Mobile Money has Limited Impact on Cash in Uganda

An International Monetary Fund (IMF) paper 1 uses data from Uganda to understand whether digital payment innovations, particularly mobile money payments, will increase financial inclusion and if it will reduce people’s preference for cash.

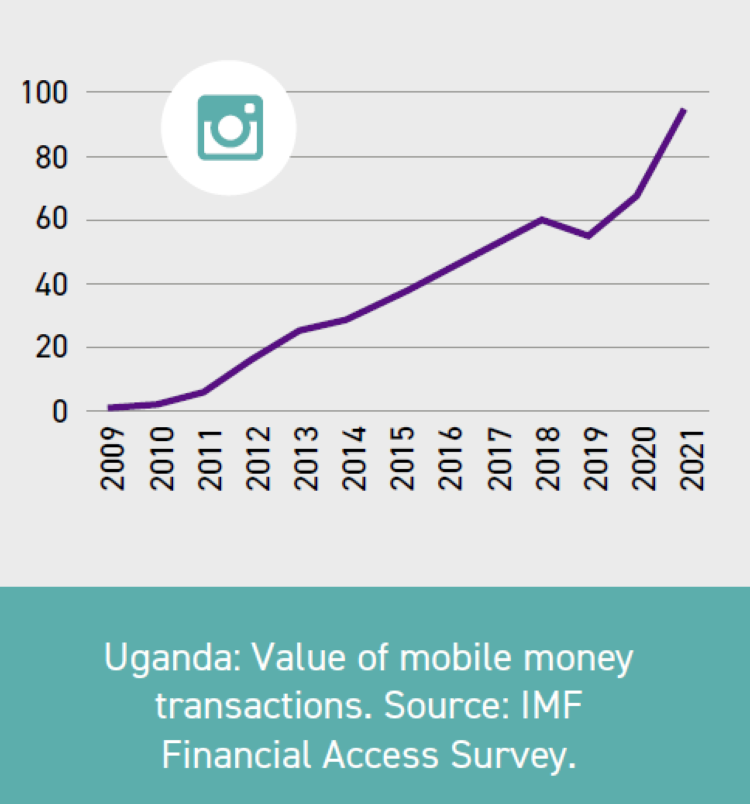

Since mobile money began in 2009, Uganda’s adoption has grown so that by 2021 the value of transactions was 94% of GDP, behind only Ghana, Senegal, Guinea and Rwanda.

Impact on cash

Linkage between data for the rise of mobile payments and changes in cash usage are not clear. While mobile money accounts have risen from 0.07% of GDP in 2008 to 0.8% in 2022, cash has only declined slightly since 2009.

Survey methodology

This study uses data from the 2018 Uganda FinScope Survey, which was commissioned by Financial Sector Deepening Uganda (FSD Uganda).

The Uganda FinScope survey employed a three-stage stratified sampling approach to arrive at a nationally representative sample of individuals aged 16 years and older (Financial Sector Deepening Uganda, 2018).

In the first stage of sampling, geographic representation was ensured by selecting 320 enumeration areas (EAs) using a probability proportional to size, ensuring national, regional, and urban-rural representativeness. In the second stage, 10 households were selected randomly in each EA. In the final stage, one adult (ie. an individual 16 years or older) was selected randomly from each of the selected households to be interviewed.

Status of mobile money

As of September 2023, there were seven private sector mobile money providers. Mobile money is backed by bank deposits and can be exchanged for legal tender. As of December 2022, there were about 25 million registered mobile money accounts.

Cash remains the main method of payment, although 28% of respondents used digital payments, mostly mobile money.

81% of respondents had used mobile money more than once in the last year and over 60% for over two years. 26% used it to send money and 58% to receive money. 64% had experienced a network failure in the last year. 9% had experienced a loss of funds. Interoperability issues and high costs meant sending money between different mobile money providers was a challenge.

Between 2018 and 2022 debit and credit card numbers rose 20% and 25% respectively, while mobile money accounts increased by 73%. There are now 3.1 million debit cards but 25 million mobile money accounts.

23% of Ugandans saved using mobile money compared with 11% using traditional banks and 60% using informal mechanisms, including keeping cash at home. Only 2% use mobile money to borrow money.

In rural areas access to bank accounts is less. Only 6.6% of respondents had a bank account, while in urban areas this figure was almost four times greater at 22.6%. In contrast 46.8% of rural respondents were mobile money users, while in urban areas the figure was 73.4%.

Conclusions

The IMF identifies two findings.

First, the rapid expansion of fintech technologies in Africa is likely to reduce, although slowly, the demand for and usage of cash over time. As an aside, issues such as network failure and limited interoperability, as well as lack of reliable electricity, may lead individuals to prefer to store their wealth in the form of cash.

Second, mobile money users are more likely to remit and receive money, and they save and borrow more, which suggests that the expansion of fintech technologies could help promote financial inclusion in Africa.

1 - ‘Mobile Money, Perception about Cash, and Financial Inclusion Learning from Uganda’s Micro-Level Data’. Félix F. Simione, Tara Muehlschlegel. WP/23/238 IMF.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.