PSR Recommends Payment Fee Cut

In addition to the British Retail Consortium providing detailed information on the cost of payments in the UK, the Payment Systems Regulator (PSR) has recommended a cap on cross-border interchange fees, following its market review of the fees.

The fact that the Canadian government has recently come to an agreement with Visa and Mastercard to lower their interchange fees shows it can be done. From Autumn 2024, small businesses and non-profit organisations with less than $300,000 in Visa sales and less than $175,000 in Mastercard sales will qualify for fee cuts of up to 27%.

This recommendation by the PSR has been driven by the increase in fees imposed by Visa and Mastercard on the UK when it left the European Union (EU). It wants to lower the cost of accessing the EU market for UK merchants, since interchange fees can be one of the largest costs for merchants when accepting credit or debit cards.

Mastercard and Visa increased charge fees on UK to EU card-not- present (CNP) transactions from 0.2% to 1.15% for debit cards and 0.3% to 1.5% for credit cards.

While in the US and Canada, the average interchange fee is currently around 1.81%, the European Commission introduced legislation in 2015 that capped interchange fees within the EU at 0.2% for debit cards and 0.3% for credit cards. The new changes proposed in Canada would bring this down to an annual weighted average interchange rate of 0.95%, saving eligible Canadian small businesses about $1 billion over five years.

What are interchange fees?

Interchange fees are the charge made to a merchant’s bank account when a consumer uses a card to make a purchase. The acquiring bank, that of the merchant, pays the issuing bank, that of the consumer.

Fees are initially collected by the customer’s card provider, like Visa or Mastercard, and paid to the issuing bank. Visa and Mastercard are not issuing banks, so they charge a ‘network fee’ from each transaction that comes out of the merchant’s total processing cost. Fees are calculated as a percentage of the transaction value.

Implications of high interchange fees

The PSR reported that, in 2022, Mastercard and Visa fees increased by approximately £150 million to £200 million, paid by merchants and, ultimately, consumers. It argues that these price increases are evidence of a lack of effective competition, which is to constrain Visa and Mastercard in the setting of cross-border interchange fees.

The PSR makes the point that without a cap, Mastercard and Visa are able to raise these fees. As a result, the proposal is for an initial time-limited cap of 0.2% for UK-European Economic Area consumer debit transactions, and 0.3% for consumer credit transactions. This would be followed, in due course, by a lasting cap on these interchange fees. Analysis will be needed to establish the appropriate level.

Holiday pricing of card fees

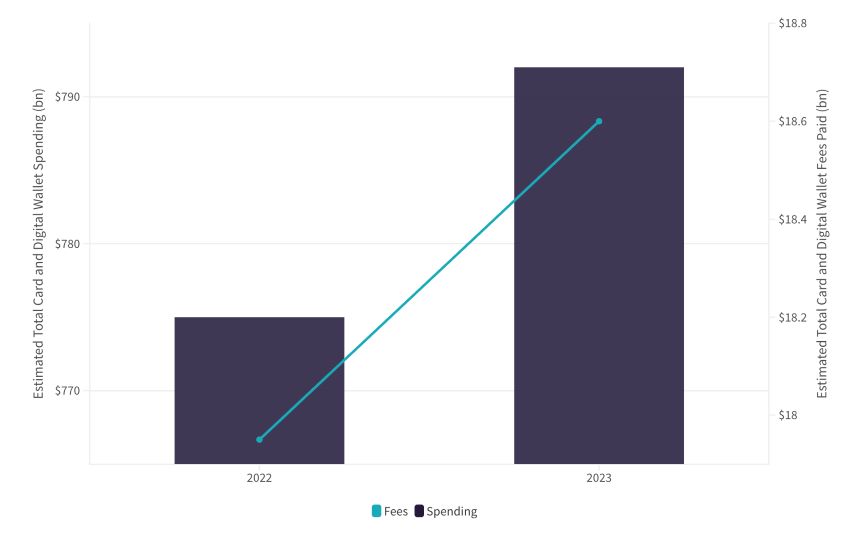

CMPSI has published a report on US card fees over the December holiday season1. The National Retail Federation expects card acceptance fees to be $600 million more in 2023 compared with 2022, ie. fees of $18.6 billion on a spend of $967 billion. From 2022-2023, holiday card fees grew twice as fast as the total holiday card expenditure.

Growth of card fees and consumer spending during the US December holiday season.

Some of this increase is explained by the growth of online spending and the additional fees charged for online payments, which are nearly 50% more than spending in shops. E-commerce spending rose by nearly 7% from 2022-2023 and now represents nearly 30% of holiday spending.

Visa and Mastercard increased fees earlier in 2023 and CMSPI estimate this will add an additional $500 million to the $160 billion already paid by US retailers.

.jpg)

Comparison of published interchange and network costs for credit cards on a $50 transaction.

.jpg)

Comparison of published interchange and network costs for debit cards on a $50 transaction.

The cost of credit card payments is greater than debit card costs. If all payments were made on credit cards, CMSPI estimates retailers would pay about $8 billion more than they do with the current mix.

1 - Unwrapping Card Fees This Holiday Season – CMSPI GlobalSubscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.