DMI – the Future of Payments

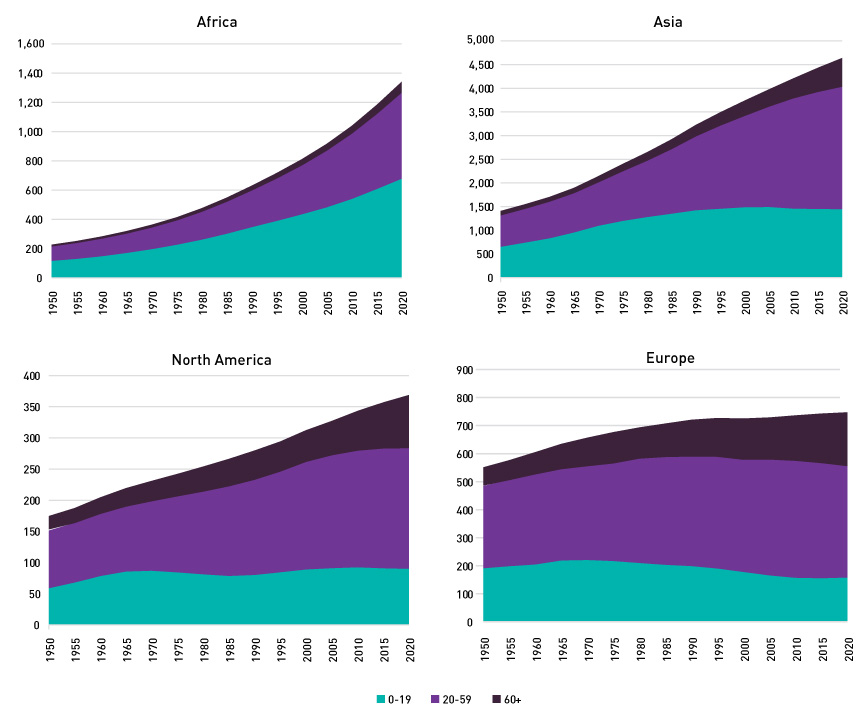

OMFIF’s Digital Monetary Institute recently published a report on the Future of Payments. The report is a thorough examination of non-cash payment developments but two elements stood out. Firstly, a striking infographic showing the age profiles of four parts of the world and, secondly, more information on the growth, importance and impact of mobile payments.

Research consistently shows that people under 60 years old are comfortable with technology and are more confident and willing to engage with it than older age groups. These age profiles are, therefore, part of the story of the future of cash.

Managing payment risk outside of the commercial banks

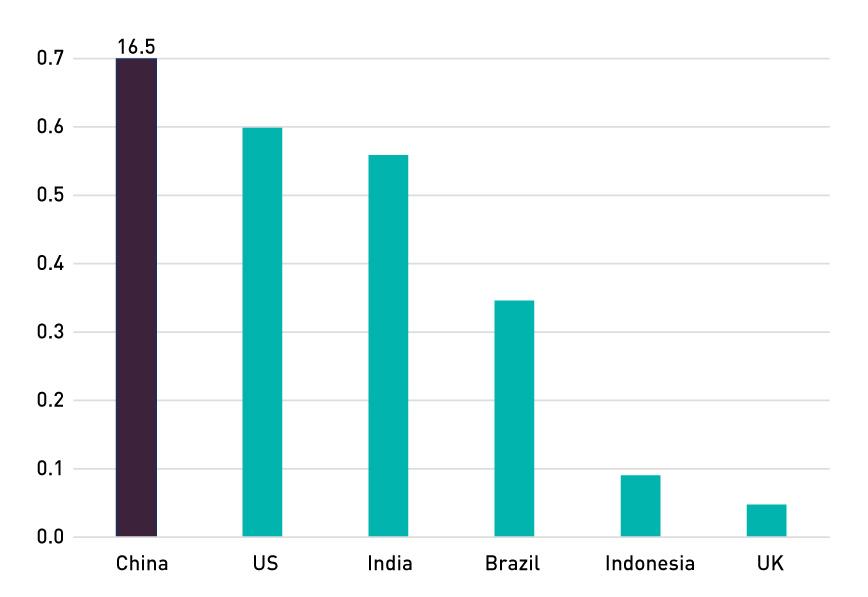

The report considers the management of risk and the regulatory response in some detail. It contains interesting data on the speed and size of payments that have moved into mobile payments. As was reported in November’s edition, mobile phone growth is driving mobile money growth in Africa. The chart below demonstrates that mobile phone growth is happening the Asia Pacific region too.

