Africa Banks on Mobile Payments

Only 28.5% of Africa’s 1.17 billion people have bank accounts and the infrastructure of bank branches and ATMs is sparse. The last 20 years had seen payments in Africa change rapidly along African lines, rather than those of Europe or Asia or elsewhere. While payments in Africa continue to change, it appears that the future is mobile.

Today Sub-Saharan Africa has 49% of the world’s active mobile money registered accounts and 64% and 66% by volume and value of transactions respectively, according to a recent webinar by Statista, the business data platform, using GSMA data. Why? The answer appears to be accessibility, affordability and availability.

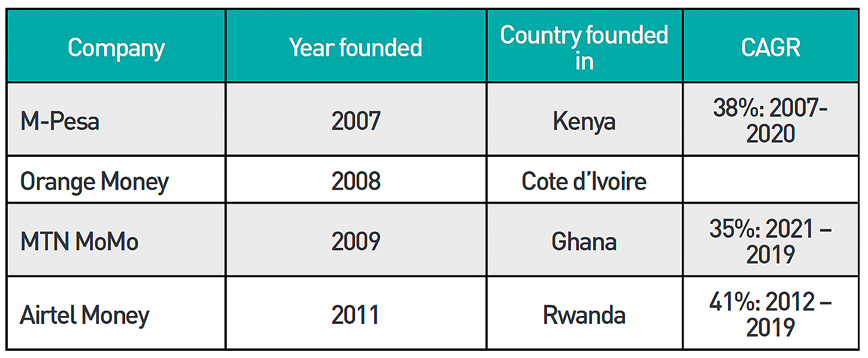

In Africa mobile money started with M-Pesa in Kenya in 2007, with new entrants following on and with rapid growth around the continent, 48% CAGR in Uganda being the highest.

Accessibility

Whilst bank branches and ATMs may be sparse, what people do have is access to smartphones and a phone signal. 17.9 million people have a fixed broadband subscription, but 531.6 million people have a mobile subscription. Between 2010 and 2020 these numbers went up from 4.5 million with fixed broadband subscriptions and 32.2 million with mobile broadband subscriptions.

Mobile phone signal coverage reaches 89% of the population.

A Chinese company, Transsion, has focused on the African market and now sells smartphones designed for the African market. These phones have increased battery life, dual Sim card slots and heat protection, while the photo function is optimised for African complexions. Priced at well under $200, in 2019 half of smartphones sold in Africa were theirs. 80% of smartphones sold in Africa are under this price point.

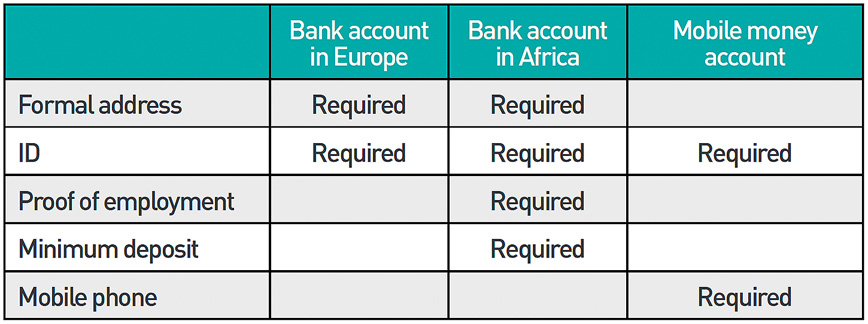

An important barrier to banking in Africa is the documentation required to open an account.

A mobile money account has a much lighter requirement, making it accessible to more people. In addition, mobile money is moving beyond the ability to upload, store, receive and send money. Many operators have developed their systems to allow bills to be paid, cross border transfers, interaction with QR codes and access to lending facilities. Some accounts even offer chip and PIN cards and e-wallets. The user experience is close to that of a bank account holder.

A mobile money account has a much lighter requirement, making it accessible to more people. In addition, mobile money is moving beyond the ability to upload, store, receive and send money. Many operators have developed their systems to allow bills to be paid, cross border transfers, interaction with QR codes and access to lending facilities. Some accounts even offer chip and PIN cards and e-wallets. The user experience is close to that of a bank account holder.

