New Report on The Importance of Cash in a Crisis

Professors Gerhard Rösl and Franz Seitz have written a paper in which they compare the handling of the 1929 depression, the 2008/9 recession, India’s demonetisation exercise and Greece’s experience in their sovereign debt crisis and financial challenges starting 2009 until today 1. While the study is primarily about the provision of liquidity into the financial system, it also provides useful insights into the role and importance of cash.

The stock of money in an economy is made up for public money, cash and reserves, and private money, commercial bank money. Over the last few years there has been a focus on the effect of restricting cash use, how cash creates a bottom limit on negative interest rates, what happens to cash in a crisis and the cash paradox when there are fewer cash transactions but rising levels of cash in circulation.

Sadly, the range of crises to study is long – the 2008/9 global financial crisis, India’s demonetisation, the coup in Myanmar, the pandemic, and a series of wars in Iraq, Syria, Afghanistan and Ukraine.

All of these discussions come back to the role of money, which is ultimately underpinned by faith in the stable monetary value of whatever is being used as money. While commercial bank money has been increasing rapidly, so has cash. In most developed countries, apart from Sweden, cash increased at a faster rate than GDP between 1991 and 2021.

Cash usage is often attributed to the wish of people to avoid paying tax and for criminal activity. The data from 2020 during the pandemic questions this assumption. Cash increased but criminal activity sharply decreased. Additionally, the growth in high denomination banknotes in circulation rose more and faster than low denomination banknotes in major currency areas.

The wish of citizens to hold cash when faced with a crisis is a legitimate reaction and action for a citizen.

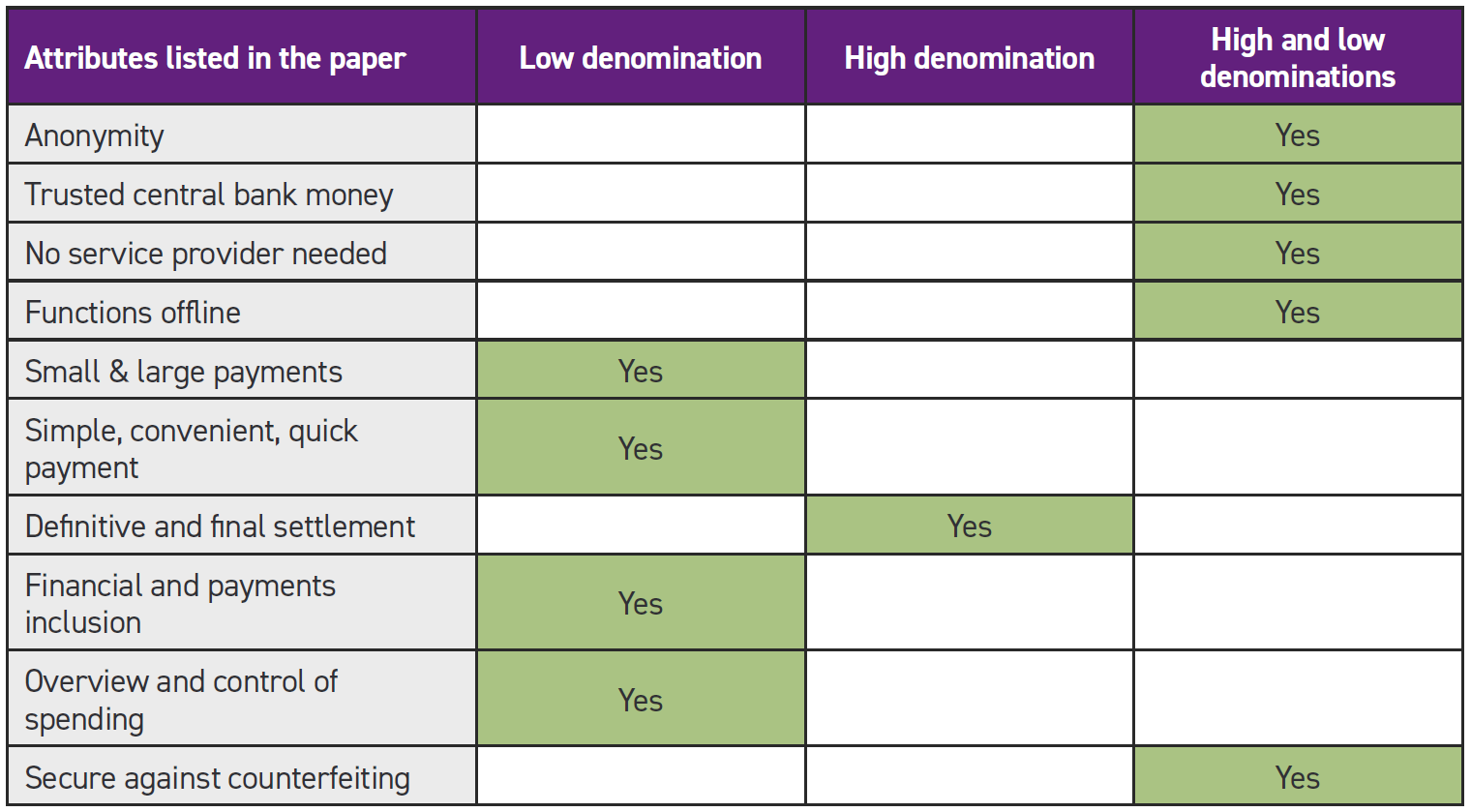

The paper lists attributes which make cash attractive. While all attributes apply to all denominations, it would be interesting to research whether the attributes apply equally to both high and low denomination notes, particularly if central banks, or others, want to create a digital substitute for the store of value role of banknotes. Do some denominations function particularly well for some attributes than others?

