Armaguard/Prosegur Merger Gets the Go-Ahead

Many countries are facing falling cash demand, which is causing problems in the cash cycle. This report, by Paul Blond of the Blond Group LLP, shows the compromises having to be made in Australia as a result.

The Australian Competition and Consumer Commission (ACCC) has finally approved the merger of Australia’s two largest cash in transit companies, Linfox Armaguard and Prosegur Australia.

The merger will create a single cash logistics provider, operating under the Armaguard name, which currently has an estimated market share of more than 90%.

The complex nine-month long review saw the competition authority gather more than 80 submissions, 13 witness statements and four expert reports, forcing them to extend their decision-making deadline several times.

Industry in decline, cash remains crucial

The review concluded that the Australian cash-in-transit industry is in structural decline due to the decreasing use of cash as a method of payment, but noted that cash continues to be crucial to some parts of the economy.

Commenting on the decision, ACCC Commissioner Liza Carver said: ‘we accepted that, without the proposed merger, it was highly probable either Armaguard or Prosegur would withdraw from the declining cash-in-transit market in the near future and this exit could occur very quickly. We were concerned that the rapid exit by either of these two major suppliers could cause significant disruption, including by reducing the availability of cash to their customers, and therefore the public.’

While the speed at which either company might exit the market is debatable, the threat appears to have swayed the ACCC’s decision. What is undisputed are the considerable losses that both companies have sustained under current trading conditions. Ms Carver acknowledged that the proposed merger could substantially reduce competition. A number of competitors and customers had raised this concern, along with the threat of potential price rises which it could cause.

To address these fears the ACCC will impose a series of obligations on the combined business that will be effective for the next three years.

Three-year competition undertaking

The undertaking, which went through three iterations incorporating a range of feedback, sets out a number of obligations for the combined business. The company will be required to continue offering cash-in-transit services to all locations that are currently serviced. Current pricing must be honoured for existing customer contracts and new customers, or renewed customers. Contract price rises must be capped at not more than the increase in the Australian Consumer Price Index (CPI) plus 7.5% annually.

In their response to these obligations, the applicants claimed that even with this level of price increase the combined business would not break even over the three-year term of the agreement, reinforcing the challenging state of the cash logistics business and the need for longer term solutions to secure cash distribution, access and acceptance.

