The Impact of a Move to Mobile Payments

Does paying with mobile digital payments increase consumers’ marginal propensity to consume? If there is to be an increase in the use of mobile payments this has implications for consumers, merchants and governments. A paper from Claremont Graduate University sets out to answer this 1.

In 2019 in China 347.1 trillion yuan ($55 trillion) was spent using mobile payments and just under 250 trillion yuan ($39 trillion) using third party mobile transaction providers, primarily Alipay and WeChat Pay. Alibaba, an e-commerce platform, started Alipay in 2008 and WeChat Pay, part of the WeChat social media and messaging platform, started in 2013. In China, these two platforms have 90% market share. 94.87% of participants in the research ‘usually’ or ‘always’ used these platforms.

This paper uses data from China, therefore, to answer the question.

Classic payment research evidence: cards v cash

There is extensive literature about paying with cash and cards. The concept of the pain of paying is well known and the literature is persuasive that the decoupling of the pain of paying, and the pleasure of purchase explains why people are more likely to spend when paying with a credit card. A credit card can also address, of course, the problem if the consumer lacks the immediate funds for the purchase.

There is also research suggesting that the form that money takes plays a role in purchase decisions. This is sometimes known as the ‘weapons effect’, where research has shown that the presence of weapons would make people think more about violent behaviour and so elicit more aggressive related thoughts. If a consumer sees the logo of their credit card, this is known to stimulate the likelihood of spending.

The paper lists six research examples of spend behaviour:

Buying sports tickets: cash users spent less although, if the item being bought had a fixed value, the cash/mobile difference disappeared.

Buying a restaurant dinner: cash users spent less than card users.

Paying with cash or a gift card: cash users bought cheaper goods.

Charity giving: cash users gave less. In a field experiment that supported this research, fewer debit card users gave to charity but those that did gave more.

Research about German payment behaviour: when people paid with cash, they were more likely to think that the purchase was necessary.

Paying directly from an account: this focuses attention on the benefits of the good, but people are more likely to make impulse purchases. A study of Chinese banking data found that after people adopted Alipay, transaction values increased by 2.4%.

But does any of this carry over to mobile payments?

Mobile payments: research methodology

The research tested four hypotheses,

H1. People have a higher WTP (willingness to pay) when they paid with mobile means.

H2. People have a higher WTP when they paid with the same form as they received.

H3. The difference between the WTP of mobile payment and cash payment would be higher for goods without a face value compared to goods with a face value.

H4. The difference between mobile vs cash WTP is influenced by subjects’ attitudes toward payment methods and psychological factors. Subjects who are more familiar with mobile payment, or less sensitive to the pain of paying would have a lower payment methods effect.

Two experiments were carried out.

Field test and results

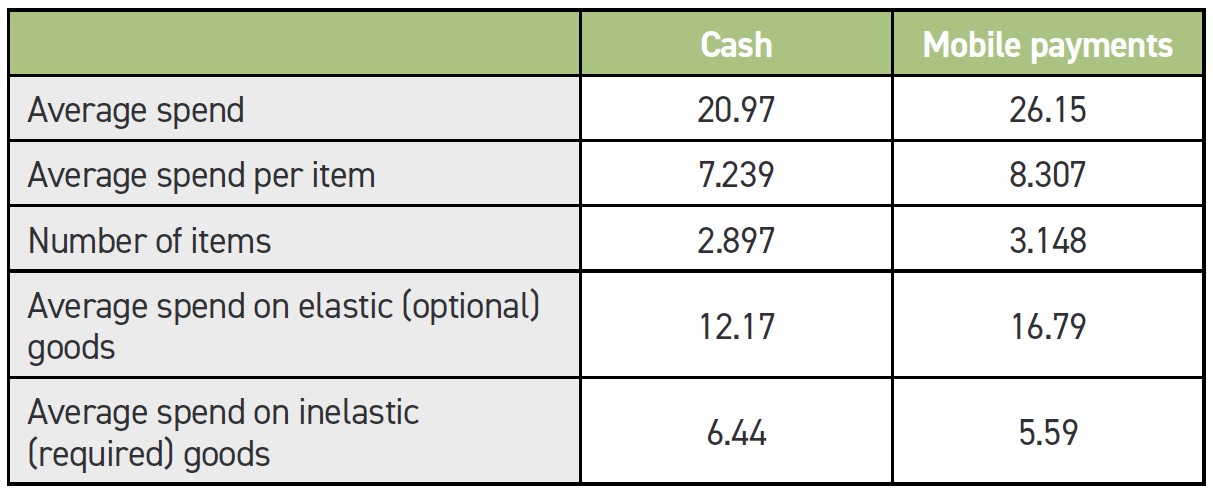

In the first 2,531 receipts were collected from six supermarkets and grocery stores in Beijing between April and May 2018.

