What Drives Consumer Payment Behaviour?

In 2019 National Westminster Bank (NatWest) commissioned independent academic research to look into the drivers of consumer payment behaviour, including consumer attitudes and intentions towards cash. The research was carried out by Professor Darren Duxbury, Dr Thanos Verousis and by David Marsh

The background to the research is changing consumer payment trends, the use of cash as a payment method is declining in many countries. In the 10 years to 2016, UK cash transactions fell by 35% and are predicted to fall by a further 40% to 2026. The research aimed to do two things. First, provide better understanding of the behavioural factors that influence individuals’ attitudes towards and intentions to use cash relative to other forms of payment. Second, examine the extent to which exogenous shocks influence intentions to use cash.

The research was based on an online survey of 2,801 UK adults in April 2019, representative for age, gender, income, education, and geographical location.

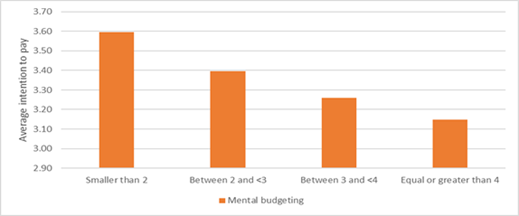

Payment intention and mental budgeting

Mental budgeting is where people separate money into different ‘pots’ in their minds, i.e. money to be spent on bills, entertainment, emergencies, etc. The research explored differences between those who mentally budget and those who don’t when it comes to their intention to pay with cash or using electronic payments.

The conclusion was that those who mentally budget are more likely to intend to use cash.

Respondents who scored low on the mental budgeting scale intended to make a greater use of electronic payments. Scoring high in the mental accounting measure was negatively related with the belief that paying electronically is a good idea (i.e. they had a positive attitude towards cash).

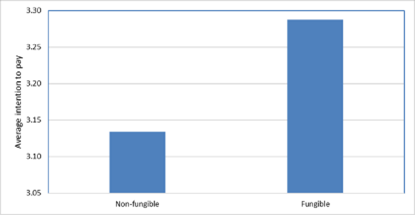

Payment intention and money fungibility

Fungibility means the extent to which things are interchangeable. The question was to what extent did respondents treat all money as the same irrespective of the source or means of storage, i.e. a physical pound is the same as a pound in the bank.

Respondents who treated money as fungible intended to make more electronic payments than respondents who treated money as non-fungible. The research concluded that those who treat money differently (i.e. differential propensity to consume/save) depending on how it was obtained or stored (e.g. earned vs gift) are more likely to intend to use cash.

Loss Aversion

Loss aversion is the tendency to feel the pain of a loss more keenly than the pleasure from an equal gain (i.e. ‘losses loom larger than gains’).

High loss averse individuals tended to feel the pain of giving up an object (e.g. cash) more keenly and hence, given they have a higher pain of payment associated with cash than other means, were more likely to shun cash payment. Loss averse individuals were more likely to adopt contactless cards, perhaps in part to limit their exposure to the pain of paying by cash.

Habitual Behaviour and Emotions

Habitual behaviour is where people have a tendency to succumb to routine/automaticity in day-to-day life. The research also looked at the feelings people have towards a payment method.

Respondents appeared to make more cash payments under £5 as a matter of routine, but more electronic payments under £5 as a result of an unconscious action. As transaction values increase, habitual routine leads to shifts from paying with cash to electronic payment, while habitual automaticity leads to shifts in the opposite direction. Transaction size, therefore, is important.

Emotions are less positive towards cash and paying electronically is associated with more positive emotions than paying with cash. However, the influence of emotions on payment intentions diminishes as transaction size increases. Again, transaction size matters.

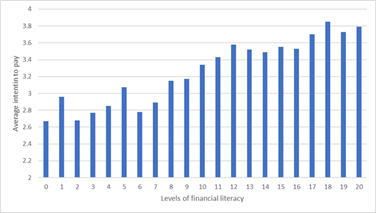

Payment Intention and Financial Literacy

High financial literacy is linked with the view that paying electronically is a good idea. Higher financially literate individuals hold a greater variety of cards and tend to make fewer cash payments. As transaction size increases, emotions become less important, while financial literacy increases in importance. Higher financial literacy is related to lower intention to use cash.

