Shoe Leather Costs of Cash Withdrawals in Canada

The Bank of Canada wanted to understand the impact on cash withdrawals if people had to pay more to access cash. Staff working paper 202128 considers this question 1.

When it comes to cash withdrawals, a key cost for economists is the time and effort needed to access cash. This component significantly exceeds that of transfer fees or other charges for cash withdrawals.

Although this area has been studied by others, the Bank set out identify those who did not have to ‘spend’ time and effort because they were passing bank branches and ATM equipment as part of their daily routine from those who had to make a special effort. They could then establish the impact of this time and effort on the demand for cash.

Structure of the study

The paper used micro-geographic individual-level data from the Bank’s 2009, 2013 and 2017 Methods of Payment (MOP) surveys of monthly withdrawal behaviour and demographic characteristics. The bank branch network is directly related to consumer cash accessibility. Most financial institutions co-locate their ATMs at their branches and so both were included in the cash data.

With the goal of studying the marginal effect of what the paper called ‘shoe leather’ costs 2 on the withdrawal frequency of cash, the study measured the distance between the financial institutions, bank branches, and consumer residential locations. The focus was on the nearest bank branch that individuals banked with, ‘their bank’, rather than the nearest bank branch of any sort near to the consumer.

The research only looked at urban areas because this gave the greatest density of branches, reducing other variables from affecting the results. For example, in urban areas people are not forced to use ‘white label’ ATMs that have extra charges associated with cash withdrawals. They have sufficient alternatives not to have to use them.

A small proportion of consumers are associated with costly withdrawals. A subset withdraw cash as they pass free cash and/or convenient cash withdrawal opportunities. Their cash withdrawals are random in that they seize the opportunity as they come across it. The study removes these consumers, creating two main groups:

Those using free or convenient cash withdrawal opportunities

Those for whom withdrawing cash is costly, particularly in shoe leather.

An increase in online transactions is reflected in a reduction in cash withdrawals.

Transactions made online, using mobile devices and apps or Interac e-transfer, mean there are fewer free withdrawal opportunities because these people have fewer physical interactions with the physical network.

The reduction in the number and probability of free withdrawals and, therefore, a reduction in the absolute number of free withdrawals, increases the probability of being selected as being a costly withdrawal, increasing the chance of self-selecting as a group. The study corrects for this bias.

The importance of ‘shoe leather’ costs

In the 2013 and 2017 MOP surveys, the average replenishment trigger to take advantage of convenient withdrawals (ie. free type) was 2.78 and 1.42 times greater than all other withdrawals. Consumers balance off shoe leather costs compared with fee costs.

The shoe leather cost of 1 km was 4 and 13 cents. 89% of consumers incurred no withdrawal fees, reflecting consumer’s willingness to travel rather than to pay additional fees. The threshold effects of distance on typical monthly withdrawal frequency was found to be significant.

If respondents lived within 1.56 km of their affiliated financial institution, a 1 km reduction in distance was associated with an average marginal increase of 0.31 withdrawals per month.

If consumers have to travel over 1.56 km, the distance has a marginal influence on cash withdrawal decisions. It is assumed that most people will walk up to 1.56 km, but beyond that they will choose to drive, at which point the cost/benefit equation changes significantly. This finding applied to all demographics.

In terms of heterogeneous effects, distance plays a larger role for both higher income and older-age groups. One thought is that time matters more for higher income people, hence this result. Younger individuals were less responsive to changes in distance, probably because they have a lower opportunity cost.

The study found that those seeking free cash withdrawals replenished their cash holdings earlier than those prepared to expend shoe leather. Rather than wait until their cash balances get to zero, they restock as and when they can.

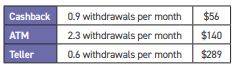

The 2017 MOP found that people withdrew cash on a different monthly frequency depending on the cash source. There was also a difference in how much was withdrawn:

The report’s conclusion was that cashback is an important source of cash. The authors plan to go on and look at the location of retail stores in a future study.

Final thought

This is an interesting piece of work for those looking at the optimal density of places where people can access cash. It also has implications for those proposing ATM fees, although the authors are planning further work to understand the impact of cash withdrawal fees, which will also shed light on this issue.

The report also adds some credence to the decision of economists to regard shoe leather costs as an important consideration for consumers, whether conscious or unconscious.

1 - Staff Working Paper- 2021-28: Consumer Cash Withdrawal Behaviour: Branch Networks and Online Financial Innovation. Heng Chen, Matthew Strathearn and Marcel Voia.

2 - Shoe leather being the time and effort taken to withdraw cash deliberately rather than in passing.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.