Why Cash Automation Makes Sense

Diebold Nixdorf recently presented a webinar on the benefits and logic of cash automation and how to do cash recycling well.

The presentation started with a description of how banks have managed cash services over time. Banks started introducing Teller Cash Recyclers (TCRs) to help tellers handle cash faster with fewer errors and to keep them safe. The teller still managed the interaction with the consumer. Branches then started installing cash dispensers, mono- or multi-function ATM devices and intelligent depositing devices. Self-service had arrived.

Technology has now allowed these self-service devices to offer much more complete and sophisticated self-service options and teller services directly to the public. For example, live video links to bank experts on products such as mortgages, loans, investments etc. Behind the scenes this equipment can also enable branches to do in-branch recycling.

The latest development, which is not necessarily visible to the public, is new operating models where this equipment is offered in partnership and ‘as a service’ on behalf of the bank. Managed services and ATM pooling are real options allowing banks to reduce their branch and cash costs.

Use of machines for cash withdrawals and deposits

Based on Nielsen research with US consumers, Diebold Nixdorf found that while 8% of the public expected to stop using cash in the next two years, 57% expected to maintain or increase their usage. In 2021 42% used cash as payments while shopping in store, down from 53% in 2019.

Based on Nielsen research with US consumers, Diebold Nixdorf found that while 8% of the public expected to stop using cash in the next two years, 57% expected to maintain or increase their usage. In 2021 42% used cash as payments while shopping in store, down from 53% in 2019.

40% of deposit accepting terminals in the US are estimated to have cash in/out ratios that support recycling, ie. their net receipts of cash provide sufficient cash to allow cash re-issue. This has increased by 80% since 2010, 90% of notes deposited are fit for reissue.

Diebold Nixdorf found through simulation analysis that 40-50% of cash in transit visits to ATMs were not necessary.

Consumer frustrations were found to be ATMs that only issue $20 banknotes (91%), waiting times (54%) and the lag between depositing money and it being credited to accounts (38%). They found merchants were willing to consider investing in automation.

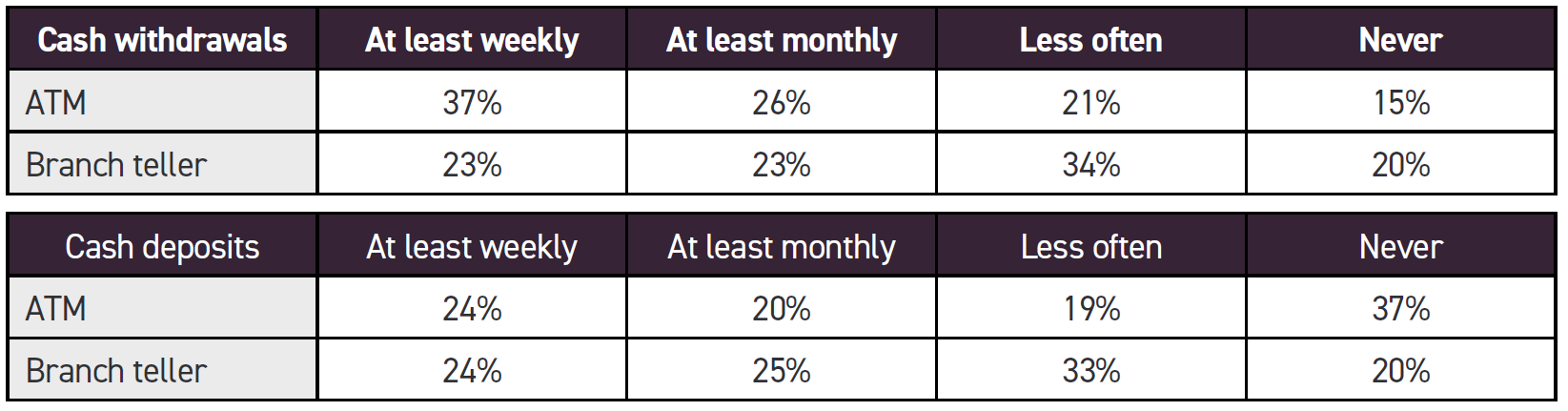

Again, from Nielsen, tellers remain widely used in the US both for cash withdrawals and deposits. The percentages who infrequently withdraw cash perhaps signpost an underlying cash decline, as wells as the challenges of surveys.

It is not clear what the split between merchants and consumers is for this data. It appears that using ATMs for cash deposits is a relatively common event.

Future models

Diebold Nixdorf suggests that ATM cash recycling could cut the number of CIT visits significantly, saving both money and their environmental impact. If a CIT visit costs $45, then cutting the number of visits each week by one would save $2,340 each year.

The presentation ended suggesting the value of cash recycling and cash management to bank branches lies in addressing the frustrations of ATMs that only issue $20 notes and waiting times. It saves the branch money and helps environmentally. It allows consumers and businesses to access depositing and withdrawing cash at times to suit them. It frees up staff for more valuable tasks.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.