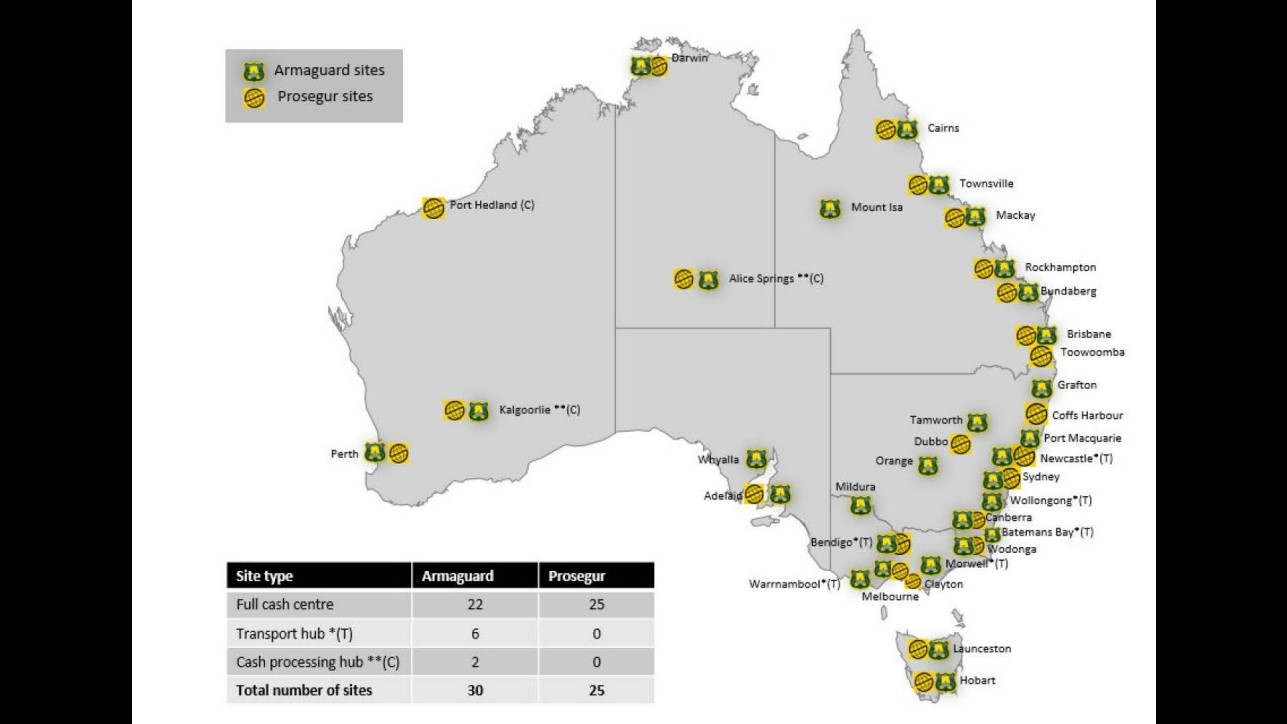

Map illustrating the degree of cash centre duplication across Australia (from applicant’s merger submission September 2022 but with some changes since submitted).

Additionally, the company must establish a register of assets that include surplus Approved Cash Centres, surplus equipment and a register of former personnel to assist other companies that might seek to acquire these assets to grow their own businesses.

The undertaking also sets out various requirements to enable third parties, including independent ATM deployers, to have access to approved cash centres and to provide a range of ATM specific and cash processing services. To support the agreement the company must follow a formal complaint handling process, appoint an independent expert to adjudicate disputes and also appoint approved independent auditors.

It will be interesting to see how these obligations play out over time, whether they facilitate greater market competition and if they contribute to the safeguarding of cash.

ATMX and Precinct – more than just ATMs?

A feature of the declining transactional use of cash and the growth of digital payment and banking alternatives has been the widespread closure of bank branches and bank ATMs. Both Armaguard and Prosegur have developed their own ATM networks, Armaguard acquiring ATMs from ANZ and Commonwealth banks as well as incorporating the Cuscal owned rediATM network under their ATMX brand.

At Prosegur, the company has rebranded the offsite ATMs they acquired from Westpac Group in 2019 as Precinct, an offering styled as more than just an ATM network, but a multi-bank solution. From this year Prosegur is also starting to offer Courier and Access Hubs from their cash centres under the Precinct banner.

With Westpac Group recently extending the existing fee free access for its banking customers at Precinct ATMs to ATMX ATMs as well, it will be interesting to see if the merger will result in a single ATM network, or whether the two brands can co-exist.

Certainly, in addition to ATMs for cash access (and acceptance) there are opportunities to develop shared banking hubs and provide cash centre access to the many smaller cash couriers that form an essential part of the Australian cash ecosystem and who are finding it harder and harder to access traditional bank branches for business cash deposit and withdrawals.

Time flies

While the cash industry has largely been in a holding pattern while awaiting the outcome of the merger decision, Australian payment behaviours continue to evolve.

According to the Reserve Bank’s Consumer Payments Survey, just 13% of payments were made using cash in 2022 whereas, in 2019, this share was 27%. At the same time, financial institutions are reducing the number of branches and ATMs they operate across the country.

The Australian Prudential Regulation Authority reports that over the five years to June 2022, bank branches have declined by 30% in major cities and by 29% in regional and remote areas. The number of ATMs in Australia have declined by approximately 25% since their peak in 2016.

In part prompted by the RBA’s suggestion to change the originally proposed open-ended nature of the merger agreement, the ACCC believes that the now three-year undertaking will allow time to consider whether any government responses are needed to further regulate the industry and maintain adequate access to cash in the future.

It is likely that market forces alone will not fully address these challenges. And while the newly created RBA led industry forum established to support proposed changes to the country’s wholesale banknote distribution arrangements will no doubt play a part in determining the future shape of the industry, time remains of the essence in ensuring cash remains an available and reliable payments choice.

Referencing the merger, the government, in its Strategic Plan for Australia’s Payments System (see article on page 5), has committed to work with relevant agencies across the public sector and with industry to ensure that Australia has a sustainable cash distribution network that maintains adequate access to cash.

How that takes shape remains to be seen.

Subscriber content

Read the full article

Full access to Cash & Payment News articles, newsletters and archives.