People paying in cash had a lower average spend and made fewer purchases than those paying with mobile payments.

Research test methodology and results

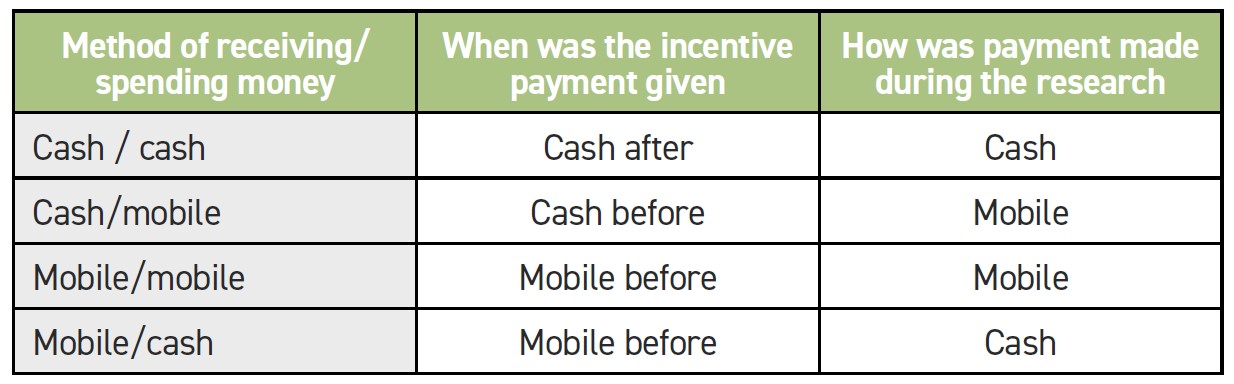

263 people from North China Electrical Power University and the China University of Petroleum took part in an experiment between December 2018 and June 2019. Each person was asked to bring 20 yuan in cash, and each were told they would receive a 30 yuan incentive to take part. These people were divided into four groups, as below.

The research was organised into four parts. Each part was designed to address identified bias in the research, for example it tested whether people were motivated by avoiding the cost of paying for consumption (Behavioural Inhibition System) or to follow their goals (Behavioural Activation System).

The participants were questioned on their willingness to pay (WTP) for a McDonalds gift voucher (worth 20 yuan) and for a mug (with a value of 20 yuan), ie. what they were prepared to pay.

Participants were then told the value of each item. The price was randomly generated.

They bought the products.

Participants were then asked views of paying with mobile payments in general.

The four groups were necessary to address whether people were more likely to buy if their incentive was in the same form as how they were being asked to pay (known as earmarking).

The type of good did not affect the result.

Whether the personality of the person was to be a ‘spendthrift’ or ‘tightwad’ did not affect the result. Earmarking did make a decisive difference. People were more likely to buy if their incentive was in the same form as how they were paying.

Key findings

On first reading of this research, it appears that the payment behaviours associated with mobile payments are closer to credit cards than cash.

Consumers: Pay using cash if you want to reduce your consumption of elastic (optional) products/services.

Merchants: Increased use of mobile payments is profitable because consumers increase how much they buy and their average expenditure.

Policymakers: Moving to mobile payments can stimulate domestic demand and it can be used to foster public services. However, beware encouraging people to purchase addictive products or to overspend. Financial awareness is key to avoid this. Increased velocity of money circulation can drive inflation.

Remarks relevant to specific hypotheses included that the different levels of pain of paying didn’t significantly influence the WTP.

Mobile payments are a positive driver for purchasing (BAS) rather than a negative (BIS).

The research found that the attitude towards mobile payment and the frequency of relevant payment methods do not motivate the mobile effect. This could be because the subject pool was drawn from undergraduates of a similar age or because different payment progress involves deeper psychological needs that work similarly for all subjects even if they have different consumption attitudes.

1 - The Influence of Payment Method. Do Consumers Pay More with Mobile Payments? Yizhao Jiang. Claremont Graduate University 2022.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.