Effective, Efficient, Sustainable and Resilient

In many countries the COVID-19 pandemic has seen cash in circulation reach record levels, yet, with diminished economic activity and a push towards ‘contactless’ payments, transactional cash use has continued to decline. As a result, many central banks around the world are actively reviewing their country’s cash infrastructure and are busy considering whether their mechanisms for the distribution of cash remain effective, efficient, sustainable, and resilient.

In the UK, the Bank of England has recently issued an update on 18 months of work by its Wholesale Distribution Steering Group (WDSG), made up of key industry stakeholders from across the cash supply chain, which is considering the future state of the UK’s wholesale cash distribution system.

On the other side of the world, both the Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand (RBNZ) are in the midst of consultations to determine similar issues in their countries.

While the stages of work and approaches taken in each country are different, the common theme is the recognition that the wholesale cash systems and roles that each central bank play in the supply and distribution of cash need to adapt.

Infrastructure, policies, and processes developed, in some cases many years ago when cash use was significantly higher, are increasingly no longer ‘fit-for-purpose’.

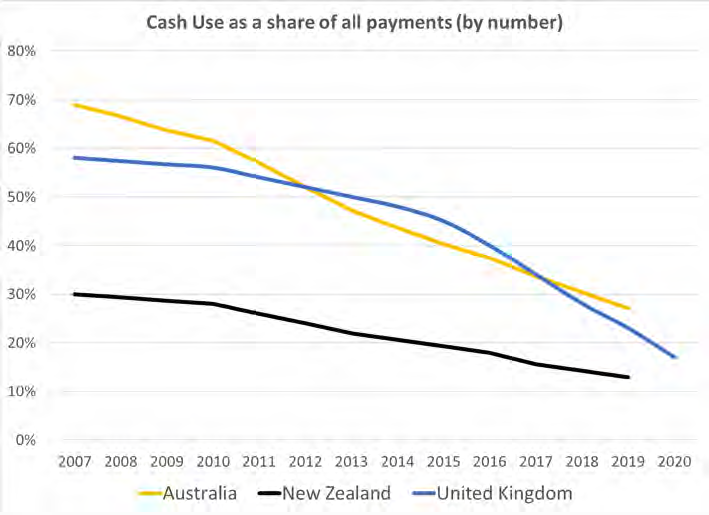

Declining transactional cash use

Australia: Reserve Bank of Australia Consumer Payment diaries, Cash Payments; Share of consumer payments by number. New Zealand: Stats NZ, The Number of Cash Payments as a Percentage of all Household Payments. United Kingdom: UK Finance, cash share of total UK payment volumes.

Australia: Reserve Bank of Australia Consumer Payment diaries, Cash Payments; Share of consumer payments by number. New Zealand: Stats NZ, The Number of Cash Payments as a Percentage of all Household Payments. United Kingdom: UK Finance, cash share of total UK payment volumes.Common across Australia, New Zealand and the UK has been the general trend towards using less cash. The growth of online shopping and active promotion of contactless payments (especially debit cards and mobile payments) have all contributed to a decline in day-to-day cash payments. The pandemic has hastened these trends, with higher contactless payments limits (despite the increased fraud risks) and a desire to limit physical contact all precipitating the underlying trend to use less cash.

Set against this, in these countries and many elsewhere, the desire to hold cash as a safeguard and store of wealth has seen cash issued by the central bank (especially in higher denomination banknotes) reach all time highs. The divergence between cash demand and cash use is presenting significant challenges and raises questions about who across the supply chain should be responsible for and bear the cost of cash.

‘Wholesale’ cash

The UK steering group, the RBA’s Distribution Arrangements paper and the third RBNZ issues paper all focused on what is termed ‘wholesale’ cash, in other words the bulk supply of cash (banknotes and in some cases coin) from the central bank (and mint) to and back from the commercial world (via banks and cash management companies).

While there is broad agreement across most stakeholders that this infrastructure, or the ‘rails’ on which cash is moved, needs to be fit for purpose, when one starts to stray into the retail or commercial aspects of cash handling (which are closely intertwined), reaching common consensus on the way forward becomes increasingly problematic.

The cash needs and approach taken by a bank that has a strong commercial cash base tightly linked to its transactional banking services is likely to be significantly different to the cash strategies of other banks that might be more focused on ensuring their retail customers can meet their cash needs at an ATM or across a branch counter. Cash management/cash in transit companies will take their own competitive stances and, while having common concerns, are often fierce and formidable rivals.

Therefore, charting a common course is no mean feat.

Access to cash

With a drive towards digitalisation and fewer in person transactions, there have been substantial bank branch and ATM closures and consolidation, with consequent challenges to both access to and acceptance of cash deposits.

While true of all three countries, perhaps the greatest attention to the issue of reduced cash access has been in the UK, and to that end pioneering work has been done, such as the publication of the independent Access to Cash Review, which in March 2019 concluded that the UK ‘is not ready to become a cashless society’.

One initiative prompted by the work was the formation in May 2019 by the Bank of England of a Wholesale Distribution Steering Group (WDSG) with a clearly defined brief to consider whether or not the UK’s Wholesale Cash Distribution model remains effective, resilient, and sustainable. In 2020 independent industry analysis commissioned by the group determined that a consolidated ‘utility’ model might be the best way forward to meet cash distribution needs.

