A2A Payments Make Progress

Account-to-account payments (A2A) have been talked about for some time. There is some evidence that they are beginning to fulfil their promise. The latest 2023 Worldpay Global Payments Report from FIS says there are now 64 real-time payment schemes in operation providing high-speed payment rails for A2A payments. While this is only up from 60 in 2021, A2A transaction value has risen 13% to $525 billion.

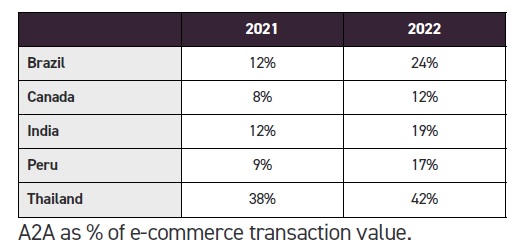

This growth has been helped by a number of key payment systems being A2A capable. Brazil’s Pix payment system doubled the share of e-commerce A2A transaction values between 2021 and 2022. India’s Unified Payments Interface succeeds based on its seamless interoperability with Paytm, PhonePe and GooglePay. Thailand’s PromptPay service, based on real-time proxy payments, is driving innovations such as corporate identification proxy, QR retail payments and request-to-pay functionality.

While A2A payments have been popular for business-to-business and person-to-person payments for some time, person-to-business payments are now starting to happen. A2A payments are not intermediated by major card networks saving on fees. They are also instant, which helps merchant cash flow.

What’s in a name? ACH becomes A2A

A2A payments have, of course, been around for some time, more easily recognised as bank transfers. These have happened for years based on Automated Clearing House (ACH) systems. It is the development of application programming interfaces (APIs) that has brought bank transfers, A2A payments, into the modern world. APIs are allowing people to buy easily and quickly.

The API allows the user to log onto their bank and instruct it to provide account details and the routing number to the processor and for the sale to be processed. The merchant does not see that sensitive data. Once the processor has the details, which are saved as a token, consumers don’t have to log into their bank again and repeat payments are straightforward.

Despite this inherent security, when surveyed, only 22% of respondents regard bank transfers as being secure. The public are unfamiliar with the A2A option at checkout, despite being comfortable with bank transfers. For recurring payments people seem happier to use A2A payments, although they need to be reassured that they can cancel payments if they want to.

An additional benefit for merchants is that fewer transactions are declined because the funding source being authenticated is the customer’s bank account. In e-commerce returns are now a major part of the business experience. A2A refunds are more straightforward as well.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.