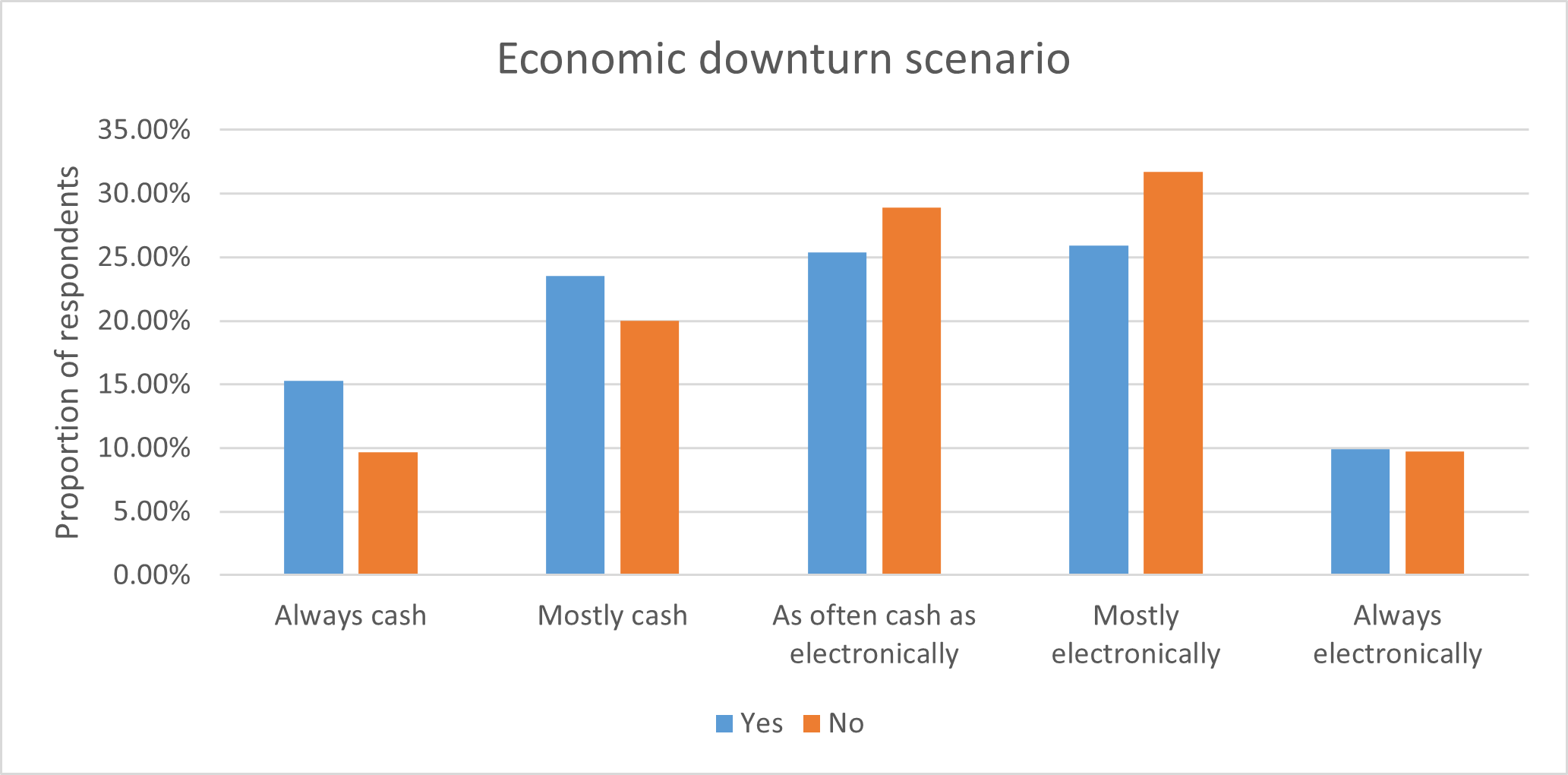

Exogenous shocks and changes in payment intentions

The study looked at two scenarios, an economic turndown and a security breach, to see how payment intention changed. In the first scenario respondents were asked to imagine a general economic downturn for the UK economy that had led to a change in their personal circumstances and a significant decrease in their disposable income. In the second they were asked to imagine that a security breach meant their personal information had been released to unauthorised parties.

Independently for both scenarios, there was a shift in payment intention towards cash. This suggests that while payment habits form, payment intentions shift in response to exogenous shocks demonstrating that such habits are not immune to change.

In the event of a security breach, individuals that scored high in the financial literacy score, and are therefore more likely to use electronic payments, had a higher tendency to switch towards cash.

Shifts in payment intention associated with an economic downturn were in part dependent on prior related experience (represented on the graph below, note yes / no refers to respondents previous experience), while the same is not true of past experience of security breaches.

Other findings indicate cash is considered as a “safe haven” when it comes to general economic or security shocks, while loss aversion is associated with a stronger switch towards cash following general economic or security shocks.

The researchers concluded that holding a contactless card is associated with an increased security risk.

Research implications

The enhanced understanding of how behavioural and habitual factors determine people’s propensity to use cash, especially in the context of the growing importance of consumers’ desire for anonymity in the ‘big data’ age, can help the cash industry, and the institutions therein, to respond in more informed ways to the cash challenge, ensuring that their products and services support customers’ future needs.

Editor’s comment

The research can also be interpreted as underlining why cash needs to be maintained. If there is a payment problem and people want a safe haven, what happens if cash did not exist. The alternative to electronic payment will look just like the place you are running from, ie. a credit card won’t feel safer than a debit card (nor would a central bank digital currency).

The importance of emotion is interesting because we all know how fast sentiment can change. What feels safe today may not feel safe tomorrow. Again, the importance of real diversity in payment choice is underlined by this.

The importance of habits and emotions raises concerns for the future. If younger people see money as fungible, don’t do mental budgeting and habitually pay digitally, they won’t use cash. If cash is not valued, and not used, then it will become economically unviable and, without friends, won’t be sustained. The research describes, therefore, what is potentially a volatile situation where cash is not needed until it is needed, at which point it will be very important, but it may have been allowed to wither away. This puts into sharp relief both the importance and the size of the challenge in maintaining cash.

1 Professor Darren Duxbury, Newcastle University Business School, Dr Thanos Verousis, University of Essex Business School, and David Marsh, NatWest.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.