Affordability

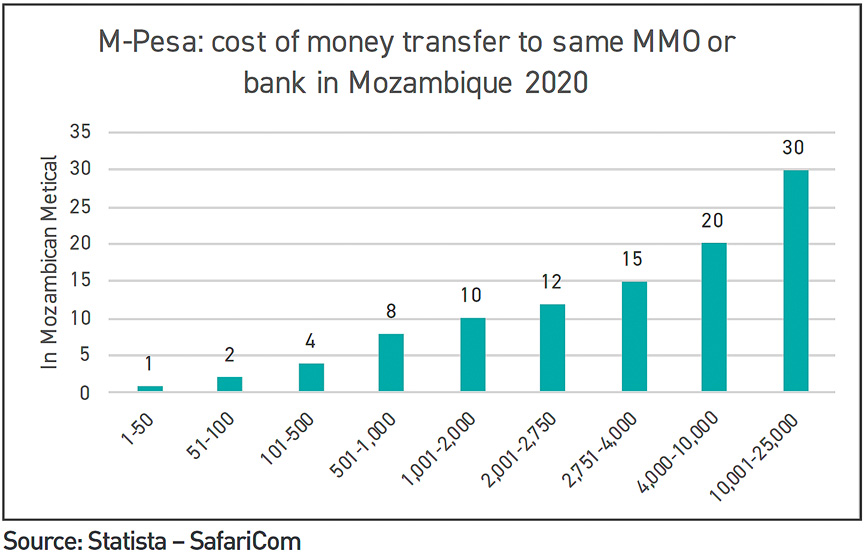

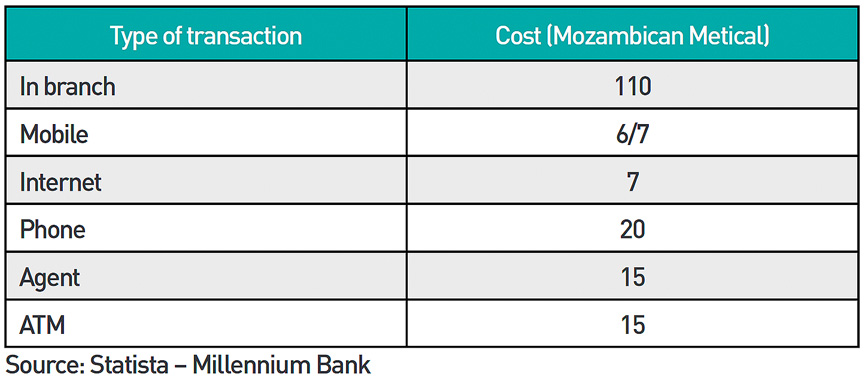

One of the reasons for the success of mobile money has been the fee structure set by providers. Revenue has been linked to the number of transactions and not to their value. M-Pesa, for example, in Mozambique have a scaled fee structure that is competitively priced compared with bank charges.

In comparison, Millennium BIM is a large bank in Mozambique.

The result is that where cash is not used to pay, mobile money is the preferred method. The Statista webinar gave data from the Bank of Ghana for January to June 2019 where, by volume, mobile money was used for 98% of non-cash payments and 11% by value.

