Cash Recovering and Holding On, Says BIS

The Bank for International Settlements (BIS) Committee on Payments and Market Infrastructure (CMPI) consists of 14 Advanced Economy (AE) and 13 Emerging Market Economy (EME) countries. It collects extensive data on their cash and electronic payments and uses these to draw conclusions about payment trends. Data collection is always significantly behind the fact, and it has recently issued its 2021 report 1. Despite the time lag, it contains some useful insights and thoughts.

The takeaways offered by the CMPI are that public demand for cash remains steady both as a means of payment and as a safe haven. Digitalisation is a global phenomenon, but between countries payment habits are very different. The next major leap forward will be if the interoperability challenges can be overcome to allow faster payments across borders.

What is changing?

Technology, and investment in infrastructure, is delivering a steady stream of developments such as smartphones, increased internet network coverage, more point of sale (POS) terminals, mobile money and electronic wallets.

Technology is allowing online banking and mobile apps, contactless card payments, electronic fund transfer and e-money, the last two of which are being boosted by the advent of faster payments. 60 countries have this in place already with many more following on.

Between 2020 and 2021, the number of fast payments per person increased by 30%. Korea had the highest number, 138, followed by Sweden at 75, although in Korea the value per transaction was much higher, reflecting their use for paying major bills. Most countries were in the range of 20-40 per person.

Legal and regulatory frameworks have had to rush to keep up and these developments have led to changes in consumer preferences and behaviour. There is, of course, always a debate about whether change has been driven by technology or user preferences.

The pandemic undoubtedly accelerated trends that were already in play, particularly digital credit transfer and contactless payments. It also drove a surge in cash holdings that has not yet reversed.

Post-pandemic

Since the pandemic, cash usage for payments has started to recover, at least to some extent, and store of value holdings have started to return. The end of negative interest rates in some jurisdictions may also have encouraged this. The use of contactless payments, in all forms, has continued to increase.

The trend to fewer ATMs and bank branches has continued and the uptake of fast and real time payments is accelerating fast. The paper regards faster payments as a significant catalyst of change. The move of non-bank payment service providers into the payments arena is continuing, bringing with it increased competition.

These changes are visible in the data for the annual number of digital payments per person for the CMPI members. In 2012 there were 179 digital payments per person, in 2021 332, an increase of 85% over 10 years. Unexpectedly, between 2019 and 2021 the increase was 32 payments per person, 300 to 332, a slight slowing compared with the trend rate.

The volume of payments made without cash in 2021 grew strongly, but unevenly between AEs (11%) and EMEs (34%). In both though, card payments drove the most growth. In AEs card payments were up 11% and in EMEs 23% in 2021, while in earlier years those increases were 6% and 13% respectively. The report suggested that this showed the shift to cashless payments is sticking.

AE and EME regions are changing at different rates and in different ways. E-payments per person are lower in AEs than EMEs, 12 v 43, while direct debt payments are higher, 56 in AEs and 12 in EMEs.

The share of debit card payments remains high at 65% of all non-cash payments, although this is little changed from 2012 when it was 62%. The value of payments made by debit cards is lower than for credit cards since they tend to be used for everyday purchases.

Focus on cash

In 2021 cash withdrawals slowed. In AEs they were higher than in 2020 but in EMEs they were less than in 2020. There was no information about why this might be the case.

In 2021 cash withdrawals slowed. In AEs they were higher than in 2020 but in EMEs they were less than in 2020. There was no information about why this might be the case.

A useful table showed data for 18 countries on the change in cash in circulation levels. Between 2012 and 2019 in half of the countries cash volumes grew – Argentina, India, Indonesia, Italy, Mexico, South Africa, Switzerland, Turkey and Zambia. However, in 2021 only seven countries saw growth in the volume of cash withdrawals per person – Argentina, India, Indonesia, Italy, Mexico, South Africa and Turkey.

Only in the Netherlands was the fall in cash withdrawals in 2021 more than in 2020. The data also demonstrated that as the number of ATMs fell, so the value of the money withdrawn from ATMs increased. Again, the Netherlands was the example used to demonstrate this.

Cash as a percentage of GDP fell in most countries in 2021, although it was still greater than before the pandemic.

