US Payment Diary Findings 2022

The Federal Reserve Bank of San Francisco has published its diary of consumer payment choice based on its 2021 research 1. The diary was kept in October 2021 at a time when average COVID-19 infections ranged between 72,000 and 110,000 infections per day. The impact of the pandemic was, therefore, still being felt, albeit in its second year.

The Federal Reserve has recorded payment diaries every October since 2016 but during the pandemic had supplemental diaries in April 2020, August 2020 and April 2021. This summary only looked at October surveys.

While the key finding was that total payments, cash payments and the number of payments made in person, referred to as in-person payments, increased compared with 2020, the change was so small that it was not statistically significant. It is possible though, to start to hypothesise about the impact of the pandemic.

Payment overview

In 2016, 26% of payments were made in cash. This percentage fell steadily until 2019, declining about 1% a year. In 2020 it dropped sharply to 19%. This year the figure is 20%. In person purchases and person-to-person (P2P) payments rose to 82%, up on 2020’s 80% but still significantly down on 2019’s 87%. The report posed the question whether this may reflect cash having reached a new, lower, level.

‘On person’ cash is cash carried by an individual while ‘store of value’ cash is cash held at home. The data suggests a move back towards more normal levels of on person cash but people continuing to hold reserve of cash at home, perhaps reflecting a continued level of concern about the situation.

The number of monthly transactions per person fell from 38 in 2019 to 36 in 2021. The number of cash payments increased from six in 2020 to seven per month in 2021.

The increase from 6% to 7% in credit and debit card payments is due to a fall in the number of overall payments rather than an increase in the number of card payments. The fall in the number of payments was driven by fewer cash payments.

Factors in the decline of cash use

The report identified four key factors in the decline of cash use:

1. Less in-person shopping, resulting in fewer opportunities to use cash

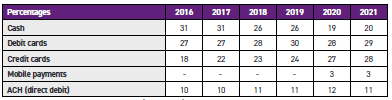

The table below shows how the percentage of payments has changed.

The number of in-person payments in cash was 27 in 2019 and 23 in 2021, while in 2021 the number of online, remote and P2P payments had not changed. An important part of this is how habits have changed when eating out, the move from in-person to remote payments particularly in fast food and coffee shops.

The report questions whether the 2021 change reflects choice while the 2020 figure was because of necessity. Have people now experienced non-cash payments and found them convenient?

2. A reduced preference for using cash

The stated preference to pay in cash in-person declined steadily from 27% in 2016 to 23% in 2019. A reduction to 19% in 2021 is statistically significant. The fall in preference for cash has been matched closely by a preference for credit cards, although this was primarily due to a decrease in the number of cash payments from ten to seven, rather than the increase in the number of credit card payments from seven to eight.

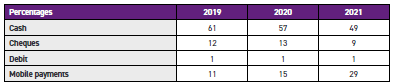

3. Consumers increased use of mobile apps to pay another person

The rise in the use of mobile apps to pay is striking, while cash, although still a significant percentage, is now below 50% for the first time. The decline in cheques is perhaps unexpected, having held up well in 2020.

Person-to-person payments by payment share.

4. A reduction in the number of transactions with a value of $25 or less

A decline in the number of payments under $25 is the main reason both total payments and cash payments declined since 2019. Cash fell four points between 2019 and 2020 and then recovered a percentage point. Credit and debit cards only fell by a point each between 2019 and 2020 and then remained unchanged.

The report notes that the number of in-person payments under $25 has decreased almost every year since 2016 and so does not believe that post-pandemic there will be a significant recovery.

Cash use by demographics

Consumers under 25 reduced cash use in favour of card payments. They made fewer cash payments overall and more card payments. Their willingness to switch to cards suggests that their cash usage will not return to pre- pandemic levels.

Consumers in lower income households continued to rely on cash for payments. Lower income households, those earning under $25,000, have always used more cash than other households, approximately three times more at 36% of payments compared with 11% for those earning over $150,000. Lower income households continued to use cash during the pandemic at the same level as before, demonstrating their dependence on cash for everyday payments.

Trends in cash holdings

Between October 2016 and October 2019, the value of currency in circulation increased on average 7% annually. During the time of the pandemic it increased by 12% annually.

On-person holdings rose and then fell in 2021. The decline in on-person holdings in 2021 was observed across all age and income cohorts. The return toward pre-pandemic levels of on-person holdings suggests the additional on-person holdings in 2020 were temporary and kept as a back-up payment instrument for emergencies.

Consumers’ average store-of-value holdings have increased more rapidly since 2018 than they were before; with increases of 22% in 2019, 24% in 2020, and 20% in 2021. The only explanation is people responding to uncertainty.

Final word

As always, the annual survey provides a useful overview of cash in the US. It has within it key information about Americans’ perception of risk, the size of the population who have a genuine dependence on cash and evidence that some of the changes driven by the pandemic are unlikely to revert back, for example, a preference for paying remotely and use of mobile apps, and the comfort of the under-25s to use cash alternatives.

It also shows the underlying resilience of cash and how core it remains to payments in the US.

1 - 2022 Findings from the Diary of Consumer Payment Choice. Emily Cubides, Shaun O’Brien.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.