Lessons Learnt Managing a Declining ATM Estate

As the number of ATMs and use declines, authorities face challenges relating to competition policy and appropriate regulations.

This is true in Finland, as elsewhere, and the Bank of Finland has written about their experience 1, learning lessons from the past, the experience of others and the extensive academic work done on this topic.

The paper defines ATM fees and usage fees, and their relative impact on providers and consumers, and finds that regulating interchange fees is a better way to maintain cost effective access to cash than focusing on foreign fees.

Is cash important?

The paper starts by stating why cash continues to be an important payment instrument that the central bank wants to maintain, which means having ATMs readily available to the population.

The arguments are well rehearsed – resilience against electronic infrastructure failure, its requirement by those who ‘shy away from more abstract types of payment’, its anonymous nature and that it provides independence of banks against the power of payment card companies (Visa, Mastercard, Alipay, WeChat Pay etc.) and other payment media platforms (Facebook, Google, Apple etc.), ensuring competition in the market.

Along with the fact that cash is the European Union’s only form of legal tender and the European Commission and the Eurosystem both require that central banks ensure continued access to cash. Cash is, therefore, here to stay.

That said, in 2010 €17.5 billion was withdrawn from Finnish ATMs. By 2019 that figure was €10 billion, and in 2020 it fell to €7.5 billion. The number of withdrawals has mirrored the reduction of the value withdrawn.

Context of Finland’s ATM system

Today all ATMs in Finland are owned and operated by Independent ATM Deployers (IADs). The three largest suppliers are:

NOKAS (branded as ‘Nosto’)

Automatia Pankkantoomeatit (branded as ‘Otto’)

Suomen Käteinosto.

In 1992 Finland had the second highest number of ATMs per person in the world after Japan, with some 3,000 ATMs. Today Finland is towards the low end of the scale, matching Denmark, Sweden, Norway and the Netherlands.

While cash withdrawals at bank branches have been declining since 2002, the number of ATMs started to reduce in 2004 and has been dropping significantly faster and more than branches. In 2014 there were 143.7 million withdrawals from ATMs, by 2020 it was 63 million.

While banks dominated the ATM industry from its start, IADs eventually entered the market to challenge them. This created market competition challenges because banks ran ATM networks and issued and priced ATM compatible payment cards and can earn more revenue from other payments, so have had little incentive to support cash.

Key questions

In the light of the decline in cash and the structure of cash supply in Finland, the paper considers whether less cash is because there are fewer ATMs or vice versa. Is competition working well? Is access to cash hampered to the extent that it no longer provides a viable alternative to payment methods introduced by powerful platforms? Is the ATM network big enough to cope with payment disasters? Whether and how the ATM industry should be regulated to maximise welfare?

Findings

To give context to the findings, it is necessary to understand ATM fee structures. ATM fees consist of usage (retail) fees, which cardholders pay to use the ATM, and interchange (wholesale) fees, that banks pay to the ATM provider. The usage fees are split into surcharges (direct access fees), that are paid to the ATM operator, and foreign (disloyalty) fees, which banks charge their customers if they use a competing ATM network.

1. Is less cash because there are fewer ATMs or vice versa?

Less cash is related to fewer ATMs but the size and structure of the ATM network is directly influence by regulations. Regulatory interventions in Finland have led to the size of the ATM network growing and IADs switching to running all ATMs.

2. Focus on foreign fees

The authorities focused on foreign fees. The report found that although this worked well since interchange fees were set by organisations outside of Finland and the banks owned the dominant ATM networks, it did not prove to be the optimal regulation for maintaining the ATM network.

3. ATM network ownership

Irrespective of who owned the ATM network, it is better to regulate interchange fees. If this is not possible, the usage fee regulations should be made contingent to the interchange fee level.

4. Quantity regulations

If fee regulations cannot be designed optimally, the paper recommends considering quantity regulations, setting goals for the maximum distance people have to travel to access cash. In the Netherlands and Sweden this is organised through voluntary compliance, but regulations can also be set.

Important events that shaped the ATM network

ATMs started in 1972 in Finland, but their story suggests pricing being used to achieve consolidation of the network by the banks, followed by disruption with the entry of IADs.

Again, the response was to use pricing to safeguard market positions which required intervention by the authorities. The solution led to a steady decline in the number of ATMs which was only halted by a change in the rules brought on by Finland’s interpretation of EU 2015 legislation. The result has led the banks to exit the market and the beginning of growth in the ATM network.

1994: Automatia Pankkantomeatit established by the major Finnish banks with interchange fees set annually to cover the cost of the systems. By the end of 2005 all Finnish banks used Automatia ATMs. The result of the small banks joining the system was that they closed their ATMs, reducing the number of ATMs to 1,729.

