Cash in the USA – an Update

Three reports bring insight into the impact of the COVID-19 pandemic on payments in the US.

The 2021 Diary of Consumer Payment Choice gives good data suggesting that cash is holding up remarkably well, but its transactional use has fallen sharply. A report from CivicScience provides a different view of how the pandemic is changing online and mobile banking, less than other data suggests. CMSPI explains how three factors, two of which are pandemic related, are driving up the cost of payments for merchants. In passing it does mention that moving away from being paid in cash is part of the problem.

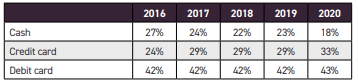

Cash transactions fall sharply in 2020

The Cash Product Office and Reserve Bank of Atlanta have issued the 2021 Diary of Consumer Payment Choice findings. The headlines are that the number of payments fell with the number of low value ‘day-to-day’ payments markedly lower. The value of payments rose as people consolidated their shopping buying online. Cash held at home rose sharply across every age and income group.

These are clear changes from previous diaries, representing the impact of the COVID-19 pandemic. The unanswerable question is what happens next?

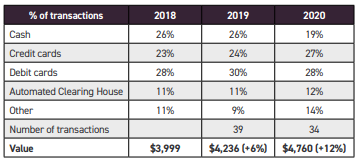

The survey takes place in October each year, although in 2020 there were additional surveys in April and August. Between the 2019 and 2020 surveys the number of payments made each month per person fell from 39 to 34, with payments under $25 down 26%. Since cash is used predominantly for low value purchases, the number of cash transactions fell from 26% to 19%.

For transactions with a value under $25, the number of debit card transactions fell from six to four while cash fell from eight per month per person to four.

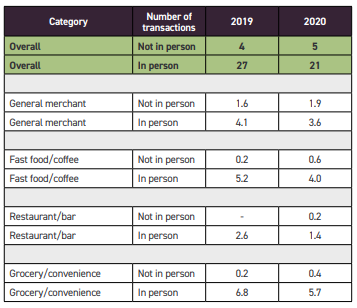

A part of the reduction in cash usage lies in what happened in grocery stores, dining establishments and general merchandise stores, which are places where cash is – usually – widely used. In this survey, the value of spending in these locations using ‘not in person’ payment options, not relating to paying a bill, rose from $110 to $212. In the August survey, 45% of respondents said they had been encouraged by retailers not to pay in cash.

The number of credit card payments did not change between 2019 and 2020. The increase is a function of the reduction in the total number of payments.

Preference for different payment instruments

Unemployment increased in the US from 3.5% in February 2020 to 14.8% in April 2020. Although significant payments were made by the government to the population, the increase in credit card usage may reflect the economic situation, although the report does not draw this conclusion.

Unusually, cash usage fell for every age group. The biggest reduction was in the 18-24 age group. At the same time, cash held in person by individuals rose. In 2016 it had been $55 per person. In 2020 it was $74. Again, the sum held increased across every age group with the 18-24 year olds seeing the biggest increase, from about $33 to $60 per person, more than for the 25-34 and 35-44 year olds and only one dollar less than the 45-55 year olds.

When cash holdings were analysed by level of income, the absolute value held increased for all groups. While those earning less than $25,000 per year held the lowest value of cash, $55, the value held was reasonably similar, ranging from $55 to $87 (those earning between $75,000 and $100,000). This age group saw the biggest increase in how much they held, about 67%. It is assumed that uncertainty drove these increases.

The ‘fall’ of in person payments

The number of cash transactions drives the cash cycle, particularly for coins used to settle those transactions. The payment diary provides data about how people spent in places where cash is traditionally used. The big reductions in ‘in person’ spending explain why the number of cash transactions has fallen.

Mobile and online banking edging up

CivicScience, a research company in the US, has published results from a number of surveys carried out between January 2020 and April 2021 looking at payment habits in the US. Some of its findings were counter intuitive.

