Measuring and Understanding Foreign Demand for Euro Banknotes

The European Central Bank (ECB) study, 'Foreign Demand for Euro Banknotes', set out to identify the demand drivers for euro banknotes and to estimate the share of euro banknotes in circulation outside of the euro area.

The authors wanted to understand whether external demand explained the 5% per annum growth in cash in circulation over the last 10 years. The conclusion is that 30-50% of the total value of euro banknotes in circulation is outside of the euro area. Demand is not driven by factors such as global uncertainty or short term interest rates, but by locally specific determinants such as local inflation, economic activity and foreign tourism.

The paper started by suggesting demand for the Swedish krona is for domestic transactions, for the Danish krona for domestic transactions and as a store of value, and the euro for domestic transactions, a store of value and for international use. They suggested that these different cash usage profiles were why Sweden’s cash usage is declining, Denmark’s is stable and the ECB’s is growing.

They reported on research that reveals that people decide to use a foreign currency because of problems with their own alternatives. In developing countries there may be a lack of credible domestic savings and payment alternatives. In economies transitioning to being advanced, there may be a lack of trust in the banking system, weak institutions and memories of past crisis, as well as poor infrastructure, financial literacy etc.

Economic uncertainty is a bigger influencer of people choosing a foreign currency than financial uncertainty. Usually, the foreign currency is used as a store of value, particularly if there is high inflation, but it can be used for transactions.

Not unsurprisingly, Central, Eastern and Southern European countries moved to the euro when it was launched in preference to the US dollar.

Euro banknote demand model

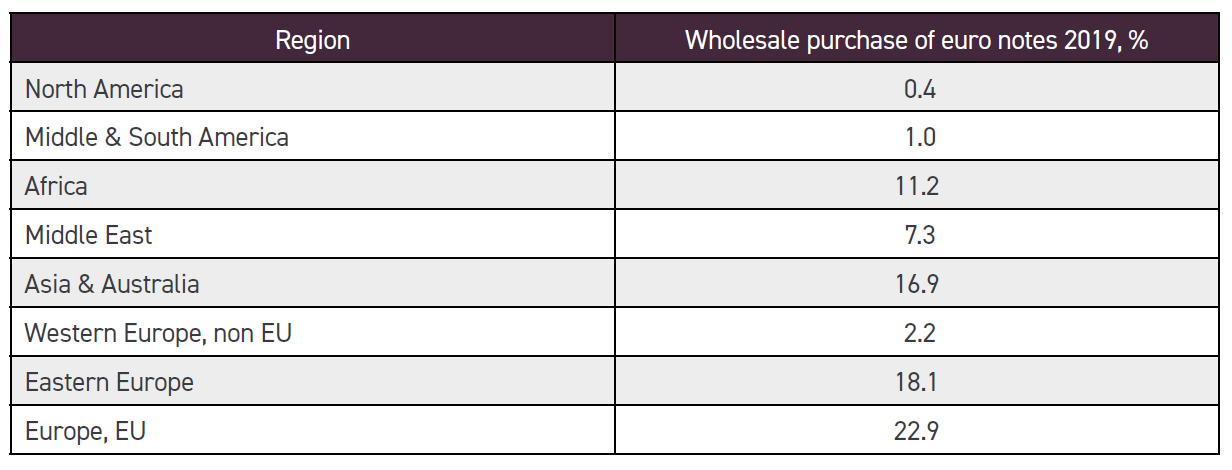

The paper describes a euro banknote demand model, referred to as a D€ note model, based on assessing long and short term relationships between a range of factors and the demand for euros for each denomination. The model was populated with wholesale export data for the Eurozone.

The long term factors used were:

Short term interest rates (reduced demand)

Real GDP (increased demand)

Foreign demand (increased demand for €50, €100 notes)

Real effective exchange rates (increased demand for higher denominations)

ATMs (increased demand for €20, €50 notes).

The short term factors included all of the long term factors and:

Unemployment rate

Economic policy uncertainty

Financial volatility.

In addition, the study added dummy factors to take into account the 2008 financial crisis and the announcement of the withdrawal of the €500 banknote.

When the €500 was withdrawn, the decline in exports was matched by an increase in the export of €100 and €200 notes.

During the pandemic, and a period when the Russian rouble devalued, the export of €200 notes to Russia increased by 13.9%.

The study showed that the model worked better for the high denominations than the low, but for both gave a good indication of how demand changes in line with these factors.

Estimation of euro banknotes outside of the euro area

The study used two approaches to reach an estimate for euro use outside of the Eurosystem.

Firstly, the 2017 Estimate Model of the external statistics division of the ECB. This set a lower bound based on net shipments from the EU, and an upper bound based on the coin to banknote ratio. The logic was that coins are used to settle transactions and, therefore, their use relates to low value domestic banknote usage in the EU rather than outside. Clearly some coins are used for transactions outside of the EU, particularly in neighbouring countries, and tourists take coins home.

The lower bound estimated that 30% of the value of euro banknotes in circulation are outside of the euro area and the upper bound is 50%.

The second approach was the seasonal method. This relies on the assumption that, in contrast to domestic transaction demand for banknotes, both domestic demand for hoarding purposes and foreign demand for banknotes show little or no seasonality, so total banknotes in circulation displays dampened seasonality factors.

Therefore, in the absence of any further assumptions, the seasonal method only allows total banknotes in circulation to be split into 1) domestic transaction demand and 2) the sum of domestic hoarding demand and foreign demand.

Foreign demand for euro banknotes rose from between €50 billion and €100 billion in 2002 to about €600 billion in 2018, which represents 49% of the total value of euro banknotes in circulation.

The authors also looked at the ‘age of banknotes’ method but did not use it in their results. This looks at how old banknotes are when they are destroyed. It assumes that the more they are used, the faster they deteriorate. Banknotes that are exported tend to return to NCBs less frequently, so their average age is greater than those of a currency that is not exported. This approach estimated that 48% of euro banknotes are outside of the EU.

The study considered net cash remittances by people in the euro area back to their home countries for 2018. This review suggested that between 6.6% and 24.6% of euro banknotes in circulation are not used in the euro area. This fails to take into account how far away some of those countries are, tourism or cross border spending. Again, the result was not used in the conclusions.

Final thoughts

Estimating foreign demand for banknotes is a difficult task. Relatively few currencies are used as a ‘reserve’ currency internationally, but all currencies experience different degrees of outflow. Although this study covers the eurosystem, which is a monetary union, the lessons learnt and the approach, we would suggest, are useful and an interesting exercise for others to consider.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.