The UK’s Path to Digital Inclusion

A recent webinar organised by Enryo, an independent consultancy, invited four experts to consider digital inclusion. Speakers addressed how to overcome the very real problem of proving identity and what needs to be done to accelerate digital inclusion. This was counterbalanced by updates on how areas facing cash challenges are being helped, and survey results showing where cash is today in the UK.

In a panel discussion at the end there was general agreement that the UK needs an independent review, similar to the Access to Cash Review, to present a pathway to digital inclusion that delivers universal access to digital payments and digital identity.

There was a view that with cash use falling, the cost of the cash infrastructure is rising, which means that the ready availability of cash as people experience it today could soon end. Hence this webinar and the need for urgent action.

Financial exclusion and the identity challenge

Dr Sarah Walton from Counterpoint presented on the role and importance of identity. Although the research reported was on the UK, the work is now being extended to drive for an international identity code of conduct.

In the UK identity is usually proved by presenting a passport or driving licence, which include the individual’s photograph, and a document such as a utility bill with an address. The research found that 5.9 million people are ‘identity challenged’, with no passport or driving licence and no financial data history. Five segments accounted for 3.6 million people:

Rural solitude: 66+, in work, no qualifications, rural (0.3 million).

Vintage veteran: 66+, retired, no qualifications, rural (0.8 million).

Budgetary families: 26-45, in work, basic education, urban (1.2 million).

Urban renters: 26-35, in work, some qualifications, urban (one million).

Community culture: 26-45, some education, urban, multinational communities (0.3 million).

Other sources of identity reviewed included online banking history, health service patient number (NHS number), tax number (National Insurance number), local tax record (council tax) and educational records (learning records service).

The presentation suggested that a rethink is necessary to consider identity as an ecosystem where requiring a narrow range of documents does not work. Identity needs to be based on proportionality with a tiered ‘know your customer’ (KYC) requirement, vouching (people live in communities where they are known, so others should be able to confirm who you are) and eKYC.

Most of the source identity documents identified are government documents. There is a need to make people’s lives easier, particularly those leading unordered lives, and so the state needs to work across its databases to help link people to their records.

Increasing access to digital inclusion

Dr Ruth Wanderhöfer looked at the challenges, outcomes and actions relating to increasing financial inclusion in the UK. There is a need to develop a route to digital inclusion that does not leave consumers or businesses behind. It is clear the UK needs to be bolder and to use the opportunities that major changes in finance are bringing. At the moment there are too many barriers and there is the need to try harder, to do better.

She defined the goal as moving more people to using digital payment solutions by making this quicker and easier and ensuring people know how different payment choices work, their advantages and disadvantages and the different levels of protection against crime that they offer. Dr Wanderhöfer made the point that for this to work, both consumer and merchant must be happy to use digital payments.

The financial innovations that offer opportunities for innovation were open banking, which could offer alternatives to paying using direct debits, variable recurring payments and requests to pay to avoid bounced direct debits, the roll of third party providers in the context of app scams and the roll out of CBDCs and digital ID.

The presentation identified a number of general barriers and then consumer and merchant barriers to the adoption of digital payments.

General barriers. These were inertia, lack of control and safety and convenience.

People dislike change ‘when there is no obvious tangible incentive that they can see.’ Consumers don’t see the cost of payments and so regard all payments as free. It is interesting that the word ‘incentive’ was used, rather than ‘benefit’.

Digital payments may be convenient but they are not tangible, and so they are not as effective when it comes to budgeting.

Finally, there is increasing awareness of digital fraud.

Consumer barriers. Lack of clarity of the protection against fraud and loss for different payment choices, a lack of understanding of what digital payments are (people don’t understand the difference between a wallet which has card details logged on it and true mobile wallets which don’t involve cards) and a real risk that one bad experience of paying digitally or using a digital tool (Buy Now Pay Later was specifically mentioned) and people may be put off adopting digital payments.

The risk of additional charges, whether for a bounced direct debit, bank fees or account charges was also seen as a risk.

Merchant barriers. For merchants the cost of payments was a significant concern. It appears they struggle to find direct debits at an acceptable price, experience high rates of failed payments, delays in payments and slow settlement and cash management can be a problem area.

Within cash management there can be a lack of data for reconciliation, a lack of real time balances and unattractive liability and charging structures.

Just ‘trying harder’ does not seem like a solution in the face of the goal and the barriers outlined.

Provision of infrastructure to maintain access to cash

John Howells, CEO of LINK, which runs the UK’s largest cash machine network, looked at what has happened to cash in the UK since 2019. In 2019 cash withdrawals fell 10%, so the downward trend was long established. The evidence shows that a major drop has occurred but has currently plateaued out. LINK regard this as a fundamental change to which the UK must adapt.

A map was presented showing the 3,400 ATMs in the UK that are either protected ATMs (1km from the next free to use ATM, also known as ‘lonely’ ATMs) or ATMs installed to maintain financial inclusion. The location of these ATMs are, effectively, a map of social and economic deprivation in the UK.

Protected and financial inclusion ATMs are two of five changes introduced to the UK following the 2019 Access to Cash report. The first was the creation of a Consumer Council which, chaired by an independent person, brings together consumer groups and ATM operators.

Two further changes were a response to where ATM coverage fails. Firstly, direct ATM commissioning and secondly what is known as ‘suggest a site’. These allow areas without sufficient ATM coverage to ask for help. LINK assesses the opportunities. To date, over 100 ATMs have been installed through direct commissioning. The cost of these changes to maintain ATM access is £15 million per year.

He also shared data on ‘cash-at-till’ which started in October 2021. Legislation was passed that allowed consumers to withdraw cash in participating retailers without making a purchase. There are 1,700 terminals signed up and 80,000 cash withdrawals have been made with a value of £1.8 million to date. Encouragingly this figure is increasing at the rate of about 20% week-on-week.

In December 2021 the UK banks agreed to share services to ensure that communities have fair access to cash. LINK will independently assess communities and can commission services where they are needed. These may be shared banking hubs, free ATMs, enhanced post offices or cash at the till solutions.

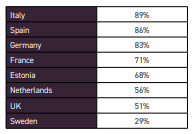

Finally, he made the point that the percentage of population across Europe who use cash week is high, although reading the media you might not think that. Even in Sweden 29% use cash each week.

COVID-19: The impact on consumer daily habits and the use of cash

Finally, LINK presented survey data commissioned from Enryo based on February 2022 research into the impact of the pandemic in the UK.

Compared with 2020, 70% of those surveyed were using cash less, 25% about the same and only 4% more. Perhaps the finding that 22% used cards rather than cash because retailers were discouraging them from paying with cash and another 13% said that they hadn’t been able to pay with cash at all may help explain those figures.

Asked about their use of cash in the next six months, 35% said they would use about the same as now. 8% said they’d use more cash because of the need to budget in the face of inflation.

When asked about future cash usage, 10% already don’t use cash, 32% said they’d use less, 13% more and 39% no change.

The top three places for using cash were convenience stores (24%), supermarkets (22%) and person-to-person payments between friends and family (18%).

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.