Cash & Payment Trends from Turkish Perspective

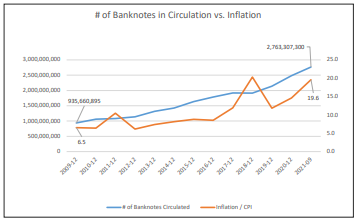

Turkey has a high rate of inflation and household demand for cash has been increasing steadily over the past ten years. The impact of the pandemic was, initially, a decrease in demand because of the shutdowns but, after vaccinations were introduced, demand recovered very quickly. Compared with the 2020 Q1, cash withdrawals from branches increased 23%. Putting aside the shutdown period, it can be concluded that the pandemic has had almost no effect on cash demand. Indeed, consumers appear to demand more cash than ever.

Pace of digitalization during the pandemic

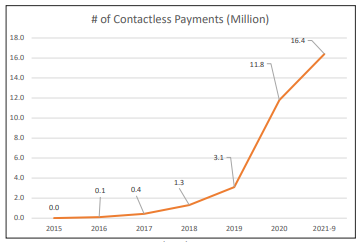

The pace of the digitalization during 2020 increased more than the average because of the pandemic. Banks implemented new digital features or enhanced their digital capabilities as a response to COVID. Customers turned to online channels more than ever, with the value of financial transactions made on the internet increasing 33% and the use of mobile banking increasing by 103% between 2019 and 2020.

The same tendency is seen in the payment choices of the customers, with contactless payments almost quadrupling.

Open banking ecosystem

Turkey’s open banking ecosystem has been growing very fast with many active local and foreign Fintech companies.

With the direct collaboration and support of the biggest private and government banks, the development pace has reached a high level.

Central Bank Digital Currency

The Central Bank of Republic of Turkey (CBRT) has been conducting studies about CBDCs since the beginning of 2020. Recently, it established a Digital Turkish Lira Collaboration Platform. According to the CBRT, the proof of concept studies have finished and it has now moved to the next stage with the participation of technology stakeholders (ASELSAN, HAVELSAN and TÜBİTAK-BİLGEM).

CBRT also plans to carry out tests that may diversify the coverage into areas such as blockchain technology and integration with instant payment systems. The results of the first phase will be announced in 2022 after the tests are completed.

Cash usage habits in Turkey

CBRT conducted a Cash Usage Habits Survey at the end of 2020 to understand these habits as well as the importance of cash in payment methods. This survey covered 1,200 women and 1,200 men with an age range of 16 to 65, from households in the selected provinces of 26 sub-regions. Here are some key figures from the survey: More than 50% of people receive their income mostly or entirely in cash.

Self-identification as ‘mostly cash user’ is much more common among non-deposit holders. Of the survey’s participants, 18.3% did not have a deposit account in any bank. Moreover, the higher the education and income levels, the less cash individuals used.

According to the results of the payment diaries of the participants, cash payments accounted for nearly 90% of the total purchases at the point of sale in terms of number of transactions, and 76% in terms of value.

Compared with the euro area countries, Turkey is the country with the highest share of cash usage by value and the number of transactions.

Answers to cash usage tendency questions indicate no decline in cash usage in the short term. The number of those reporting an increase in their cash usage compared to a year ago exceeded those who reported a decrease. Likewise, the proportion of those who indicated ‘increased usage of cash in the year ahead’ is higher than those that indicated a decrease in usage.

Future trends

The appetite for innovation in the financial sector is high, with significant R&D in the banking sector being devoted to digital banking transformation, blockchain and open banking services. In addition, there is strong support from the central bank and other regulatory bodies to maintain the pace of digitalization.

At the same time as the high pace of digitalization there appears to be no decrease in the use of cash in Turkey. The cost of cash remains, therefore, an important challenge for banks. Consequently, cash process automation and efficiency tools such as predictive/optimization software using big data and AI algorithms will be on the agenda of the banks.

Other optimization opportunities may be about pooling resources such as ATM networks using white-label ATMs, spreading the CBRT’s Note Held To Order project to include more institutions, creating bigger commercial cash centres and even the opening of white-label branches empowered by open banking capabilities.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.