UK Retailers Demand Intervention as Payments Shift to Cards

The British Retail Consortium (BRC) has just published its 2021 survey of its members who account for 36% of total UK sales from 25,000 shops. While card usage soared, so has the cost of card payments, prompting the BRC to demand emergency intervention by the government to prevent price gouging by the card companies.

The headlines being reported are all about cash transactions halving to 15% in 2021 and the cost of accepting card payments rising to £1.3 billion a year. The BRC uses the findings to call for:

Legislation to stop card fees rising (the Payment Service Regulator (PSR) is reviewing payments but this is taking a long time and in the meantime fees and costs are rising)

The abolishment of interchange fees (in 2020 the UK’s Supreme Court found them to be unlawful)

A Treasury review into the costs of accepting cards.

Some key points hiding in the detail are that cash is the cheapest way a retailer can accept payment, both absolutely and as a percentage of turnover; the use of alternative payments such as Buy Now Pay Later (BNPL) and PayPal has reduced significantly; and the income earned from interchange fees by banks mean that they have no incentive to encourage consumers to switch from card payments to account-to-account (A2A) payments.

Decline in cash use

In addition to fewer cash transactions, as a proportion of total money spent cash has declined from 15% to 8%. The average value of a cash transaction rose from £12.91 to £13.87. While inflation has driven all prices higher, this increase may be because people are making lower value payments with a card rather than with cash.

The BRC points out that as cash volumes fall, the costs associated with cash rise. The BRC is active in campaigning for support for cash infrastructure.

There are a few indications in the survey that show the move away from the high street for shopping is slowing down, if not reversing, which would be good for cash. For example, non-food items bought online has declined from 48.6% in 2021 to 39.9% in the first 11 months of 2022.

When the total UK retail footfall is compared with the pre-pandemic numbers, from January to September in 2021 the lowest fall was 16.9% and the largest 76.2%. In 2022 the comparative figures were 9.8% and 16.64%. Month on the month the decline is less as people return to the high street. Again, good for cash.

Card use

90% of retail spending and 82% of transactions are paid for using cards, up from 67% in 2020. The cost of processing card transactions is now £1.15 billion of the total of £1.3 billion card payment costs.

Sales made paid for by debit card have gone up 4.7% to £421 billion in 2021. According to Accenture, the UK’s adoption of contactless payments is the same as Australia’s, 83% of card payments, significantly more than in other countries. With the contactless payment limit increased to £100, consumers are using cards for lower value transactions. The average debit card transaction value fell from £27.12 to £24.90.

Debit card transactions have risen from 54% of the total, 8.91 billion, to 67%, 11.5 billion. Credit card transactions have hardly changed, rising from 14% to 15%. This suggests that debit cards have benefited from the decline in cash use.

Alternative payments are defined as BNPL, PayPal (and equivalents), gift card and crypto payments. These are generally used for online payments and their use has fallen from 4% in 2020 to 2.4% in 2021. At the same time the value of each transaction has fallen on average from £34.32 to £9.44. It is unclear why this is, although part may be attributed to less online shopping and also some BNPL payments may now be categorised as a card payment.