Great depression 1929-33

M2, often referred to as ‘broad money’, is the measure of liquidity in private households, firms and the non-banking public sector. It is made up of cash and book money (commercial bank money).

The Federal Reserve did not loosen its monetary policy until late in the great depression. As a result, book money shrank between 1929-1933. Non-bank liquidity fell 33% in December 1929. In this context cash alone is irrelevant unless the withdrawal of cash from a bank leads it to fail, in which case deposits can be lost too. Between 1929 and 1933 the number of US commercial banks fell 40%, with 9,940 out of 24,970 banks suspending operations.

Commercial banks can increase lending to domestic non-bank customers, increase their purchase of net external assets from non-bank customers and exchange the long term deposits of their non-bank customers for more liquid ones. While bank and non-bank liquidity is important, today reaching those needing non-banked liquidity is harder. Credit channels are important but, as was found in the 2008 financial crisis, if consumers don’t want credit, increasing credit availability is not useful.

21st century crisis

In a 2021 paper Rösel and Seitz categorised crisis into three types:

Technology crisis such as the Millennium (Y2K) crisis

Financial market crisis such as the global financial crisis of 2008/9

Natural disasters such as the pandemic.

They argue that the type of crisis determines the denominational demand that will result. The Y2K crisis was about whether people would be able to access and spend cash, so the low denomination notes were demanded. Perhaps a fourth type should have been included, that of war. In March 2022 cash demand in Sweden rose 8% due to the war in Ukraine.

In 2008/9 the annual growth of cash increased by 14% in the Eurosystem, 11% in the US and 10% in the UK. The central banks were able to meet the demand. The notes demanded were primarily high denomination notes.

It is worth noting that bank money and cash are not direct substitutes for each other.

India’s demonetisation

Today India remains a cash economy. In 2021 cash in circulation was worth R30,000 billion while bank deposits were worth R20,000 billion. The Prime Minister of India declared in November 2016 that the two highest denominations would no longer be legal tender from midnight. The 1,000 denomination would be replaced, in due course, by a new 2,000 denomination and the 500 denomination would be replaced, in due course, by a redesigned 500.

The result was chaos, with a monetary contraction of 40% in November and December 2016, an estimated 2% drop in GDP that quarter and a temporary reduction in consumption and increase in unemployment.

The impact was primarily felt by rural communities and the poorest in society. The number of bank accounts and deposits rose only slightly, and the tax base increased only marginally. The majority of notes in circulation were returned, suggesting that the goal of fighting corruption was unsuccessful. The Prime Minister said that prices were artificially high due to the ‘misuse of cash’. Prices did not fall.

It would appear that the demonetisation exercise happened without addressing the reasons cash was so widely used. As a result, the benefits forecast were not delivered.

Greek sovereign fund crisis

Greece experienced a series of financial crises from 2008 followed by the 2020 pandemic. Prior to the crisis, Greece had issued about 2.5% of euro banknotes. Twice during the crisis, in June 2012 and June 2015, it reached over 5%. Cash usage was only reduced by a mixture of capital controls, limits on how much cash could be withdrawn from ATMs and a vigorous programme to encourage cashless payments, including tax deductions, bank loyalty programmes and weekly lottery for those making digital payments. The cash payment limit has been reduced to €500. A 2019 request to the ECB to reduce it to €300 was declined as ‘disproportionate’.

Despite that, in 2020 80% of point of sale and person-to-person payments, by volume, were made in cash and 62% by value. The Eurosystem average was 73% and 48% respectively. Again, cash has remained widely used throughout the crisis because the population needed it for domestic transactions.

Conclusions

The paper made a number of observations. Private electronic money (in the form of bank deposits) is not a perfect substitute for cash because of the unique attributes of cash. The payment mix needs to include cash for psychological as well as economic reasons. The ability of cash to provide non- bank liquidity provides stability across the financial system.

A key point is that in order to fulfil its stabilising functions in times of crisis, cash has to function properly also in normal times. This implies that it should be the task of central banks to guarantee the cash infrastructure even if cash used for daily transactions is declining.

Finally, supply-side driven problems for the cash cycle should be avoided, as the experiences of the demonetisation in India and cash withdrawal restrictions in Greece have clearly shown.

1 - On the stabilising role of cash for societies. Gerhard Rösel, Franz Seitz. Institute for Monetary and Financial Stability. Working Paper series 167 (2022).

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.