2008: Eurocash Finland and Suomen Käteinosto were established as IADs, financing their operations based on a share of the interchange fees. As a response Automatia introduced foreign fees. The Finnish Competition and Consumer Authority intervened and set more competitive costs than those introduced by Automatia.

2012: Automatia set a policy of keeping loss making ATMs in rural areas if to close one meant the public had to travel over 20 km to access cash.

2013: Cashback started.

2014: Directive 2014/92/EU required banks to provide banking services, including cash withdrawal.

2015: EU regulation (EC) No. 924/2009 required service fees for cross-border payment transactions within the European Union to be the same as in the home country for similar services. The result, in 2017, was that using the Nosto ATM network had to have the same pricing structure as the Otto network.

2017: NOKAS CMS Oy bought Eurocash and increased the number of ATMs by 95, bringing the total to 165. It also did a deal with the retail chain S Group to introduce more ATMs. S Group had been unable to get Otto to increase the number of ATMs. It had been forced to pay for a minimum number of withdrawals because the ATMs in their shops were used insufficiently.

2020: By 2020 Otto had reduced its ATM network by 409 from 2014, while Nosto had increased its number to 555. The number of ATMs in Finland had increased by 20% since 2016.

2020: Loomis bought Automatia. To date Loomis has not changed Automatia’s business model. All ATMs are now owned by IADs in Finland.

Comparative experiences of other countries

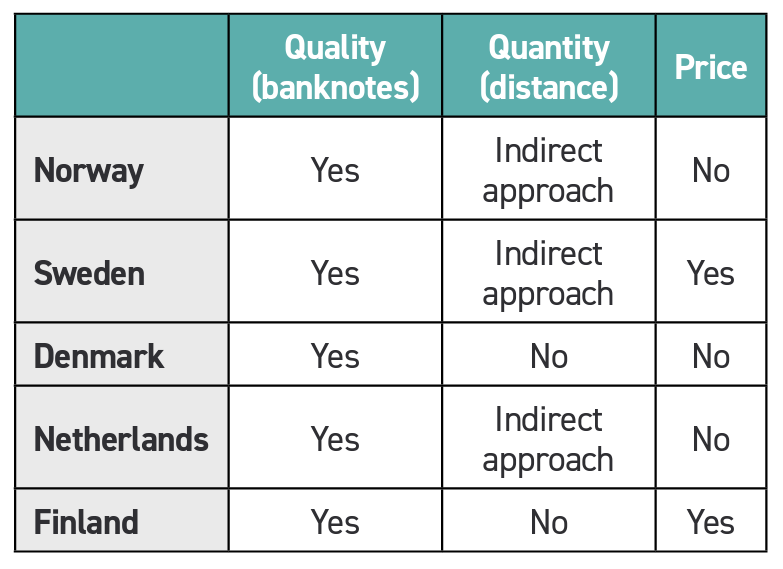

In terms of cash usage, Norway, Sweden, Denmark and the Netherlands face similar challenges to Finland.

Norway has no price regulations, but its 2017 Financial Undertaking Act requires banks to ensure customers have access to their deposits but does not require access to cash.

Sweden’s 2021 Payment Services Act requires banks to maintain sufficient access to cash and bans foreign fees. The largest bank runs 56% of ATMs, Nokas 22% and ICA, a retailer, 18%.

Denmark has no price or quantity regulations.

The Netherlands has set a goal of the public being within a 5 km radius of an ATM. This is achieved through a voluntary system. Prices are not regulated.

Policy considerations and learnings

The paper considers how central banks can encourage the maintenance of appropriately sized ATM networks.

Foreign fee schedules encourage banks to develop their own networks so that they don’t have to pay when their customers use other ATMs. If there are no foreign fees and a dominant supplier, then convenience goes up for consumers but there is no incentive for banks to increase their network. This is the case in Sweden and Finland.

On the other hand, surcharges and fees can provide incentives to increase the network because banks want their users to use their ATMs and not their rivals.

Between 2009 and 2018 cash services were loss making in Finland, which saw a spiral of decline as a result – fewer ATMs, fewer cash withdrawals, increasing costs. The ban on foreign fees in 2017 changed the situation, leading to the increase in Finland’s ATM network.

While interchange fees determine the network size for IADs, they create pressure for banks to raise usage fees which then dilutes the incentive for IADs to increase their network. For this reason, the conclusion of the paper is that foreign fees can be left unregulated so long as interchange fees are set at an optimal level. The reverse does not apply.

1 - ‘Competition and regulation in the Finnish ATM industry’. Tuomas Markkula, Tuomas Takalo. BoF Economics Review, No. 8/2021.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.