Germany Faces Higher Card Fees

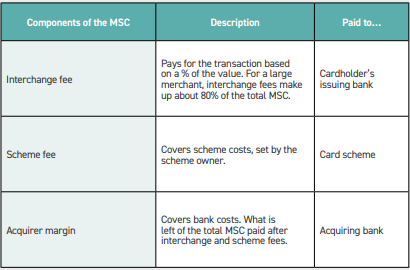

Card fees are complicated. CMSPI have issued a useful paper looking at Germany’s payment market and what has happened since 2015. The Merchant Service Charge (MSC), what merchants pay to receive a payment from their customer, consists of three elements, as below.

The European Union (EU) 2015 Interchange Fee Regulation capped interchange fees at 0.2% for debit cards and 0.3% for credit cards. The regulations excluded scheme fees as well as interchange fees on commercial cards. Between 2015 and the two year review of the regulation, scheme fees rose by about €400 million, according to the CMSPI consultancy, and since 2017 they are estimated to have risen by a further €600 million.

The European Union (EU) 2015 Interchange Fee Regulation capped interchange fees at 0.2% for debit cards and 0.3% for credit cards. The regulations excluded scheme fees as well as interchange fees on commercial cards. Between 2015 and the two year review of the regulation, scheme fees rose by about €400 million, according to the CMSPI consultancy, and since 2017 they are estimated to have risen by a further €600 million.In 2019 an agreement was secured for inter-regional payments in the EU that put in place a cap of 1.15% for debit cards and 1.5% for credit cards. This only applied to ‘customer not present’ transactions.

Every country is, of course, slightly different. In Germany CMSPI estimate that costs for the international card networks have risen 60% since 2015. Their use is rising fast, 30% over the same period. Partly this is because of a trend towards what are known as mono-badged cards issued by new online banks such as N26. Mono-badged cards can’t use Germany’s very successful Girocard system. Girocard has 61% market share of the payment market, and 92% share of the debit segment within the total. Girocard allows merchants to negotiate their interchange fees for face-to-face payments, resulting in fees lower than the EU cap.

Like many countries, Germany is seeing a rise in Buy Now, Pay Later (BNPL) payments. These tend to replace debit transactions (which incur MSC charges as low as 0.2%), incurring much higher charges (3% or more, based on a €35 transaction).

CMSPI has identified further cost increases in 2021.

First – from 1 April an ‘Innovation and Market Development Fee’ of 0.0025% on transaction values for debits and 0.005% for credit transactions.

Second – Brexit has led to a reclassification of transactions with the UK to be inter-regional, raising the debit fee from 0.2% to 1.15% and the credit fee from 0.3% to 1.5%. It estimates this will cost €15 million in total.

Finally, from 23 January the commercial interchange fee rose as high as 2.3% depending on the payment channel, card type and merchant sector which applied.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.