Number of mobile cellular subscriptions per 100 people. Source: World Bank, OMFIF analysis.

Number of mobile cellular subscriptions per 100 people. Source: World Bank, OMFIF analysis. China, of course, is the home to two huge mobile payment companies, AliPay and WeChat Pay, which is reflected in its ranking.

As a result, the big tech mobile payment companies are increasingly important in their economies, no more so than in China.

China’s two leading payment companies, AliPay and WeChat Pay, have grown in influence and become an increasingly central part of China’s financial system. One of the concerns was about whether these companies might take risks that commercial banks would not, including whether they were monitoring illicit activities or monitoring financial transaction sufficiently carefully.

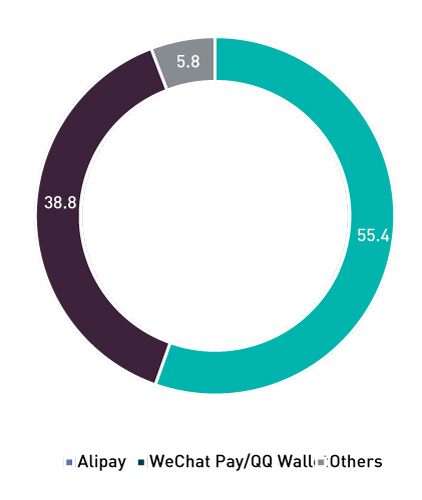

Chinese transaction volume as market share, %, Q1 2020. Source: iResearch, OMFIF analysis.

Chinese transaction volume as market share, %, Q1 2020. Source: iResearch, OMFIF analysis. There were more specific concerns about how funds in their systems were being managed. For example, were funds being reinvested in high-risk, high-return assets in order to maximise profits? Were they prioritising advertising and marketing to grow their user base rather than improving their products and services?

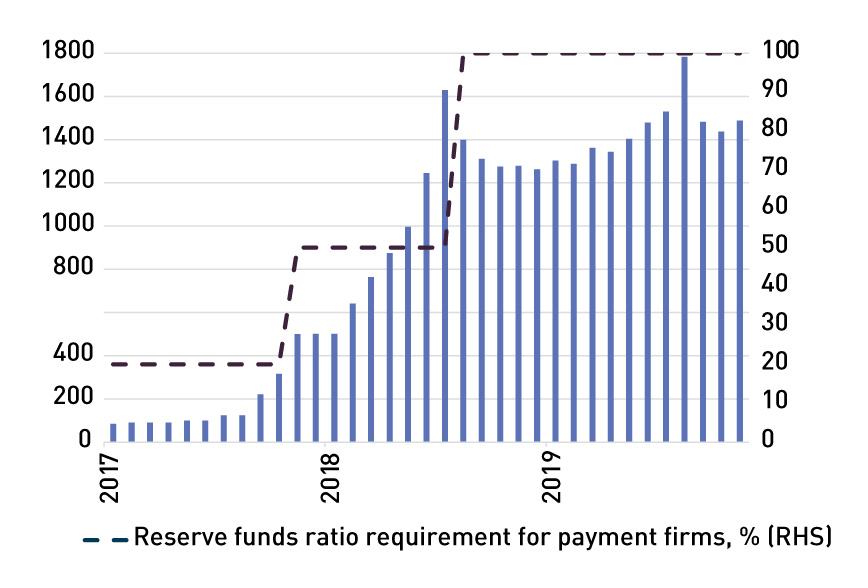

The response of the regulator was to use reserve fund requirements to manage these risks. In 2017 20% of unused customer funds had to be held in non-interest bearing accounts overseen by Peoples Bank of China. In 2018 this was increased to 50% and in January 2019 all unused funds were required to be kept in a separate account.

Chinese non-financial institution deposits, ¥bn. Source: People’s Bank of China, OMFIF analysis.

Chinese non-financial institution deposits, ¥bn. Source: People’s Bank of China, OMFIF analysis.These changes were criticised by some people, including Jack Ma of Ant Group, who own AliPay, because they were regarded as stifling innovation and curbing an important revenue source for third-party payment companies.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.