How Profitable are Credit Cards?

In 2019, 75% of US households had at least one general purpose credit card. Revolving consumer credit at the end of 2021 was over $1 trillion. In this context, the US Federal Reserve has issued a FED Notes on credit card profitability 1.

While most analysis uses bank-level regulatory data, which means the best that can be achieved is bank-level profitability to be calculated, this study uses data on the credit card portfolios of some of the largest credit card lenders in the US. The data covered 80% of the cards issued. Based on this, the study looks at the drivers of profitability to understand both sources of profit and the business model of credit cards from the perspective of both issuers and borrowers.

Sources of income

Transaction income is the income from the interchange fees paid by the merchant’s bank to the cardholder’s bank.

Credit income is the interest earned on outstanding card balances at the end of the month.

Usage fees, which also include late fees, over limit fees, foreign exchange fees and others. These are not incurred by all types of card.

Other income sources include balance transfers, pre-payments and miscellaneous other sources.

Sources of profit

Credit income generates 80% of profits, usage fees 16% and other income 7%. Transactions are a negative at -4% due to the costs of rewards and other expenses being greater than interchange fees. The Net Credit Margin (NCM) trend is similar to the total profitability trend, reflecting its role generating the largest proportion of profit.

Over recent years the net interest margin on revolving balances (balances carried forward from the previous month) has been increasing. However, the Net Transaction Margin (NTM), which is the card lender’s net income on credit card purchases per dollar of purchase value, has been reducing because of the increase in expense of proving rewards. This has been made worse by an increase in people using reward cards to collect reward points.

In 2015 reward expenses represented 3.5% of the quarterly average purchase volume. In 2020 this was 4.4%. Air mile reward points are the most popular reward collected.

People who revolve their balances at the end of each month are known as ‘revolvers’ in this report. Revolvers pay the majority of interest charges and usage fees, including both late and annual fees. Revolving balances are highly seasonal but they have been gradually declining over the last few years.

Consumer definitions

Heavy revolvers – people who roll over their end of month balance every month

Light revolvers – people who roll over their end of month balance between one and 11 times each year

Transactors – people who don’t pay interest because they pay off their balances every month

Other – either inactive accounts or accounts without 12 months of history, usually new accounts.

Who pays what?

Who pays what?

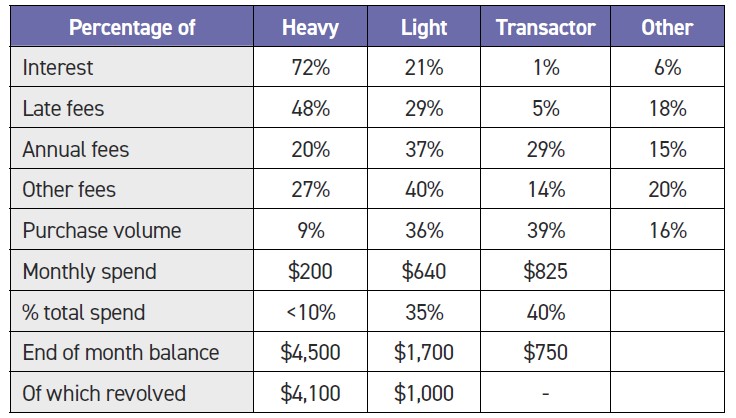

Between 2014-19, revolvers accounted for 50% of accounts, of which 20% are heavy and 25% are light revolvers. Transactors were 21%, inactive accounts 16% and insufficient history accounts for a further 16%. Unsurprisingly heavy revolvers had lower credit ratings and incomes than light revolvers, who had lower scores than transactors.

Who pays the most?

Heavy revolvers accounted for 50% of all balances and 66% of revolving balances. Light revolvers accounted for 22% of revolving balances.

Heavy revolvers paid $60 in interest each month accounting for 70% of all interest paid. They paid 50% of late fees. Light users paid $15 in interest each month, 20% of all interest and 30% of late fees.

In contrast transactors and light revolvers paid the majority of annual and other fees, 30% and 37% respectively. Heavy revolvers paid less than 20%.

Overall heavy and light revolvers paid the bulk of both interest charges and fees.

Final word

Perhaps it is little surprise that people are turning to cash in difficult times when those with the most financial challenges are paying the most for payments.

Equally two pieces of legislation currently in the Senate have also been put forward in the context of helping those with low incomes retain choice and to make payments cheaper.

The first is the Credit Card Compensation Act, and the second is the Payment Choice Act of 2021 put forward in July 2021, sponsored by Representative Donald M Payne Jr, designed to ‘prohibit retail businesses from refusing cash payments, and for other purposes.’ The bill has passed in the House of Representatives and now needs to be passed in the Senate.

Key points in the Payment Choice Act include:

Requires retail businesses – those that sell or offer goods or services at retail to the public and accept in-person payments at a physical location – to accept cash as a form of payment for sales in amounts less than $2,000.

Prohibits them from charging cash-paying customers a higher price compared to customers not paying with cash.

Provides for enforcement through preventative relief and civil penalties.

This research by the Federal Reserve also points to the court cases and investigations being conducted across a wide range of countries in the cost of payments.

1 - Robert Adams, Vitaly M. Bord, and Bradley Katcher.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.