‘Ready, Steady, Go’? Results of the 3rd BIS Survey on CBDC

The Bank of International Settlements (BIS) received 65 responses to its latest Central Bank Digital Currency (CBDC) survey of which 21 were from Advanced Economies (AE) and 44 from Emerging Market/Developing Economies (EMDE). The results are published in BIS Papers 114, authored by Codruta Boar and Andreas Wehrli.

Although those who reply change each year, a number of clear trends are evident:

A move from conceptual research to practical experimentation.

The motivation to introduce CBDCs is defined by local circumstances. Although the BIS has defined five core reasons, the other category contains nuances and motivational spider charts reflect distinct differences.

Those who are minded to introduce CBDCs are firmer in this thinking and are responding accordingly; those who have reservations are slowing down or pulling back. 7/8 of central banks in the advanced stage of investigation are EMDE countries.

Increased thinking about collaboration around cross border use of CBDCs and the need to find common policy grounds.

A new awareness that cash use may decline.

A growing awareness of the implications of other countries introducing CBDCs that their citizens might choose to use.

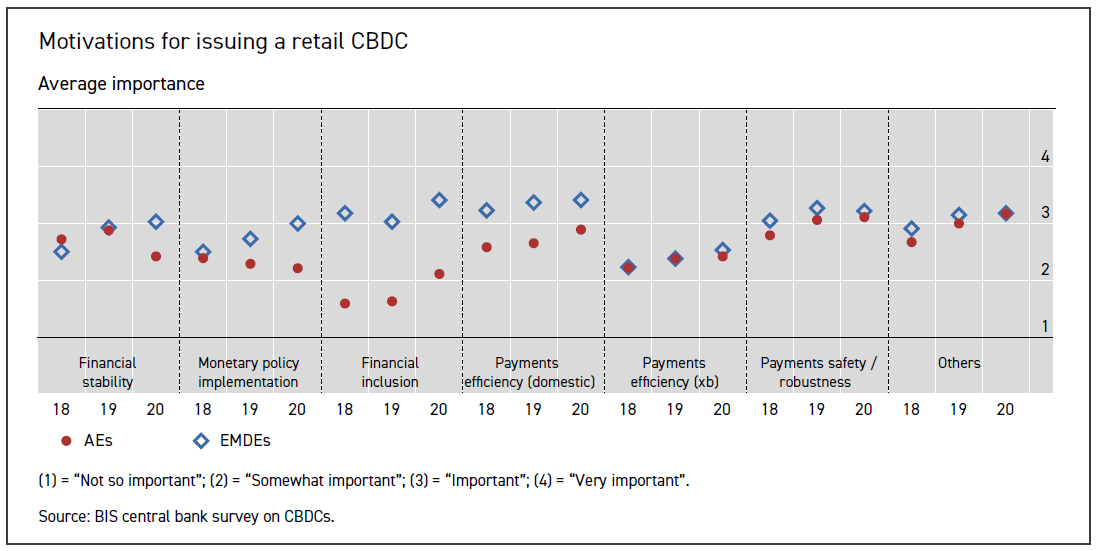

Motivation

AEs and EMDEs differ particularly around the importance of CBDCs in delivering financial inclusion, domestic payment efficiency and monetary policy implementation. Generally, EMDEs score more of the motivational areas as important than do AEs, hence EMDEs leading the charge on retail CBDCs.

For EMDEs, payment efficiency and financial inclusion appear to be their key motivators, while for AEs it is payment efficiency and payment safety.

For EMDE’s, ‘other’ includes access to central bank money if less cash is used, and maintaining sovereignty should ‘digital dollarisation’ take place (if citizens and businesses choose to trade in another country’s digital currency).

For wholesale CBDCs, payment efficiency is the prime motivator for both AEs and EMDEs*. Other motivations are the development of capital markets, the enhancement of cyber security and improvements in securities trading and settlement.

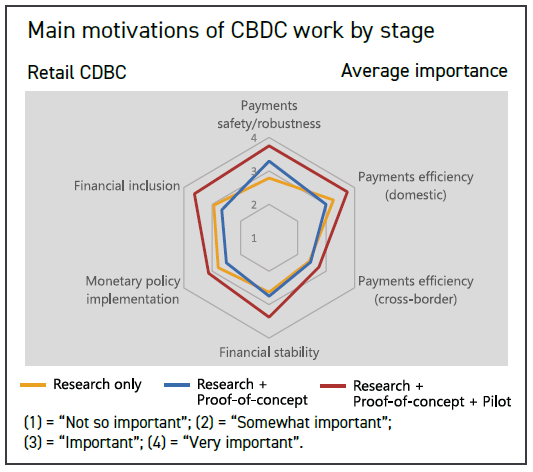

Motivation by stage of work

For each stage of research, from conceptual work to pilot preparation, the motivation for the work is different. The developing thinking, and emphasis, for cross border payments for retail CBDCs attracts less attention and the lower level of interest in monetary policy is also reflected.

Likelihood to issue a CBDC

60% of respondents said they were unlikely to issue a CBDC in the next six years. Half of those who had responded in 2019 as being likely to issue a CBDC now said it was possible or unlikely.

EMDE central banks were more likely to be considering issuing a CBDC than AE central banks, but even amongst AE central banks 20% thought it possible they might in the short or medium term.