The wholesale cash utility was defined as a single consolidated entity formed and funded by a number of wholesale cash providers and operated as a single new entity, with its own governance structures and arrangements.

Insufficient support

Over 18 months or so, including through the height of the COVID-19 pandemic, the group worked to consider the merits of such a utility, appointing legal firm Eversheds to support the challenges of navigating competition compliance and using accountancy firm KPMG to undertake a detailed business case development and costings.

Despite this collaborative and in-depth work, ultimately the group concluded that there was ‘insufficient support for a utility model, and that at this time the actions of individual members, guided by the WDSG success criteria, are best placed to deliver the required modernisation of the UK cash infrastructure’. In the absence of a utility solution, the WDSG has agreed that a series of industry-wide commitments will help ensure that the wholesale cash infrastructure continues to support the effective provision of retail cash.

Drawing on the learnings of this earlier work, the Bank has asked each stakeholder in the wholesale cash supply chain to set out in detail how they will contribute towards the delivery of these industry- wide commitments.

The Bank intends holding each bank or wholesale cash operator accountable for meeting its individual commitment and plan. To help support this, the UK Treasury will provide the Bank with the powers that it needs to keep the wholesale infrastructure sustainable and resilient into the future.

The updated was published just before Christmas, alongside announcements by the UK’s Cash Action Group that outlined a series of commitments to protect access to cash and deposit services for households and businesses across the country.

The Bank has also announced that during this year it is going to undertake a detailed review of its Note Circulation Scheme (NCS), the rulebook that governs the Bank’s relationship with the commercial sector, and in particular the arrangements that underpin the storage, sorting and distribution of banknotes.

Australian note distribution review

In Australia, the RBA sought industry feedback to an issue paper it published in November, inviting responses by late January 2022. The very focused issues paper sought comment on the RBA’s own rulebook, the Banknote Distribution Agreement, a set of contracts between it and the four major commercial banks that lays out rules for wholesale cash movements, compensation of cash held at designated approved cash centres and arrangements for measuring, rewarding and/or penalising banknote quality and fitness sorting.

As in many developed countries, the Australian cash ‘ecosystem’ is complex and comprises several major organisations of scale and many other smaller companies that contribute to its operation.

While the RBA’s legal agreements are with the four Australian Cash Distribution and Exchange System (ACDES) banks, the bulk of the actual wholesale cash handling is undertaken by cash management companies, the lion’s share of the work being done by the largest two companies that have national operations across the length and breadth of what is a vast country.

The two big players have been traditionally fierce rivals and fought keenly to win retail and bank business. With reduced bank branch and ATM numbers and lower transactional cash volumes they, and others, are under increasing structural strain.

In its paper the RBA acknowledged that there was considerable spare processing capacity across the country’s approved cash centres and estimated that cash demand could potentially be satisfied with 20-30% fewer sites.

While individual companies have already consolidated some of their centres to maintain their businesses, more co- ordinated or extensive consolidation is likely to raise competition authority issues and, given the geography of the country, present real operational challenges.

Currently, compensatory interest is only paid on verified cash holdings, so delayed processing comes at a cost if cash needs to be moved great distances. While interest rates are currently low the lost interest is also minimal, but with upward interest rate pressures – as we are starting to see – the costs of holding cash without compensation will mount.

In its paper the RBA makes a number of suggestions as to how the future state of cash distribution might look, and it too floats the idea of industry consolidation and some type of utility model. It will be interesting to see if this idea gains transaction, or, like the UK, different competitive stances make common agreement difficult.

The RBA is now analysing the responses received and engaging directly with several of the main industry stakeholders to explore the issues raised and suggestions made. First reporting back to the RBA’s Payments System Board, the RBA intends publishing a paper setting out stakeholder feedback and recommendations in the second half of this year.

Te Moni Anamata (RBNZ)

The RBNZ has also been actively discussing the Future of Money. Consultation on cash system redesign (see Currency News January 2022 for more details) is the third paper in a series that has first considered the broader issue of cash stewardship and separately the prospect of a Central Bank Digital Currency.

RBNZ has taken a much broader approach to its consultation process, inviting widespread comment from not only cash system stakeholders, but the wider public and industry. As such, RBNZ has received several thousand responses to its three consultation papers, including many from members of the public.

A key takeaway from initial analysis is the importance the public attach to access and availability to cash even if they aren’t regular cash users themselves. This role for cash as a means of payment for consumers that don’t have access to other forms of payment, or have limited financial literacy, is an important consideration in determining whether cash is a ‘public good’ which should be supported (and potentially paid for) at a state level.

The RBNZ is now busy analysing responses, engaging with some of its principal cash stakeholders and working towards publishing next steps.

With cash remaining both an essential store of wealth and safeguard and for many an important means of payment, the infrastructure that underpins it needs to remain fit-for-purpose. It will be interesting to follow news of how each of these three countries adapt and respond to changing cash demand.

Paul Blond is Managing Partner of cash and payments consultancy The Blond Group LLP based in Australia and the UK, and has worked closely with clients on these consultations.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.