Digital Payments - and the Last Mile to the Unbanked

The Federal Reserve Board (FRB) of Atlanta has published an article by Oz Shy, ‘Digital Currency, Digital Payments, and the ‘last mile’ to the unbanked.’ As the number of cashless locations increases, vending machines, toll booths, parking, shops etc., the article considers what stops people going digital and looks at policy options in response.

The Bank for International Settlements (BIS) issue a paper in 2016 that pointed out that most electronic payments are based on an account. Those with a low or variable income, in financially isolated communities and ill at ease with technology find this a problem. Bank accounts need identity documents and cost money to own and use, money they don’t have. Making a digital payment, if even possible, is an expensive activity for the unbanked.

Bostic et al. published an FRB Atlanta paper in 2020 that argued the focus should be on the provision of digital payment vehicles that do not necessarily depend on traditional accounts. A non-bank payment network needs non-costly ways to pay cash in and to withdraw cash as well as to make digital payments.

The paper goes on to describe the M-Pesa system based on the phone company being a digital money transmitter rather than being a deposit-taking institution, and on the Bahamas Sand Dollar, a Central Bank Digital Currency (CBDC), where an individual can put funds into their mobile app or a payment card at authorised financial institutions, up to $500 if no identity documents, up to $8,000 with identity documents. It briefly mentions Hong Kong’s Octopus card, a pre-paid transportation card, which can be used for on- and off-line payments.

Whether for a CBDC or a commercial digital payment, the paper considers four policy options.

1. Take no action and see what happens. The Federal Deposit Insurance Corporation (FDIC) 2017 research found 6.5% of Americans to be unbanked and in 2019, 5.4%. Perhaps this ‘problem’ will solve itself.

2. Take no action but require physical retailers and public utility companies to accept cash in person. A number of US states have already passed such legislation.

3. Allow free ‘pass-through’ accounts to be held by people at the Federal Reserve, with post offices and commercial banks acting as agents. Bill S.3571 was presented in the US Senate in March 2020 to this effect.

4. Require the US Post Office to provide basic banking services. In 2020 S 4614 was put forward proposing this in the US Senate.

General purpose reloadable pre-paid cards already exist and these can, depending how organised, offer ATM cash withdrawals, cash deposits and digital payments. They can be expensive, for example $14 per month to reload value. Research shows that it can be cheaper to have a normal bank account, so long as you it does not go overdrawn or isn’t used for borrowing.

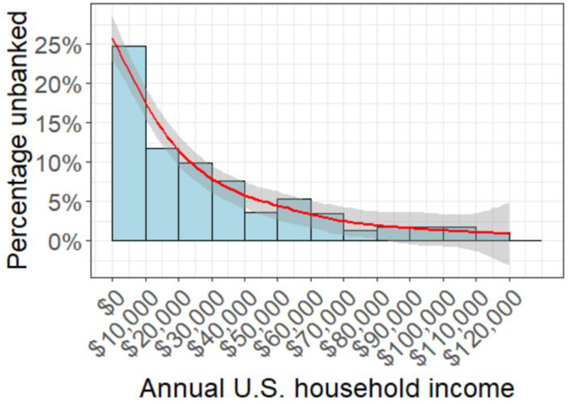

The FRB of Atlanta’s payment diaries show a rapid reduction in unbanked individuals as their annual household income increases. The percentage dropped from 25% in the lowest income group to below 10% for annual household incomes above $20,000. When incomes reached $30,000 or more, about 7% were unbanked. For those with household income over $80,000, the percentage of unbanked is statistically insignificantly.

Percentage of Unbanked Respondents with Household Income Not Exceeding $120,000

Note: The red curve displays a computed smooth local regression (loess). The shaded areas are the corresponding 95-percent confidence intervals. Source: Diary of Consumer Payment Choice, 2017-19.

The 2020 FDIC research investigated why they are unbanked.

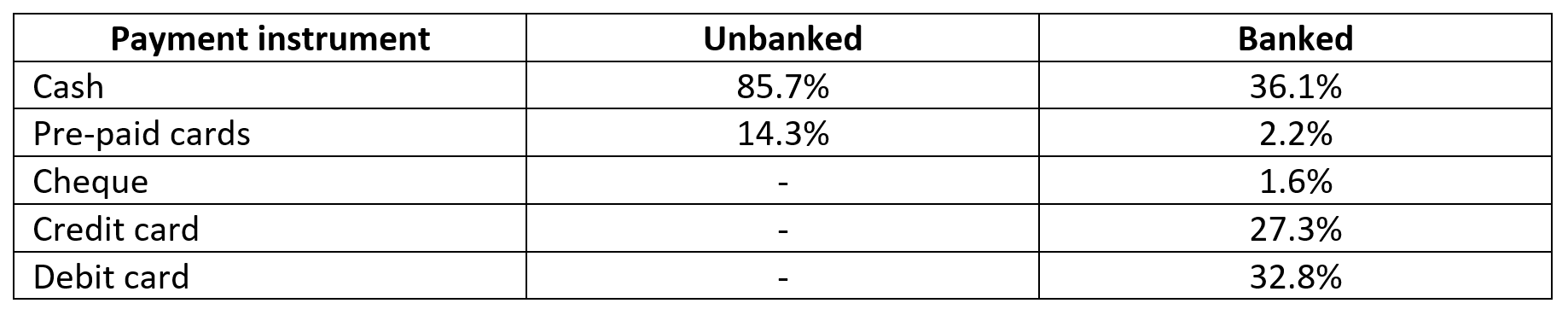

It also explored differences between in payment choices between the unbanked and the banked.

Final comment

The paper used the phrase, ‘cash clears at par’, meaning that neither buyer nor seller pays or charges upfront fees to receive cash. When we consider what payment choice means for the unbanked, the data in this paper highlights the reality of being on a low income and the importance of maintaining a low cost payment channel.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.