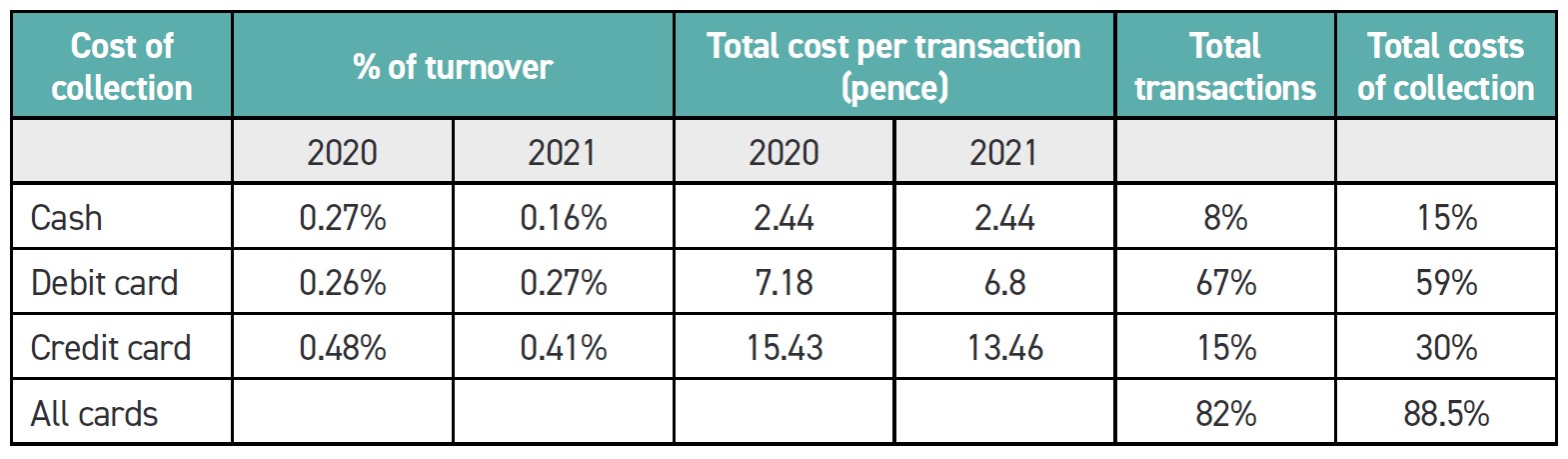

Cost of payments

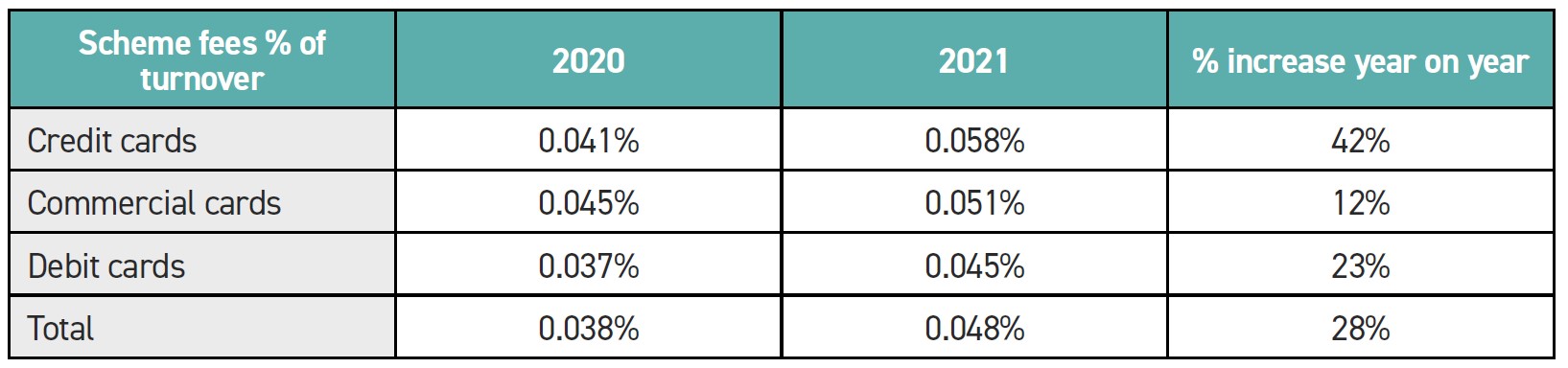

Despite the 2015 Interchange Fee Regulation that was meant to stop this, the average debit card transaction cost has gone up from 0.265% to 0.273%, scheme fees have risen by 28% compared with 2020 and merchant service fees have risen by 12%.

Cash as a percentage of turnover or as a total cost per transaction is the lowest cost payment option, although with a total cost of collection of 15% compared to cash being only 8% of all transactions, cash is more expensive than debit cards and only just better than credit cards.

These card costs, though, don’t include scheme fees.

For debit cards the increase in scheme fees raises the cost per transaction from 1.04p to 1.25p.

In addition, interchange fees have increased 10% as a percentage of turnover and merchant service charges 12%.

For debit cards, which account for 67% of transactions, the 28% increase in scheme fees and 12% increase in merchant services charges, combined with the increase in debit card usage, has seen retailers pay an additional £141 million in charges in 2021.

Final word

With retailers under enormous cost pressures and facing a flight from the high street, this survey explains the BRCs campaign to get the PSR to take action.

It is interesting to view the BRC report in the context of a new report issued by Accenture based on a survey of 3,000 people that says 63% of adults use cash at least five times a month in the UK, only a small step behind debit cards that are used that frequently by 75% of adults.

Credit cards are preferred for people when purchasing big ticket items such as appliances and travel, but 20% of respondents are looking to move away from using credit cards because of their costs.

Accenture concluded that the death of cash is going to take a long, long time. Given the results of the BRC annual payment survey, there is every reason for retailers to work to make this happen.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.