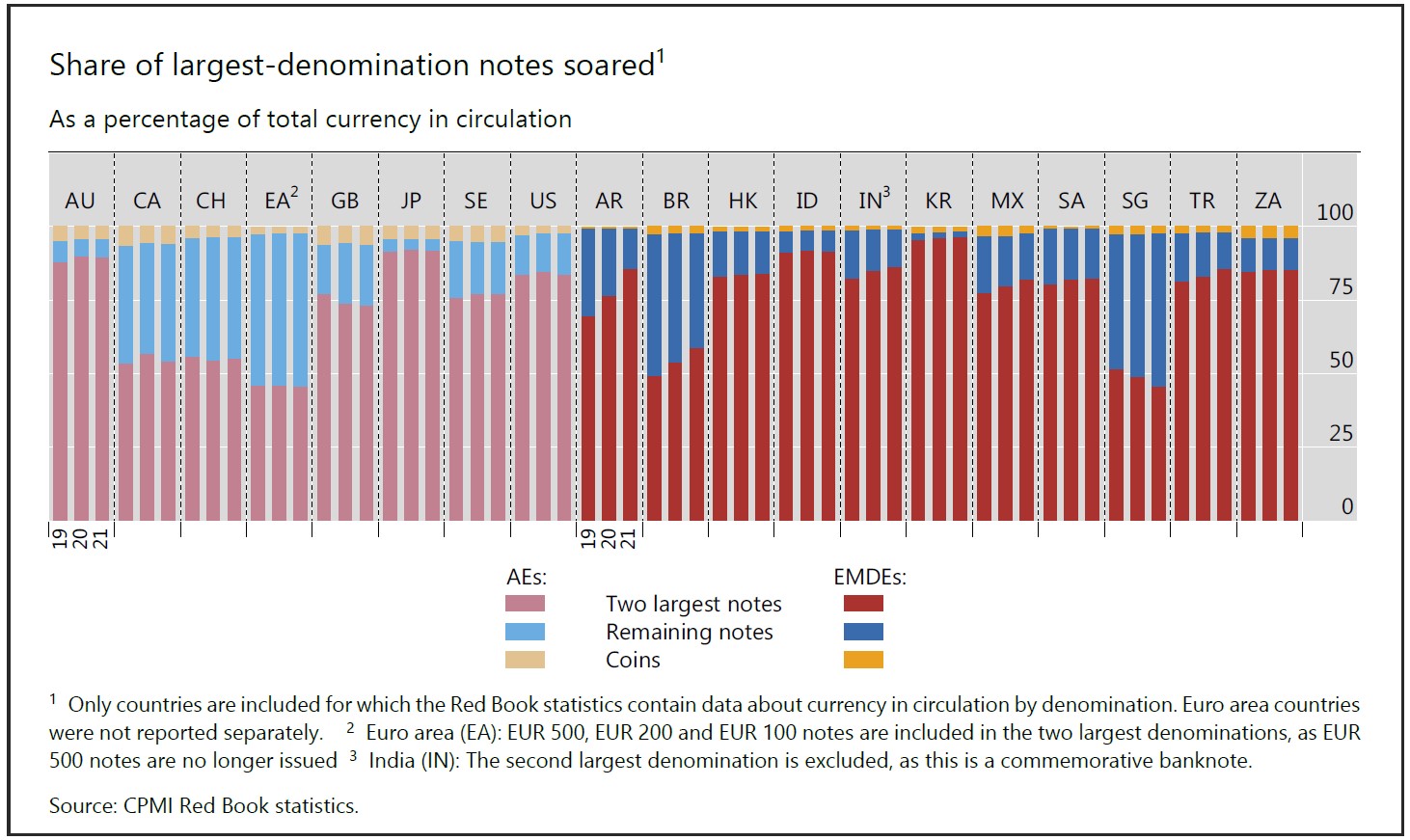

Denominational spread

In Brazil, Canada, the Eurosystem, Singapore and Switzerland the high denomination banknotes accounted for 50% of cash in circulation. This suggests that in these countries cash is still widely used for transactions.

In the other countries the high denomination notes made up over 75% of cash in circulation. This may be because the denominational structure is inefficient and the low value banknotes are fulfilling the function of coins.

The use of high denomination notes either increased or stabilised in most countries in 2021. This suggests that the store of value function of cash was not yet significantly reversing.

Coins made up a negligible part of cash in circulation in the Eurosystem area, Argentina, Brazil, Hong Kong, India, Indonesia, Korea and South Africa. This may suggest the denominational structure is inefficient and so coins are not useful for payments.

For those countries where coins make up a visible proportion of cash in circulation, in 2021 they appeared to be stable in the UK, India, Indonesia and Singapore, slightly declining in Australia, the Eurosystem area, and the US and declining in Mexico.

Final word

The CMPI believes that faster payments and the existing technology changes will see electronic payments in all forms continue to grow strongly.

The persistence of a public demand for cash leads the CMPI to speculate about a future role of CBDCs.

In the near term, the opportunity to enjoy faster and cheaper cross border payments depends on solving interoperability challenges so that faster payment technology can be extended beyond domestic borders.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.