuations, a fall in 2020 being offset by a rise in 2021, for example. In 2021 the growth in payments using prepaid debit cards was exceptional, all be it from a lower base than the others. In 2020 only 10% of payment transactions were made by pre-paid cards.

The Atlanta Fed, who wrote about this in a blog, does not speculate but one has to wonder about drivers such as the rise of people wanting to participate in ecommerce driving this change. If it had been 2022, we might be thinking about budgeting in difficult economic conditions.

Apple Card Scoops $1 Billion in Deposits

The thought that Facebook might accept payments with its Diem project was an important element in the interest in CBDCs. The reach of a tech giant to reach billions of people was seen as a risk to the entire payment system. The launch of the Apple Card savings account may show whether these fears were correct.

Apple Card savings accounts are held by Goldman Sachs, paying a 4.15% interest rate. American users who open an account can manage it from their Apple Wallet and incur no fees, and don’t have to have a minimum deposit or hold a minimum balance.

Apple has a cash feature that gives customers up to 3% cash back on purchases of Apple products. Any funds earned will be deposited automatically into the Apple Card savings account.

Whether it is trust in Apple and/or the rate of interest, in the first four days after launch nearly $1 billion was deposited with 240,000 accounts opened. The run of banks crashing in the US may also be part of the story.

Safaricom Keeps Innovating

Safaricom is about to launch a new payment option based on its M-Pesa mobile payment platform. People will be able to use a QR code to make a payment and Safaricom claims this will reduce the process risk of mis-entering payment details. To do this, it has had to partner with payment service providers, banks and card schemes to be able to offer ‘ScanUlipe’.

In November 2022 Safaricom introduced M-Pesa Go, which allows subscribers to send and receive money, purchase airtime and bundles, use Lipa n M-Pesa services and access the M-Pesa Super App. M-Pesa Go is specifically aimed at 10-17 year olds. It wants to catch the new generation of users.

India Uses G20 Presidency to Promote DPI for Payments

India is currently president of the G20. It is reported to be promoting its digital public infrastructure (DPI), Unified Payments Interface (UPI), Aadhaar identification system etc. UPI has recently been linked in real time with Singapore’s PayNow system. Visa and Mastercard are competitors and questions have been raised around governance, particularly privacy.

The G20 has formed a Task Force to work on Digital Public Infrastructure for Economic Transformation, Financial Inclusion and Development.

The NPCI International Payments Limited (NIPL) is working to enable cross-border acceptance of UPI. In addition to Singapore, the Indian payment system has gained acceptance in the United Arab Emirates (UAE), Mauritius, Nepal and Bhutan.

India’s promotes the fact that its DPI has open standards and interoperability. It is striving to create awareness of DPI, putting together a fund, either through the G20 or international institutions, and putting in place some form of global institutional structure. It sees this as a key task for the G20 Task Force.

Cash a Target for New Strategic Partnership in France

Worldline, a global leader in payment services, and Crédit Agricole Group, the leading French retail bank, have formed a strategic long-term partnership with the aim of creating a joint company which will be up and running by 2025. It will combine the merchant acquiring footprint of the bank in France with Worldline’s technology and global infrastructure.

The reason? While being a major payment player in Europe’s largest continental payment market is attractive, the press release is specific about the opportunity to grow market volume by reducing the use of cash. Cash penetration is still about 40% of payment volumes.

Spain’s Push to Digital Bearing Fruit

Data from GlobalData research shows that in 2021, 57.3% of payment volume in Spain was in cash. Alongside this positive figure is the compound annual growth rate (CAGR) for card payment volumes 2017-21 of 10%. The frequency of card use rose from 62.2 times per card per year to 82.5 during this period.

The Spanish government is keen for electronic payments to increase, which is perhaps why it was happy to allow the creation of Sistema de Tarjetas y Medios de Pagos (Sistemapay, also known as STMP) in February 2018 through the merger of Spain’s three domestic schemes: ServiRed, Sistema 4B, and EURO 6000.

STMP is the domestic card scheme with a monopoly across debit, credit, and charge cards. Post-merger, all local cards are issued by Sistemapay. To enable international usage, nearly all cards are co- badged with international schemes such as Visa and Mastercard.

According to Banco de España, nearly 83% of in-store card and mobile payments were contactless in 2020, compared to 78% in 2019. On 20 March 2020, the contactless payment limit increased from €20 to €50. As elsewhere, this resulted in a further boost to contactless payment transaction volume in the country.

Unusually, in Spain COVID-19 slowed ecommerce growth. In 2020 ecommerce transaction value rose by just 1.3%.

Supporting the growth of digital payments, the number of POS terminals increased from 1.8 million in 2017 to 2.2 million in 2021, a CAGR of 5.4%. The number of card payments rose from 4 billion in 2017 to 6.7 billion in 2021 at a CAGR of 13.6%.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.