CBDCs: Public Infrastructure for Innovation

Dr Wolfram Seidemann, CEO of G+D Currency Technology, pointed out at the company’s July Currency Technology Symposium that it’s not only about the resilience of the existing cash cycle, but it’s also about innovating the new cash cycle.

The world is changing, G+D Group CEO Dr Ralf Wintergerst explained. Population is increasing while ageing at the time and we see geopolitical and economic changes – all fuelled by growing acceleration of technology and increasing spend on innovation. And change is, of course, an opportunity.

When one considers the world wide web was invented in 1988 and there were no digital payments, the transition to where we are today is extraordinary – fintechs, Payment Service Providers and technology companies working on new digital payment instruments such as cryptocurrencies, stablecoins and Central Bank Digital Currencies.

Technology, confirmed that G+D is heavily committed to cash but believe that there should be a complement in the digital space. The digital payment market is very fragmented, it’s not inclusive and it only addresses specific use cases. A lot of efficiency could be generated if a central bank would issue a digital form of cash that can be used universally as a platform.

CBDC state of play

Over the past years the interest in CBDCs amongst central banks has increased to the point where many central banks are now working on them.

A recent BIS survey suggests that by 2030 there could be 15 live CBDCs in circulation.

G+D started work on CBDCs over four years ago and has had a team of about 50 dedicated people working on it, drawing from its existing expertise in digital payments and building new knowledge and capability.

G+D recognised early on that the offline functionality of CBDCs would be a critical capability to allow them to fulfil their potential, particularly to deliver financial inclusion. It is running or supporting pilots in Brazil, Ghana, Eswatini, Thailand and Hong Kong. The Bank of Thailand trial involves several thousand people and is very advanced, including 24/7 support by G+D.

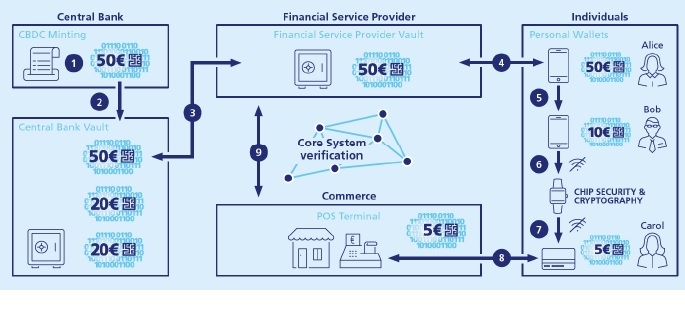

CBDC Ecosystem

CBDCs will, of course, need an eco-system equivalent to the cash cycle. Mainstream thinking is that central banks will use commercial banks at the point of user interface, meaning the commercial banks will, as they do today, manage the regulatory requirements of knowing the customer, anti-money laundering etc.

CBDC will become an entire ecosystem similar to today’s cash cycle.

What problems does a CBDC solve?

19 of the G20 countries are in advanced development stage of CBDCs. Is this a fear of missing out or do they have a tangible benefit in mind? The ECB, for example, has a team of 60 people working full time on CBDCs.

Dr Raoul Herborg, Managing Director of G+D´s CBDC unit, argued that CBDC is a platform – an enabler – for innovation by the private sector. CBDC could be seen as part of the public infrastructure.

At a basic level CBDC`s should deliver value for merchants because they will be easier to use and cheaper for the merchants to use, avoiding some of the fees charged today for digital payments.

For the public, CBDCs should increase financial inclusion, offer new services and increase convenience. CBDCs will be a universal payment tool offering people an alternative to existing digital payment offerings.

To deliver some of these benefits, there will need to be low barriers to entry to allow innovative new players to build their payment services. Perhaps, for example, organisations won’t need to be a bank to provide payment services but will just use CBDCs to do this.

One can be of the opinion that CBDC`s are not really solving simple day to day transaction issues, but they certainly address the lack of standards and bottlenecks in bank and financial innovation. To enable innovation, there is the need to set appropriate regulatory frameworks and to put in place common and interoperable standards, granting access for all market participants.

Examples of future innovations discussed were:

Programmable payments (with smart contract integrated)

Special purpose money

Delivery against payment, payment against delivery

Machine-to-machine payments

Green wallets.

Positioning for future payments

The case for CBDC`s is driven by a real belief that the public need a digital fiat currency as a safeguard against all the things that can go wrong when the profit motive runs amok. Over and beyond, a CBDC could – if done right – deliver growth to a country and value to the people serving as a platform for innovation. Even though, there are still many questions to answer and a long journey ahead.

In the Currency Technology Symposium G+D demonstrated that it is at the heart of this story, helping shape what is to come.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.