Branch ‘Deserts’ a Myth in the US

The Banking Journal of the American Bankers Association (ABA) published an article ‘The Real Story On Bank Branch Closures’, about the decline in bank branches in the US. It was responding to a story in NPR that painted a picture of bank closures leaving whole communities devoid of bank branches, particularly in lower-income, rural and at-risk communities.

The ABA tells an interesting story of what has actually happened, including data and an initiative to reduce the number of unbanked Americans.

Branch closures

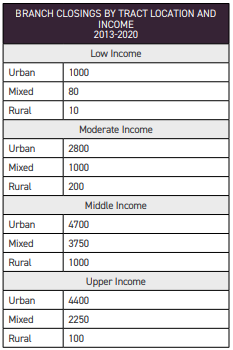

Data from S&P Global Market Intelligence reported 3,324 branches closed last year in the US and 1,000 opened, leaving 85,000 in place. Bank branches can close for a variety of reasons – for example industry consolidation, lack of demand, increased use of mobile and online banking. In reality, most closures have been in upperand middle-income areas (76%) and in saturated urban markets (94%).

In the period 2013-20, on average a branch that closed had 18 branches within two miles of it and 159 branches within 10 miles. Only 5% of closed branches were in low-income areas, leaving 99% of such areas within commuting distance of a branch. 0.5% of branch closures were in rural areas and only five branches closed in rural low-income areas.

Access to bank branches

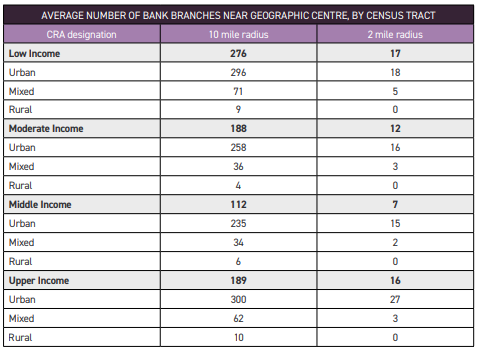

As the table shows, low-income, urban, mixed or rural areas are better served by bank branches than any other income group.

Source: ABA.

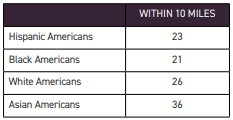

Source: ABA.Analysis by racial and ethnic groups shows similar results.

Where there are banking ‘deserts’, the areas are extremely rural and with low population densities, a median of 7.6 people per square mile. 80% of those people are white, mostly upper- or middle-income.

The ABA suggests targeted investment in internet infrastructure as one solution. Based on Federal Deposit Insurance Corporation (FDIC) data, 34% of American households used mobile channels in 2019 to access bank accounts, up from 18.4% in 2017. The biggest groups moving to mobile banking were black, Asian and Hispanic Americans, so this does not seem an outlandish suggestion.

The ‘unbanked’

FDIC data says 7 million Americans, 5.4%, do not have bank accounts. Given 99% live close to a bank branch, typically within seven city blocks, the FDIC research suggests that access to a branch is not a key reason for being unbanked. Instead, the reasons for not having bank accounts were:

48.9% – funds too low to meet the minimum balance required for an account

36.3% – don’t trust banks

36% – privacy concerns

34.2% – account fees too high.

The ABA is working with the Cities for Financial Empowerment (CFE) Fund trying to get more financial institutions to join the Bank On initiative. This creates certified accounts to encourage the unbanked to open accounts by offering low costs, online bill paying, no overdraft fees and transaction capabilities such as debit or prepaid cards. So far 3.4 million accounts have been opened across 10 institutions, with 75% of those opened by new customers.

To achieve this result though, the CFE Fund has worked hard with specific messaging to reach the unbanked. Focus groups and surveys were used to develop those messages and to develop education programmes.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.