Despite banks investing heavily in online and mobile platforms, the main determinant of how people decide to open a bank account was location. 26% of respondents gave proximity to where they live as key. 73% of those surveyed lived within a 10 minute drive of their branch. The finding was consistent across all age groups and incomes. Of the 10,000 people in this survey, 16% did not have a bank account.

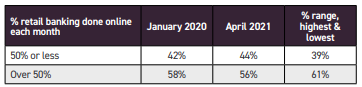

Despite all the talk about the impact of the pandemic, online banking behaviour has hardly changed. In fact, it has declined slightly.

The surveys looked at whether there was a link between whether people bank online and the extent that they shop online or in an actual shop. It repeated this to look for linkages with the time they spend on social media and how they shop. Unsurprisingly, there was a clear link between online banking and online shopping and time spent on social media and online shopping. Perhaps unexpectedly, 47% of 18-24 year olds don’t use online banking.

When it came to income, the survey divided income into those earning $50,000 or less, up to $100,000 and over $100,000 each year. The two segments earning over $50,000 have almost identical percentages for online banking, suggesting that income is important in determining behaviour.

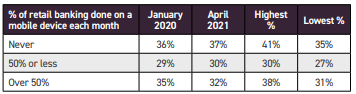

The study then looked at the use of mobile devices to make retail banking transactions (paying bills, transferring money etc).

The survey provides monthly data and the trend line for those never doing banking on a mobile is increasing, those 50% or less is broadly stable and those doing online banking for over 50% of the time is declining.

When the data is analysed by age, there is the expected decline in mobile banking as people get older.

The income figure, however, is slightly unexpected. 39% of people earning less than $50,000 and 38% of those earning up to $100,000 do not use mobile devices for banking. But what is also true is that 43% of those earning less than $50,000 and 45% of those earning more than $100,000 use mobile devices for banking for more than 50% of transactions. The middle ground is rather squeezed.

Moving away from cash payments increases merchant costs

CMPSI, a global payment consultancy, has looked at the US payments market. It reports that the average US retailer operates on a pre-tax margin of under 5% and that payments are a retailer’s third largest cost after labour and premises. Understanding what is happening to payment costs, therefore, is important. The report suggests that retailers are facing rising payment costs from higher fees, a changing payment mix and the pandemic pushing commerce online.

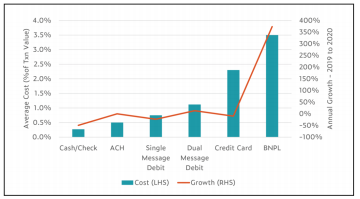

CMPSI estimates that the weighted average cost of payment acceptance has increased from just over 0.8% in 2009 to just over 1.2% at the end of 2019. Their forecast is that it will rise to 1.6% by 2025.

The 2011 Durbin Amendment capped debit fees at 0.05% of transaction value, along with a 22 cent cost per transaction for issuers with assets under $10 billion.

It also required cards to be co-branded with at least two non-competing networks, allowing merchants to pursue least cost routing.

Although it estimates 71% of the savings from these changes have been passed on to consumers rather than being kept by the merchant. In addition, other fees have risen.

Payment mix

Unfortunately, merchants have chosen to ‘pivot away from cheaper payment methods, such as cash, towards higher cost methods such as credit cards.’ A new payment method, Buy Now, Pay Later (BNPL), has arrived on the high street and has proved popular with consumers who do not like credit cards. BNPL grew 350% in 2019-20 which has drawn consumers away from lower debit cards, instead incurring a merchant fee estimate as 3.5%.

The Strawhecker Group surveyed 1,500 US consumers in early 2021 to understand their views about BNPL services. 39% had already tried BNPL services and of those who had, 55% found they had spent more compared with when they bought with other options. Average spend was $312. The reliability of these products was high, although consumers were not so confident about the motivations of the providers.

Cost of e-commerce

When payments are made online, merchant margins are squeezed in a number of areas. For example, fewer payments are approved, there is a greater risk of fraud and there are higher headline fee rates.

In addition, for online payments merchants have to use PINless debit card processes for least cost routing, but the options are restricted making getting good value more challenging. The US Justice Department is currently investigating this market.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.