Availability

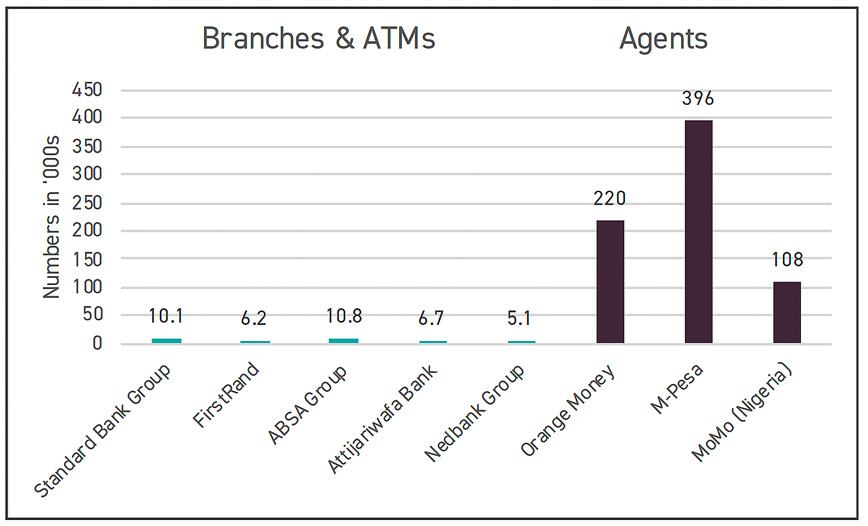

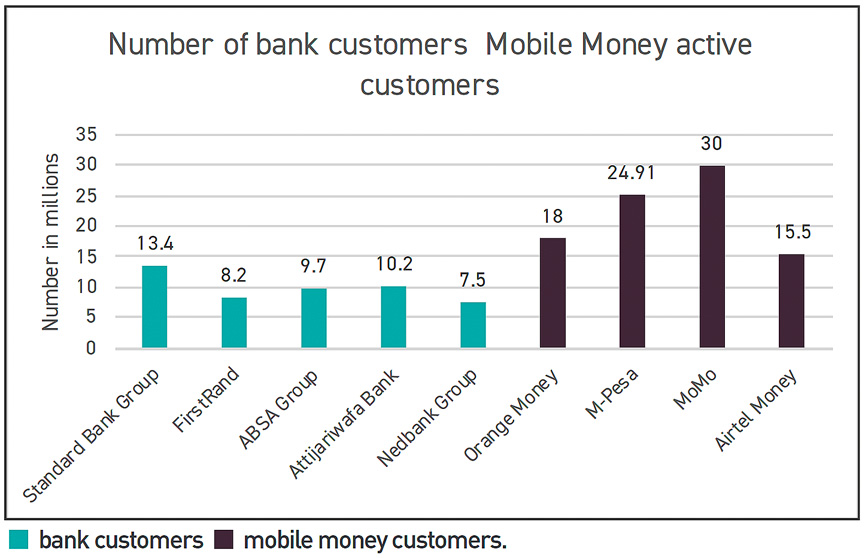

A significant reason behind the popularity of mobile money is access to agents compared to access to bank branches or ATMs. 2019 data for Uganda, for example, showed 200,857 mobile money agents compared with 9,370 ATMs. Ghana had 188,000, Rwanda 98,359 and Kenya 252,703.

The difference is shown starkly when branches and ATMs are put alongside the number of agents across Africa, as shown in the graph at the top of this article.

Impact of COVID

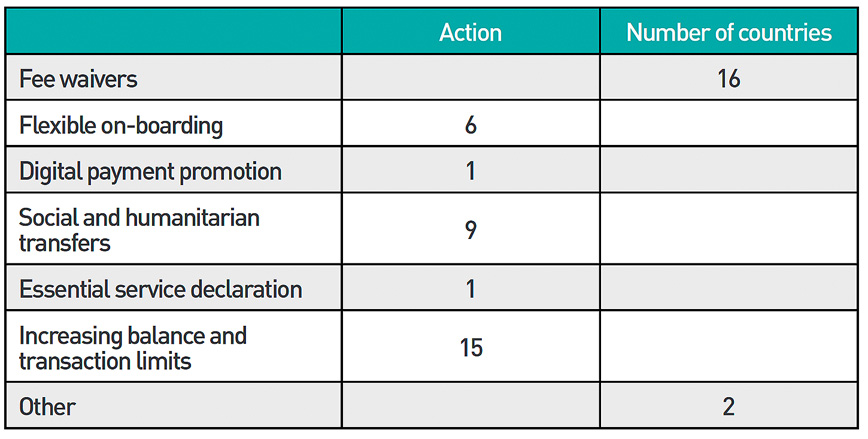

Following the outbreak of COVID-19, 18 countries in Africa took steps to encourage the use of mobile payments.

To focus on one country, Rwanda waived fees, increased balances and transaction limits and used mobile money for social and humanitarian transfers. Between 16 February and 19 April, P2P transfer volumes went up from 0.6 to 3 million transactions, with the value going up from RWF 6.9 billion to RWF 40.3 billion. The number of unique subscribers went up from 472,000 to 1.82 million. The regulatory and government actions have clearly amplified the move to mobile payments.

The future

It may be that Orange Money is showing the way ahead. In 2017 it launched itself as a bank in France. It went on in June 2019 to obtain a banking licence from the Central Bank of West African States and then, in November, in Spain. By the end of 2019 it had 500,000 bank customers which grew to a million customers in France and Spain by June 2020. In July 2020 it launched Orange Bank in Cote d’Ivoire. Orange Bank is purely online accessed through an app.

What Orange is doing, of course, is taking its bank offer to its mobile money users, but it is prepared to allow them to open an account based on being a known customer. The opportunity it is pursuing is to bring the unbanked into the banking system.

The number of mobile money accounts significantly exceeds the number of bank accounts, creating a ready market for new business.

Mobile money has been adopted in Africa in response to its lack of traditional infrastructure and requirements needed by banks to open accounts. Good mobile signals, low cost smartphones and the approach of the mobile money companies has enabled a significant uptake of the technology across much of Africa. With a young, large population, Africa remains an enormous market for payment providers whether banks, mobile money companies or other financial innovators.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.