The Power of the Assumptive Close

The Economist Intelligence Unit has issued a paper, ‘Going Digital. Payments in the Post-Covid World’. It is interesting both for what it says and how it says it. The report constantly references financial inclusion as a benefit of going digital. What it does not explain is how all of the digital payment fees and charges referred to in the report will be paid for by those financially excluded today because of the costs and challenges of bank accounts.

‘Governments have a crucial role to play in formulating policies that guarantee equitable access to these systems while encouraging innovation’, the paper states. ‘However, regulators’ responsibilities will increase further with the spread of digital currencies and super apps, which will allow for more cross-selling while also exacerbating the risks to data security, privacy and sustainable credit terms.’

Guaranteeing equitable access makes sense, but then the paper goes on to talk about cross-selling and risks to sustainable credit terms, which require a degree of financial knowledge and expertise to handle. For example, M-Pesa introduced a form of overdraft capability, Fuliza, and the result has been widespread over-spending.

Later in the report it says, ‘payment platform providers must create additional capacity to prepare for greater demand for digital payment services, as well as opportunities to migrate customers to financial services that yield higher margins. They must also prepare for the rising costs and complexities of compliance with regulatory requirements.’

Again, the real focus is not on financial inclusion. The second sentence, though, does warn payment-platform providers of the consequences of regulators guaranteeing equitable access.

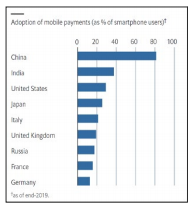

Despite all the talk about digital payments, the reality is that payment through wallets remains a small share of the digital market, as is clear in the chart below.

One section of the report starts with the headline ‘Pandemic gives regulators a unique opportunity to spur digital payments’, but then fails to give any reason why a regulator should want to spur digital payments. An example of making an argument not based on logic but through the use of language.

Similarly, it says ‘in the Philippines, the government is making a concerted effort to achieve a cash-free society by 2025 and aims to make half of its financial transactions digital by 2023. The rewards of this are numerous, most notably in terms of wider financial inclusion’, without any further explanation of how a cash-free society will help.

In a later chart, the paper lists a number of payment super app value propositions in south-east Asia. It lists six functions – payments, e-commerce, financial services, mobility/delivery, deals and chat. Again, if you are on an extremely low or variable income, how many of these services will be accessible? Payments are clearly a core function, but will the provider offer this at an accessible cost if users are not taking up the other functions?

The paper goes on to talk about China as the birthplace of the super app, and observes that it is now reversing its original loose regulatory approach, which allowed simple payment providers to become major financial players with quite sophisticated deposit and lending facilities. It suggests that other countries in south-east Asia are following the original Chinese approach – happy to trade access to banking products against the risk of over-mighty, unregulated future providers.

The article makes the comment that payment operators ‘will shift their focus towards improving their profitability, moving on from their current preoccupation with expanding their customer bases.’ One has to hope that there will still be space for today’s cash users to use their products.

All of this, of course, still leaves issues around data security, financial fraud, cybersecurity and the role of regulators faced with unfamiliar technological advancement to be resolved. If there aren’t common regulatory standards amongst neighbouring countries, will there be a risk of regional monopolies?

The paper ends with another of its assumptive closes: ‘The benefits of digital payment systems significantly outweigh the risks associated with them. For governments, they provide an avenue to raise financial inclusion and further the cause of economic development. Individuals, especially those in developing countries, can more effectively participate in economic activity. Private organisations will benefit from the new opportunities created as a result.’

For those with an income above a threshold and with stability, this statement may be true. The opportunities to make money for the private organisations is clear. The case for going digital benefiting the large number of people at the margin of society and the economy was not tackled.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.