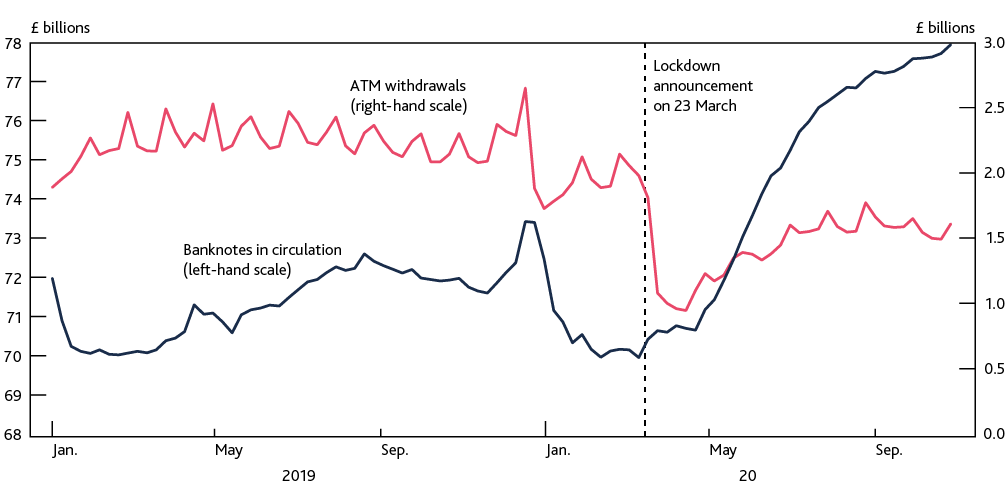

The Cash ‘Paradox’

In its latest Quarterly Bulletin, the Bank of England published an article ‘Cash in the time of COVID’. The article seeks to explain what it referred to as the cash ‘paradox’, that cash in circulation is up while cash transaction volumes are down, which has been brought into sharp relief during the pandemic.

Demand for cash

In the ten years from 2009 payments in cash fell from around 60% of transactions to 23%, although this still represents about 9.3 billion transactions a year. Between 2005 and 2017 the value of notes in circulation doubled. Research shows a higher cash demand when interest rates and inflation are low, when exchange rates fall and there are concerns about the banks or the economy.

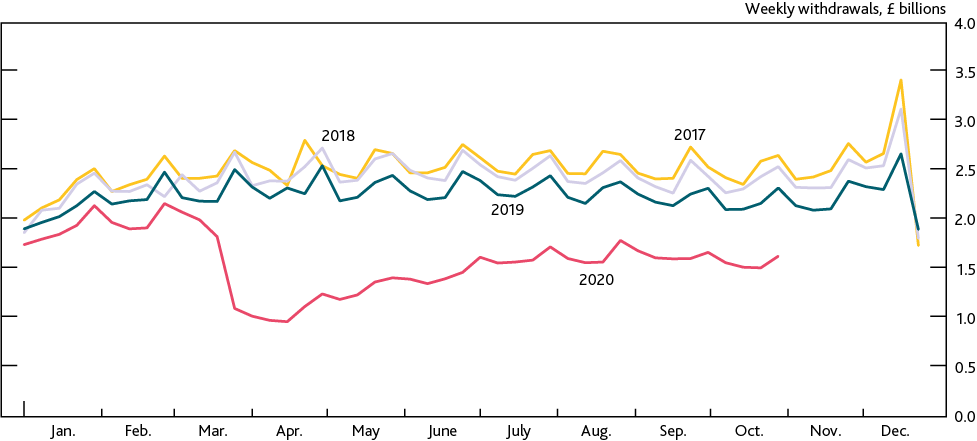

In the pandemic cash usage has plummeted, ATM withdrawals were down 60% in March recovering to a 40% decline by October. In the UK 90% of cash is accessed by ATM withdrawals. The decline was less in low income areas, and the report gives the district of Liverpool Walton as an example, where the decline was 23%.

In addition to the decline in consumer spending and a fear of transmission, the report also noted the reduction in two big cash user groups, tourists and commuters. Commuting fell between April and September by 81% in London and 71% in Glasgow.

Key drivers for cash were identified as the level of consumption in the economy, pub and restaurant usage and tourism. If unemployment increases, cash usage is also likely to increase.

Causes of the increase in cash in circulation

The Bank identified four possible causes for the increase in cash in circulation:

Cash is not being returned by retailers, financial institutions, the ATM system and the public.

People are holding more cash either as a contingency or because they have been unable to spend it.

There is a lag between economic activity re-starting and cash starting to flow again around the cash cycle.

The cash ‘system’ is fully primed.

A LINK survey in April suggested that 14% of people were holding more cash as a contingency and the Bank’s own July survey produced a figure of 8%. In LINK’s April survey, 76% thought their behaviour had changed over the next six months, 34% were doing more online shopping and 50% were using cards more.

In the Bank’s July survey 33% were making more non-cash payments, 16% because of the convenience of contactless payments and 16% because shops preferred contactless payment. 30% said they had not changed their behaviour.