A move to being more likely to issue a CBDC perhaps comes from the level of work being invested in exploring the idea, the increase in digital payments and the possibility of global stablecoins or CBDCs issued by other countries.

The survey showed some countries pushing back possible launch dates but an equal number bringing them forward, reflecting the complexity of the whole subject and the huge interest in it.

The paper also reported on the work done by central banks to amend their legal status to be able to issue a CBDC. About a quarter of central banks have, or are working towards, legal authority to issue a CBDC, but this has hardly changed over the last few years.

Cryptocurrencies and stablecoins

Central banks continue to see cryptocurrencies as niche products. Their surge in value reflects their speculative nature, which is underlined by their level of usage not increasing in line with their value.

Two thirds of respondents are studying the impact of stablecoins on monetary and financial stability, reflecting a different view of stablecoins compared with crypto currencies. EMDE central banks have increased their research. Despite this, only a few central banks cite stablecoins as motivating their CBDC work.

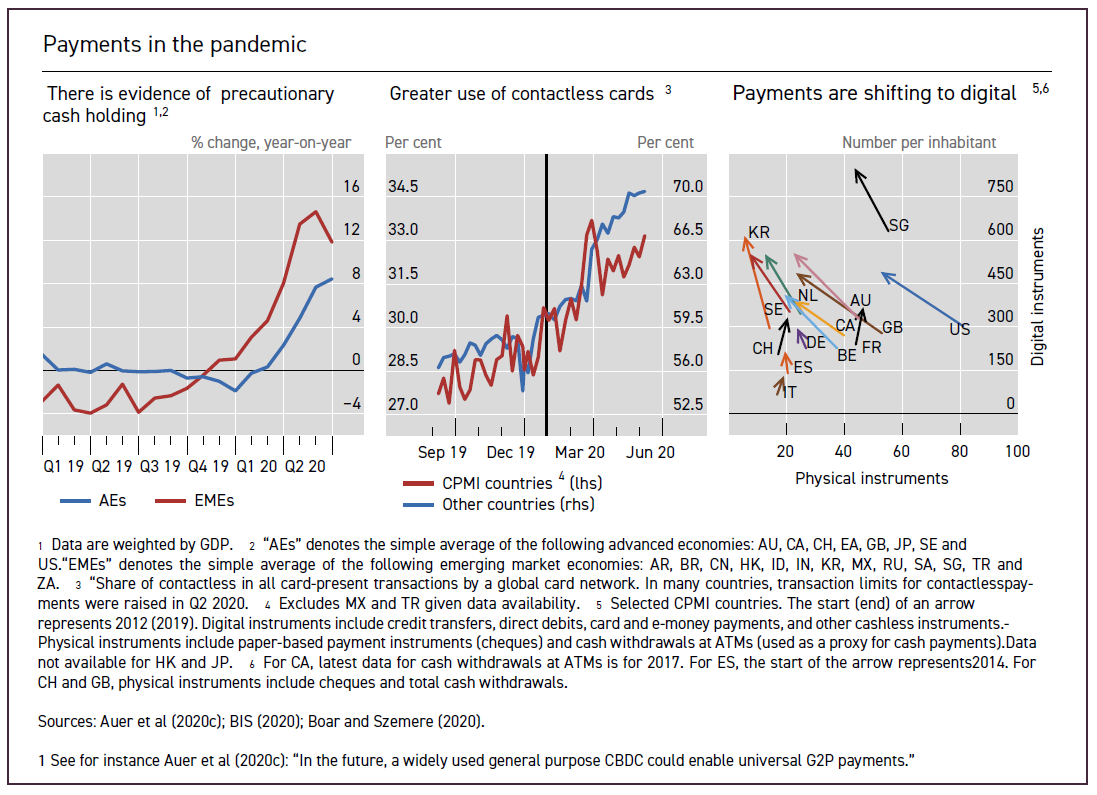

The ‘payments paradox’ in a pandemic

The results of the study included an interesting set of data in its Annex about payments in a pandemic. It shows clearly how the payment paradox is accelerating in the pandemic. Simply put, the payments paradox is how there can be a rise in cash held (and in circulation) at the same time as a decline in cash used. The data shows how the pandemic increased cash held while digital payments rapidly increased.

It shows clearly how notes held as a store of value increased in both AEs and EMEs.

It also shows the continued increase in payment using contactless cards. The lines show an acceleration, but in the context of demand that was already growing strongly. The Committee on Payments and Market Infrastructures (CPMI)** represents 28 countries, over two thirds of which had a high level of contactless payments prior to the pandemic, which is why their percentage increase is lower than the other countries.

The countries shown in the chart that shows the shift to paying digitally are CPMI members. The chart shows the journey from 2012, the start of the arrow, to 2020.

Given we know that the number of transactions reduced in line with less economic activity in most countries, this data suggests an increasingly unstable situation, perhaps an unsustainable situation. One to watch.

*Project Helvetia (BIS Innovation Lab working with the Swiss National Bank based on SIX infrastructure), Project Stella (ECB and Japan), Project Jasper-Ubin (Bank of Canada, Monetary Authority Singapore), Project Inathon-LionRock (Hong Kong Monetary Authority, Bank of Thailand), Project Aber (Saudi Central Bank and Central Bank of the UAE).

**(Membership (bis.org).

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.