Cash usage

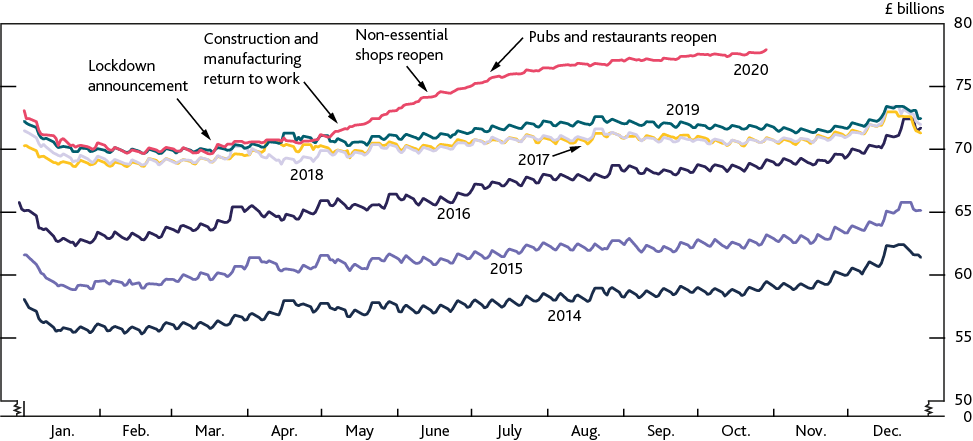

Cash in circulation has increased sharply since the pandemic started. It is not clear why demand grew strongly in May as lockdown started to be eased rather than when lockdown was introduced in March.

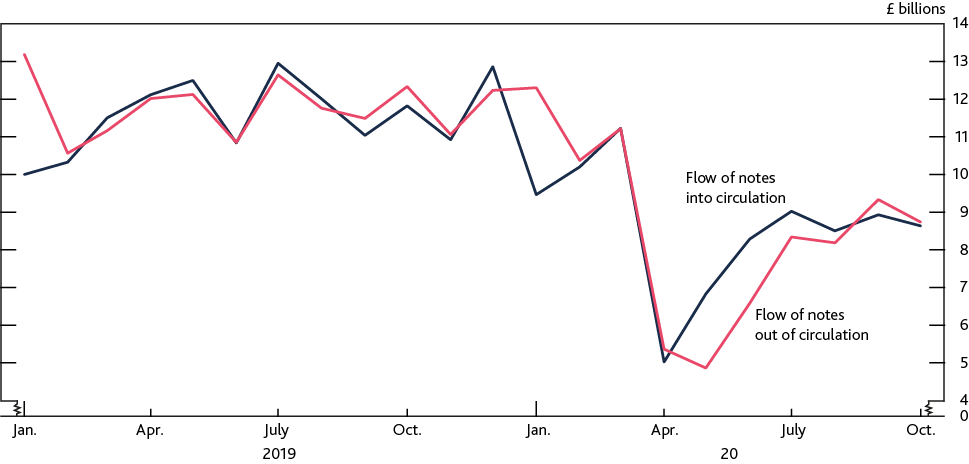

Cash inflows and outflows have been balanced once more since August/September.

At the start of the pandemic there was a fall in consumption across all payment methods, with ATM withdrawals, Visa and Barclaycard reductions largely matching. Total household consumption, according to Visa figures was 30% down In April with contactless transactions also down, 40% by value and 44% by volume. As the economy recovered card usage increased until August when it then plateaued, but cash usage plateaued earlier in June.

How safe are banknotes?

Many retailers have already acted to safeguard their staff, including encouraging customers to pay with non-cash alternatives, and there is a movement to invest in self-service equipment in shops and banks.

In this context, the report gave details of research about the risks associated with using cash in a pandemic. This was reported in November’s Currency News but the Bank’s conclusion was that ‘any risk from handling cash should be low’.

Medium to long term outlook

Online shopping represented 19% of retail activity in September 2019 but had increased to 28% this year, including a significant number of new users. In a Bank survey of the public in January, 15% of people said they had been to a shop that refused cash. In July a second survey reported 42% saying that in the last six months they had been in a shop that had refused to accept cash.

In a Paysafe survey, 56% of respondents said they were happier using contactless payments than they were a year earlier. The number of people who said they could go for a month without using cash increased from 32% pre-pandemic to 44%, with 44% saying that this was because retailers encouraged non-cash payments and 35% being concerned about the safety of cash.

This evidence causes the Bank to consider to what extent the changes caused by the pandemic will become permanent, in particular, whether the recent increase in the growth of notes in circulation will continue, for how long and by how much.

To achieve this, it will conduct further surveys and consultation with key players to assess whether COVID will permanently affect consumer behaviour and consumer preferences for cash over other payment methods.

The Bank will work with NCS members and a range of large retailers to understand customer demand, cash holdings and attitudes to cash acceptance. It will talk financial institutions to understand how business models and customer demands are changing.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.